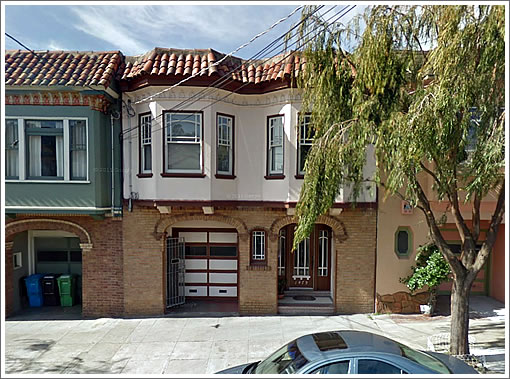

Purchased for $215,000 in 1999, the owners of 1479 Quesada Avenue borrowed $590,000 in July of 2007 and pledged their property as collateral. By the end of 2008 the owners were already $14,695 past due on their payments. And this past April, title to the house was taken back by the bank with no bidders at $379,000 on the court house steps.

This morning, “Occupy” organizers plan to rally at 1479 Quesda Avenue to protest “unfair foreclosure proceedings” at the property. No word on how being evicted for borrowing over a half-million dollars and then failing to pay it back constitutes being unfair, other than to those who made the loan.

I feel bad for the situation of these homeowners who may have fallen prey to unscrupulous lending. The fact that the publishers of this website show no concern and are dismissive to the occupy movement is very disheartening.

[Editor’s Note: There’s nothing to suggest these homeowners fell prey to unscrupulous lending. In fact, keep reading, it’s actually the opposite and the Occupy movement isn’t doing itself any favors by associating themselves with this as an example of economic injustice.]

Property tax records went to a PO box, so it was likely a rental.

So they made no payments, and collected rent or got free rent, for about 4 years. Assuming 45 months @2000 per month, that’s $90,000. That’s nearly 20% of the property value. So you can get 20% of the property value by just walking away from the mortgage. If you had a downpayment, you can bet it all back. You can manufacture equity out of thin air.

The property has not even been resold. Anyone who thinks the worst is past us is dreaming.

Wait… you “feel bad” that these homeowners borrowed $500,000 and never paid it back? LOL…

Oh lord.

I think the Occupy Movement’s insistence on painting all things black and white is disheartening. On the whole, the movement has an important message – but it gets lost when they choose stupid battles like this one.

What does borrowed $590k means? Do they cash out $590 in a second load? Assuming they have 30% equity to the original load in 2007.

Amount owned on first mortgage = 215*70% = 150k

Estimated Property value = 350k

Equity on the original load = 350-150 = 200k

Finally amount they made = 590-200 = 390k

That’s quite a loot.

Message to the occupier, the foreclosed owner has (or has spent) $390k more than you.

Oh and there was a $74,000 second behind that $590,000 first. $664,000 in House ATM cash. But greedy greedy greedy. These loans were in July 2007. Back in 2006 they refi’d with a $556,000 first and $50,000 second. $606,000 in total. So while there property was actually starting the spiral down in value in 2007, banks were pumping them with more cash. Brillant. Greater fools theory and the banks are the greater fools. Not the homeowner who quite realistically stole money and defrauded the banks.

So in this case, Occupy Wall Street, you are barking up the wrong tree. Don’t protest the bank at the benefit of the “poor” foreclosed homeowner. Protest the greed of all who have cost the tax payers in this mess.

And for the record, I believe in most of the message of Occupy Wall Street. And as a democracy, it is the dearest freedom we have. Which is being pepper sprayed upon by university police, and debunked by those in power who are fighting change eventhough the system is broken.

Instead go Occupy Bank of Agony (Countrywide) as they are more fundamental to the crisis.

“I feel bad for the situation of these homeowners who may have fallen prey to unscrupulous lending. ”

Consider reading about the great depression where balloon mortgages were more common. Contrast the above situation with someone who actually saved for years to make a down payment. Made all their payments. Still had a job, but lost the home (and probably any accumulated equity) simply because they could not pay off or roll over the ballon payment.

I am worked all my life, saved and made a conservative purchase in 2003 (large down, 15 year good rate at time). I pay mortgage as well as all my bills on time. I drive a 12 year old car and live frugally. Somehow I think I am being punished for being responsible. Someone tell please tell me, am I out of step?? Oh and when I read the OWS thing all I can say is …well can’t say those words actually.

The more I think about this “protest” to put the back to the house the more ridiculous it is. The former owner are laughing they way out with all the obligation free money the take from the bank.

If you put him back into the home, you will bind him back to the financial burden, even if the loan amount is negotiated down. It will be a long term shackle he cannot escape. Do you think he can really pay off the loan?

This guy is a big winner from the sub-prime crisis. You guys should hold a party to congratulate him.

Occupy protesters need a dose of smartness. They are picking wrong issues to protest. If there overall message is that our government is working for lobbyists. I agree with them. But there execution is stupid. They look like lazy, jealous and unproductive people on the streets.

If you want change in government, protest infront of congressmen’s office, or DC. Find the congressmen who supported any lobbyist sponsored legislation, and make your case with them. Make sure you vote them out in the next election.

Instead they have another hippie movement in the parks and in many cases disturb the life of normal people.

The most clear and simple reason why Occupy is important. And even if you don’t agree with it, why democracy is being challenged by big money and big politics.

http://front.moveon.org/the-single-most-important-robert-reich-clip-you-can-share-today

Here is a real-time twitter feed. Apparently the Cops are there now.

https://twitter.com/#!/search/realtime/1479%20Quesada

So they cashed out for $449K, rented the place for $48K that year, I’m sure they had a job that paid over $20K a year. Putting them in the 1%.

oy…Eddy I looked at that twitter feed. punkboysf in the black bandana seems to be leading the charge. Ugh…those black bandana wearing anarchists were the death of Occupy Oakland…they seek confrontation, destroy property and in general stupidly think that tearing down the system (any system) will somehow make things better. Occupy Oakland had no power to keep them in line, particularly with their consensus-based direct democracy model, and floundered. It was sad.

I too have a lot of lot of sympathy with the fundamental message of Occupy Wall Street. The system IS broken. But, of course, the message is subverted by focusing on things like 1479 Quesada.

OWS is as ideologically incoherent as the Tea Party. “Keep the Government out of my Medicare!” can be viewed in the same light as this “protest” today.

i won’t be apologizing for the borrower or helping her move back in (and i certainly can’t comment on whether her lender was scrupulous or whether she knew what she was agreeing to)…but the speculation – on high living, cash outs, and motivation – is pretty amazing here.

an internet search suggests the borrowing was related to a disability filing and medical bills (not trips to paris or jet skis). they also suggest the the 1999 purchase may have been a generational transfer of wealth from child to parent (there’s a claim that the family built the home). i wonder how many of us are one illness away from bankruptcy? more then realize it, i’d wager.

evidently 14 houses on this block have been foreclosed on. any owner on this block with an ARM (like over 90%(?) of bay area buyers in the years up to the bubble) is very underwater and therefore unlikely to be able to get refinancing.

the whole story – the loan, the loss, the protest, and the collective violin playing in the face of a fire here- is just sad.

Everyone had its responsibility in the Real Estate / Mortgage crisis, but bankers were not made accountable. Sure enough in a correctly working world everyone would take the heat for their actions, even suffer some level of consequences, enough to serve as a caution for the future. But the imbalance between (guilty) over-leveraged bankers still collecting millions and (also guilty) over-leveraged home-debtors who are kicked out of their homes is strikingly unjust.

If one was bailed out (which is unjust, I repeat), why not bail out the other (also unjust but somewhat fair game)? Whether we might think this action is a misguided move or not, the core of the issue is the total imbalance of power.

Apparently, this is actually part of a larger campaign and not just some breakaway sf occupiers. There’s actually a “Occupy our Homes” movement and today is their “National day of action”

http://www.occupyourhomes.org/blog/2011/dec/6/national-day-action-stop-and-reverse-foreclosures/

@ modernedwardian — Are you sure you have the right story? Ran across something similar to what you describe that happened last month. Same Street.

I agree with Unbelievable completely. Same here, worked hard to save up and buy a fixer home in a now very trendy pricey neighborhood, over 20 years ago. Always pay the mortgage on time. Pay my bills, deal with fixing the house when things break.

I’m responsible, as many others are.

But these people in the above story were not. They were greedy and decided to cheat the system. Zero sympathy.

And zero sympathy for the OWS people when they simply want to stay angry, become violent and camp out in public spaces without a clear true focus.

“i wonder how many of us are one illness away from bankruptcy?”

This is the other Quesada case I was thinking of.

Life can happen, but in my view a first payment default, followed by multiple bankruptcies and a federal suit just to delay proceedings are very indicative of fraud.

“When reporters asked about the particulars of her case, she wouldn’t give any details, but a check of court records show that in November 2006, Gage took out a $525,000 adjustable rate mortgage that started at 11.99 percent.

Her first payment was due two months later, but she never made it. She didn’t pay the next month, nor did she pay the following month.

Lawyers for the company that owns the mortgage told ABC7 Gage never made a payment, declared bankruptcy multiple times, filed a case in federal court and lost for failing to state a relevant claim.”

http://abclocal.go.com/kgo/story?section=news/local/san_francisco&id=8415237

OWS is doing a great job of giving a face to the discontent. If irresponsible bankers had been sent to jail, if actionable and fair new regulation had come out of this mess, I would be the first to say STFU to OWS. But justice was not served and attempts at restoring fair regulation have been smothered.

Sure the borrower was reckless, probably greedy. But everyone was in this equation. Banks should never have lent that much money to her. And it should never have been bailed out for this reckless lending. Moral hazard 101. Floodgates are open. Try and stop the flow now.

@modernedwardian,

We aren’t speculating. This is called due diligence. Some simple math tell us rather than being a victim they get a lot of money from this deal. You should do your due diligence too. The Internet suggests the borrowing was related to a disability filing and medical bills is rather weak speculation. Ask him to produce the medical bills.

Even if they spend all the money on medical need, it is still a huge win for them. Will you and I got 590k to pay for medical expense when we are sick? They already got more than their house is worth. Nobody own them anything.

@ Editor:

WRONG.

the OCW is actually evolving its message quite nicely to where it should have been initially. OWS is finding its voice. OWS is exposing the injustice of the corrupt alliance between “the banking sector/Fed Reserve” and “government, including Congress and Executive Branch/Treasury, etc.”

California is non judicial. Banks are able to foreclose w/out proving contractual rights to do so. Perhaps Banks that foreclose do have the right and requisite documentation, including proper ownership of the Promissory Note, but often times, the foreclosing Bank does not possess the contractual right to foreclose and repossess. In California, ultimately it is up the the Foreclosed person or group to seek out justice himself, herself, themselves or itself, but it is an arduous process the many Defendants do not pursue for many various reasons, including expense, energy, etc.

In essence, the US Government unilaterally elected to allocate “bailout” capital toward the “Bank” or “Corporation” versus the “Individual”. Why??? Why would Hank Paulson/the Fed Reserve/Congress decide to allocate taxpayer capital toward the bailout of Banking entities, etc. versus the “Individual”.

No one has asked for this answer until now via the OWS “movement”. The OWS movement’s message is becoming more and more clear as it evolves. It is gutteral and the OWS “people” are not just speaking for the “99%” but they are ironically speaking for the “1%” too because the damage that the courrupt alliance between the Banking sector/Federal Reserve/Congress/Executive branch will trickle down to the “1%”.

@johnny

It is hard to see anything in your post that is responsive to the Editor’s critique, viz., that a borrower who puts up his/her house as collateral for a *half million dollars of spending money*, blows the cash, and declines to pay any of the loan back, is not an example of someone who has been improperly smashed by “the system.”

To the contrary, the person is one who has gamed the system, ultimately on the tax payers’ dollar, for his/her own personal benefit.

Your post has a whole lot of vague and general language and scare quotes but nothing about the particular homeowner that is the focus of this story. The closest you come is with the insinuation that the foreclosing bank in this instance might not possess the contractual right to do so, but you (of course) nowhere state that that’s actually the case here. (Hard to see how that would excuse or make more sympathetic this borrower’s theft in any case.)

“In essence, the US Government unilaterally elected to allocate ‘bailout’ capital toward the ‘Bank’ or ‘Corporation’ versus the ‘Individual’. Why???”

That is not a particularly difficult question. U.S. banks were/are insolvent. Without huge “bailout” infusions of cash, the financial sector would have frozen, and the broader economy would have crashed much harder into a severe depression with far higher unemployment. Read Econ 101. There was no such risk without a “bailout” of individuals, and I’ve not seen a coherent plan to bail out individuals in any event that would not encourage counter-productive behavior (e.g. encourage those willing and able to pay to stop doing so to get their “bailout”) and penalize those who behaved responsibly. Anyone with such a plan can present it – maybe I’ve just missed it, but I don’t think so. The “corporations” bailed out were basically the auto companies – that has not turned out to be a bad deal for the taxpayer – and AIG/Fannie/Freddie, which was really just more bank “bailout.”

That said, there are certainly sound arguments that the form of bank “bailout” should have been different — nationalization of the banks, boot management, prohibit/tax bonuses, etc. I agree with those criticisms.

“OWS is exposing the injustice of the corrupt alliance between ‘the banking sector/Fed Reserve’ and ‘government, including Congress and Executive Branch/Treasury, etc.'”

Huh? That has been “exposed” by countless others, and I don’t see OWS either “exposing” anything new or working productively to change course. I wish they would do so – I’d support it then.

How long does it take to save $500,000 cash for a family of 4 with an average San Francisco household income? OCW, leave it alone if you are really for regular folks.

“OWS is doing a great job of giving a face to the discontent. ”

“Another ACCE member, Donna Vieira of San Leandro, said she and her husband lost their $718,000 second home in Reno, Nev., to foreclosure in 2010, and blamed the bank for appraisal fraud, although Vieira and her husband both work as real estate appraisers. “We couldn’t do an out-of-state appraisal,” she said. “The day we signed the loan, it was already $243,000 under water. They didn’t disclose that.””

[Emphasis mine]

If these people were helpless victims, what’s left?

Are only couples of in-state appraisers competent to make their own housing choices?

http://www.sfgate.com/cgi-bin/article.cgi?f=/c/a/2011/12/06/BAHB1M8UH3.DTL

Above that the article’s other anecdote is a couple that bought a million dollar house “Because they could afford it” and claims that they got an option arm when they “requested” a 30-year fixed. Even if true, who forced them to make a less then amortizing payment each month?

You may think the Chronicle reporter cherry picked these stories, but note that there were only 12 ACCE (ACORN spinoff) people at the protest and these were two of them.

Consider also that 1479 Quesada was picked by the Occupy people as an example. If Fox News “randomly” picks a less then sympathetic borrower, that’s probably bias introduced by them. But when the organization’s themselves select these examples it tells a different story.

I wonder if race played a factor in the Bay View house. I bet these Occupie folks would not protect a $500,000 mega mansion forclosure in Oaklahoma

@jonny:

If OWS really want to expose the injustice because of bailout, they should protest the source of bailout (Washington, Congress). Focusing on irrelevant issues doesn’t help their cause.

There were others, including many Tea party members who opposed bailouts and brought that issue up. That was one of the reason why some of the Republican congressmen didn’t get elected in their primaries.

I also agree that bailout was wrong (Even the case A.T points out). We don’t know what would have happened if there wasn’t any bailout. Things could have gotten worse and recovered by now. It’s a scare tactic. This is what Bush used to go to War and Obama is using the same to help his buddies.

“I feel bad for the situation of these homeowners who may have fallen prey to unscrupulous lending.”

No, it is the bank and taxpayers who fallen prey to this unscupulous homeowner.

Point proven: you say banks were bailed out because they were “too big”.

Banks should be allowed to go bankrupt just like they were allowed to prior to the formation of the Fed Reserve.

If banks were allowed to go bankrupt and did not have the mother ship of milk from the Fed Reserve to drink from when in trouble then the bank would not have loaned the “$500,000” to this couple and allow them to “blow it”. In addition, if the bank operated from the context that it was “on its own”(like Individual borrowers are) w/out being able to fall back on the Fed Reserve for emergency fund that it provides banks by simply hitting Control Alt Print, then the bank might not have loaned these folks money. The financial relationship is skewed between Individuals and Financial Institutionas that have access to the Fed Reserve and “bail out tax payer money”. Whether the borrowers here were right or wrong is irrelevant. The relationship is imbalanced and unfair, especially for a country presumably Founded upon the “Individual” and focused upon the rights of the Individual as a priority above the rights of “preferred groups” such as the Financial Sector. The OWS movement is evolving toward this focused message. Right or Wrong about OWS, Individual rights in this Country have been consistently diluted over the years and the Foreclosure issue is shining a light on this concept.

For all we know, the foreclosing entity in this case may not have been legally entitled to foreclose much less accept payments from this couple, but often times, because California is a non judicial foreclosure State, the foreclosing entities are able to foreclose and repossess (and sell) properties that they had no legal right to do so.

“Banks should be allowed to go bankrupt just like they were allowed to prior to the formation of the Fed Reserve.”

Seriously? See:

http://www.fdic.gov/bank/individual/failed/banklist.html

Banks “go bankrupt” all the time (although it is a process outside of the bankruptcy code but the effect is similar) and individual depositors get “bailed out” when that happens up to $250,000 per account.

“Individual rights in this Country have been consistently diluted over the years”

Yep – totally agree. This is what OWS might focus on, and I mean focus, not just rant vaguely and incoherently.

“and the Foreclosure issue is shining a light on this concept.”

Nope, not buying that one. Shoving all your chips on the table and losing the hand has nothing to do with the loss of individual rights. Find a better poster child — there are millions of them.

“”and the Foreclosure issue is shining a light on this concept.”

Nope, not buying that one. Shoving all your chips on the table and losing the hand has nothing to do with the loss of individual rights. Find a better poster child — there are millions of them.”

And consider how there really can be no Individual Rights without Individual Responsibility.

If people can’t be held responsible for their decisions of what housing to consume and how to get it (buy vs rent, loan type,…) the only stable alternative is that these decisions will be made for them by banks or the state.

Foreclosure are sometimes the solutions. Big banks are not victimizing people by doing this. If you cannot make your payments, solve the problem and start to rebuild. If you borrowed the money, you owe the money. This is an interesting take on where OWS may get things wrong.

I am not unsympathetic, but OWS should understand that economic collapse would not have made our lives better. Complain about the difficulty of getting/paying for healthcare and you get it right. Complain about a stacked supreme court declaring that corps are people and you get it right.

Complain without just cause…. The 90% that work, pay bills and keep going just shrug and think you are wrong – there goes the message.

Although there are many cases of banks ripping off home buyers and others, this is not one of them. In fact, it appears to be the case that THIS buyer ripped off the bank!

WRONG

@ A.T.: You’re wrong. Banks don’t go bankrupt. If they did, depositors like you(if you had deposits w/a failed bank) would lose your deposit. Nope, “failed” banks are “taken over” by the government, ie, FDIC ie THE TAXPAYER, and your deposits are not lost, but are simply transferred to a different custodian. You don’t understand the difference between bankruptcy and FDIC takeover, but the above explanation should help you.

@ tc_sf: you’re conflicted because you’re an advocate for financial institutions thus fail to see both sides of a coin. Consider this though tc_sf, if a financial institution foreclosed and repossessed your property, yet did not own the Promissory Note you originally signed, then you might argue that the financial institution did not have the legal authority to foreclose and repossess your property. It happens all the time in non judicial California and other non judicial States where financial institutions are not required to show proof that they have legal authority to foreclose/repossess.

there are plenty of issues OWS can focus on such as the health care issue, etc, but what OWS is doing is Marketing 101. Focusing on the Housing issue will magnify OWS’s message to a wider population than focusing on Health Care. Housing has a broader footprint.

“Ugh…those black bandana wearing anarchists were the death of Occupy Oakland…they seek confrontation, destroy property and in general stupidly think that tearing down the system (any system) will somehow make things better. Occupy Oakland had no power to keep them in line, particularly with their consensus-based direct democracy model, and floundered. It was sad.”

Yeah, I was supportive of their cause but when a hi-rise building in which I own a unit was vandalized the day of the Oakland general strike I quickly lost any and all sympathy. Too bad, because the overall movement I think makes sense.

Mr. johnny, I know the distinction between bankruptcy and FDIC actions very well — much of what I do for a living involves one or both of these processes. Yes, failed banks are taken over during the process. And in Ch. 7 bankruptcy, debtors are taken over by creditors. (Both of those are extremely simplified summaries of very complex processes, but that’s it in a nutshell). Are you really advocating a return to the pre-1933 system where depositors’ accounts were not insured? Now I get it. You’re a closet Tea Partier! Go Ron Paul!

johnny,

Banks have gotten a lot better at digging up loan documentation recently since they realize that there is big money at stake. Mortgage insurers like PMI have been denying claims from lenders without the proper documentation for a loan. Eventually, it dawned on the banks that it was worth their while getting the documentation issues sorted out. From PMI’s last quarterly report before filing for bankruptcy:

“The Company decreased its expected future claim denials in the second quarter as a result of significant recent increases in the frequency with which servicers have produced documents for previously denied claims.”

http://phx.corporate-ir.net/External.File?item=UGFyZW50SUQ9MTAyNTE0fENoaWxkSUQ9LTF8VHlwZT0z&t=1

@A.T. NO, I am not advocating anything but what is right, and I don’t give a shit about “tea parties” or any other “party”.

in an earlier post, you implied banks go bankrupt; they don’t. Banks get taken over by the Government, and depositors in the failed bank do not lose anything. if banks went bankrupt in the real sense like an INDIVIDUAL does, depositers would lose their deposits.

Banks get preferential treatment that Individuals do not receive. Explain to me why??

if a financial institution foreclosed and repossessed your property, yet did not own the Promissory Note you originally signed, then you might argue that the financial institution did not have the legal authority to foreclose and repossess your property. It happens all the time in non judicial California and other non judicial States where financial institutions are not required to show proof that they have legal authority to foreclose/repossess.

1. You have yet to present any evidence or even baldly claim that that is what happened at 1479 Quesada.

2. This is not an argument against foreclosing borrowers who can’t or won’t meet their obligations. It is simply an argument that someone else should be foreclosing them. In neither case is the recalcitrant borrower in the right or entitled to a free house.

It is a reasonable point that the holder of the debt ought to be the one exercising the right to the collateral but not one that makes the borrower/thief sympathetic or his/her theft excusable in any way. “Hey, you can’t take this house — I stole my money from that other guy!” (Recall that the non-sympathetic nature of the borrower was the point of the Editor’s post that teed off your indignant ranting.)

and explain this conduct happening right here in the United States of America.

Why does the Fed w/out any real checks get to hit Control Alt and Print give money to selected entities??? Why not hit Control Alt and Print and give money to INDIVIDUALS??? Explain the morality

Numbers for individual companies were equally astonishing. For example, the Fed provided Bear Stearns with $30 billion to see it through its 2008 shotgun marriage with JPMorgan. This was in addition to the $29.5 billion in assets purchased by the Fed from Bear to assist in the buyout by JPMorgan. Citigroup, meanwhile, tapped the Fed for almost $100 billion in January 2009 — its peak during the crisis — and Morgan Stanley received $107 billion in Fed loans in September 2008.

“These banks and the Fed have never believed in transparency,” Mr. Turner said. “I actually think their thought process is sorely flawed. If the banks knew this stuff was going to be made public they’d behave differently. Instead of runs on the bank you’d have bankers doing things intelligently to avoid getting into trouble.”

“…yet [the bank] did not own the Promissory Note you originally signed…”

Just a naive question: how does a an organization who’s core competence includes handling important paperwork manage to lose a key document required to lay claim to a half million dollar asset? Aren’t these guys and gals being showered with huge bonuses because of the great job they’re doing?

I’m an organizational mess yet I can find every receipt for anything I bought for over $100. … and the user manual.

Notice I put “go bankrupt” in my prior posts in quotes to reflect that banks do not technically go bankrupt. You’ve identified the key difference between a true bank bankruptcy and the FDIC process — individual depositors get their deposits guaranteed! And this is your example of how individuals are treated unfairly as compared to the seized bank?

Another very poor poster child.

You’re also under a common misconception. Bankruptcy (real bankruptcy, like an individual Chapter 7) is for the benefit of the individual debtor! It permits a debtor to legally escape debts at the expense of his/her creditors. Banks get seized and management is fired in the insolvency process applicable to banks, and individuals are allowed to erase debts in the process applicable to them. Again, this is bad for individuals and good for banks?

Yet another very poor poster child.

There are countless good causes out there, but you’re supporting some odd ones.

“Consider this though tc_sf, if a financial institution foreclosed and repossessed your property, yet did not own the Promissory Note you originally signed, then you might argue that the financial institution did not have the legal authority to foreclose and repossess your property. ”

That issue has been thoroughly discusses on other threads and really tangental to the Rights and Responsibilities issue. Consider that now lending is 90+% governmental. If people start defaulting and sending the bill to the taxpayer don’t you think this will cause a movement to tighten down on people’s lending choices? What if we still has small community bank lending? You think others in the community wouldn’t care if some people socked it to the local bank thereby restricting lending for all others?

You can’t have a stable system where people have the full Right to make a choice and then dump the consequences on others regardless of the transmission mechanism (big bank, government, small banks,…) Whoever gets the bill is eventually going to move in and restrict the rights of the chooser.

Some people may favor giving up some individual rights for community benefits, but your conjecture that being able walk away from individual decisions scott free enhances individual rights is entirely backwards in my opinion.

What about someone near the Quesada homes that could actually use a home equity loan to start a business but is no longer able to obtain one?

What about someone who could use an Option ARM for its intended purpose (Variable income, soon to be reliable rising i.e. medical resident,…) but can no longer get one?

You could argue that it’s better for the overall system that these choices are far less available, but it’s no victory for individual rights.

@tc_sf: you’re conflicted because you are an advocate for the financial institutions versus the “borrower” or Individual.

I am an advocate for neither.

What I am an advocate for is simple fairness and the current system (the Fed, Banks, Government) is skewed without question toward the “Entity” versus the “Individual”. This is not right.

“Just a naive question: how does a an organization who’s core competence includes handling important paperwork manage to lose a key document required to lay claim to a half million dollar asset? Aren’t these guys and gals being showered with huge bonuses because of the great job they’re doing?”

Acquisitions of other banks or entities who themselves may have gotten the loan via an acquisition. Different IT systems that don’t integrate, re-orgs and cultural integration issues. Retail mortgage banking is really a big money job compared to other banking work.

As others have pointed out though, theres no evidence that this even happened in the case above.

bottom line is that people are greedy idiots, congressmen are whores and the banks are just plain dumm;

there is no responsibility b/c most of these people have been taught from early on (by their parents, the NY Times, Keith Olbermann, the Nation, college “professos”, self-annointed “activists”, etc, etc.) that the system is rigged and, in effect, that the way to get ahead is to screw the system.

However, they have not shown one person who made millions/billions in the financial crisis illegally and who did not go to jail – not one.

For all the bitching about GS or bailouts, no one has stated that what was done was illegal (whether it was dumm or improper is another question).

But the response is to steal and defraud to get ahead.

we are devolving the way of Greece not because of our debts – rather the debts are an indicator of us having devolved as a society to the point that cheating and stealing are acceptable modi operandi and chutzpah is the new normal.

“Retail mortgage banking is really a big money job compared to other banking work.”

Should read “… not really a big money…”

Speaking of bankruptcy, if CA were a judicial foreclosure state, the (former) owner would be in bankruptcy right now. Because its not, she got to walk away with half a million dollars tax free (if it was used to pay medical bills, well that is a separate issue). Again, who am I supposed to feel sorry for?

“if it was used to pay medical bills, well that is a separate issue.”

why?

if the bank who lent her this money, now has to be bailed out, why do I have to pay for her medical bills?

@wrath

“However, they have not shown one person who made millions/billions in the financial crisis illegally and who did not go to jail – not one.”

Unless somebody is prosecuted and sent to jail, it’s pretty tough to definitely say that they acted illegally and didn’t go to jail. Given the scope and size of the collapse, the real question should be why have so few people been prosecuted, and almost nobody in a place of real power.

The foreclosure fraud is a good example of rampant illegal activity which has gone un-prosecuted. Perhaps my info is out of date, but the last I heard nobody of any importance has been prosecuted, despite loads of evidence of blatant & systematic fraud.

Comparing the current crisis to the S&L scandal highlights how little effort has been made towards investigating and prosecuting potential crimes this time around.

The rule of law in the U.S. is basically dead. The powerful do not have to follow the laws anymore.

@johnny

Your problem is that you seem to be missing the point of this article and thread: the owner of this property appears to be a terrible poster child for the Occupy movement. The owner appears to have cashed out in a major way, and not made any payments on at least one of the loans. It’s irrelevant if they money was used for medical expenses (which I’m not sure is the case, there seems to be some confusion on that), since they appeared to have intentionally taken out money and then never paid a dime. There are plenty of people who did everything in the proper way, but were still foreclosed on. Bring attention to those people, not people who clearly gamed the system. What you are doing will only turn off people who are on the fence about the Occupy movement.

The Occupy movement needs to focus on what it’s mission really is, or will probably suffer the same fate as the Tea Party: being co-opted and fractured into irrelevance. The Tea Party was supposedly for the middle class, but as soon as their members got into congress the only thing that happened was a massive tax cut for the rich. We haven’t heard much from them since then. Occupy brought important issues to the national stage, but is now at the same point as the Tea Party was about a year ago. It could become something major, or fade away without much accomplishment. Right now it looks more likely to fade away due to a lack of leadership and focus.

Just my $0.02

occupy ws ended when zucotti park encampment was shut down. the people involved in this protest are extremely uninformed about the history of the extremely reckless homeowners who used the mortgage as their personal bank

and i’m not sure how to categorize the e homeless drug addicts currently encamped in occupy sf. have any of you been? i walked through last week and saw 80% homeless people, 3 sets of people smoking crack and the whole place smelled of piss and marijuana.

i’m a liberal, yet have way more respect for the tea party. at least they are civil and not pissing in banks or causing mass looting or violence.

I predict the OWS movement will start to fade away when the angry, mostly young, unemployed and directionless people begin to feel the cold and damp of the approaching winter.

Time to head back to their apartments and dorms to get warm and hang out on Facebook.

Fadeout. Movement over.

I predict that futurist will change his name for the fourth time sometime in the next six months. And he will still be as clueless as he was as noearch and modernqueen.

OK, sorry for the incivility. But the conditions that underlie and motivate the occupy movement are not changing anytime fast, and to not recognize that an increasing slice of our population is seeing some sorry truths and becoming radicalized in consequence is myopic.

And I predict that curmudgeon will still be living under the bridge next year, sharing space with Michelle Bachmann and Rick Santorum.

As with the Tea Party, the lack of a strong central leadership makes it hard to say with certainty who is and isn’t “officially” speaking for the group.

But the quote below from the link to “Occupy Our Homes” above certainly identifies them directly with OWS:

“The Occupy Wall Street movement and brave homeowners around the country are coming together to say, “Enough is enough.” We, the 99%, are standing up to Wall Street banks and demanding they negotiate with homeowners instead of fraudulently foreclosing on them.

Occupy Our Homes is a movement that supports Americans who stand up to their banks. We believe everyone has a right to decent, affordable housing. We stand in solidarity with the Occupy Wall Street movement and with community organizations who help the 99% fight for their homes.

”

Additionally were there any remaining doubt about whether the “poster children” above were cherry picked to portray OWS and OOH in a poor light, consider that they just posted the video below from their “National Day of Action” featuring what I believe are both the homeowner that is the subject of this thread and the other Quesada home that I mentioned.

Note that Caroyln, who is most likely the homeowner from the abc local link, who took out a $525k loan on a home that her father built and they had lived in for 50 years and then defaulted on the first payment wants people to ask the banks “what they did with the money”

http://www.youtube.com/watch?v=FsSzSooN4Q4

tc_sf is on point with this one.

@Johnny- you seem to ignore the fact that when banks are taken over by the government (fdic/ots/occ) the impetus for that action is to protect the depositor’s funds.

FDIC is acting to protect the individual account holder when they padlock a branch.

No one is arguing that the amount of leverage and lack of oversight was appropriate, but it is unbelievably naive to say that it would be ok for a major bank, (Citi, for instance) to be allowed to go bankrupt, or become insolvent.

And that misguided opportunistically socialist naivete is what irks me about the occupy movement.

Much of what we are railing against in 2011 (cheap money, policies emphasizing home ownership, etc..) were honorable programs in 1999. They were created to help people buy homes, who, lezzbehonest couldn’t, and probably SHOULDNT be homeowners.

The american dream is beautiful, but its not and shouldnt be guaranteed.

The reality of the matter is that homeowners who have no skin in the game (whatever the cost of the property, and whoever built it) have no motivation to keep making payments. Its economically more beneficial to walk away.

I have no sympathy whatsoever for a lender who doesnt have their docs in order.

I’ll even go a step further. Bravo. Good for her for getting over on a stupid lender. Good for her for exploiting a social program that she may not even need.

And shame on us as a society for allowing our leaders to screw the pooch on oversight of otherwise valuable social programs.

There was a story about an 8 figure home foreclosure in atherton, owned by a corporation as an investment. In the course of the proceedings, the aoi listed the business of the corporation as “recycling paper products (such as loan documents) into toilet paper”

bravo.

a wise man once said: If you borrow enough money, eventually, you own the bank

These individuals that used their homes as ATMs and then defaulted on their loans should be prosecuted for fraud and or grand theft.

It doesn’t matter if they spent the money on medical bills, took a cruise around the world, or donated it to the red cross. they borrowed the money, plain and simple.

I wish OWS and their supporters, as well as the news media, would do their homework in regards to the details of these foreclosures.

For instance I would like to know if some portion of the $590k was due to inflated loan fees/ points that may have been tacked back onto the loan by unscrupulous brokers that may have been complicit in this scam.

hard to imagine that this place was ever worth 590k total, even at its peak.

It WAS worth $590K. That’s exactly how much she extracted by owning it. If the bubble had gone on longer, she might have gotten even more. I’d pay $590 for a free ATM card too.

In the end, that’s was the basis on which people started valuing houses. It was exactly the right way to value them.

Here’s a newsflash: it’s no longer the right way to value them, but the people who valued them that way are mostly still in them, artifically reducing the supply for a while, and keeping the market from discovering the true value, which the people in Japan discovered, when their bubble popped, wasn’t as much as they thought.

This home is a prime example: it has been withheld from the market for years, paid for by borrowed money, not earned money and then not paid for at all. It will be many more years before all of these people are gone. In the meantime, prices will continue to fall just like they did in Japan – there isn’t any other alternative, because the homes have to fall to the point where productive people can afford to buy them, and we built a ton more than can ever be supported at anything near the currently inflated prices.

The relative strength in sales at current levels absent the poor / predatory lending standards would suggest we found some sort of a plateau. Maybe we get the double dip, maybe we do not. This is just more fallout from the subprime / nodoc era that will continue for quite some time. It will depress the market but I’m not convinced there is enough pent up supply like this one to crush the market.

@lyqwyd:

“The foreclosure fraud is a good example of rampant illegal activity which has gone un-prosecuted. Perhaps my info is out of date, but the last I heard nobody of any importance has been prosecuted, despite loads of evidence of blatant & systematic fraud.

Comparing the current crisis to the S&L scandal highlights how little effort has been made towards investigating and prosecuting potential crimes this time around.

The rule of law in the U.S. is basically dead. The powerful do not have to follow the laws anymore.”

Names, places please – just the facts.

Why do these few folks get to stand in for the Occupy Wall Street Movement?

I’m sure this has been addressed somewhere in this lengthy comment thread, but I think the editors are playing fast and loose with OWS. This is a small, confrontation-oriented faction, and clearly not a very bright one.

I think the editors are playing fast and loose with OWS. This is a small, confrontation-oriented faction, and clearly not a very bright one.

I agree, but you’re in the wrong place if you’re expecting even-handed treatment of OWS here.

“I’m sure this has been addressed somewhere in this lengthy comment thread, but I think the editors are playing fast and loose with OWS. ”

You can indeed see above that these examples were picked by Occupy Our Homes which ties itself to OWS.

This was a national event with a good bit of media coverage. Can you point to comments or statements by OWS leaders or supporters trying to distance themselves from OOH?

w.r.t. timeframe for subprime working through the system, note that the Quesada homeowner from the ABC local link first missed a payment in Jan 07.

I intended to try and estimate foreclosure timelines for the two ACCE(ACORN) anecdotes, but it seems sfgate rewrote their story.

The above link used to be titled “Bay Area protesters join ‘Occupy Our Homes’ day” and is now retitled ”

Occupy Oakland protesters focus on home foreclosure” with no anecdotes.

Unclear if this was a rewrite or retraction, but a news summarizer site got a hold of the original:

http://www.thedailyglobe.com/article/2375437/5703-bay-area-protesters-join-occupy-our-homes-day-12-06-2011-4-33-pm

@wrath

“Names, places please – just the facts.”

I’m not really sure who’s names or what places you are asking for, but here’s some facts about foreclosure fraud/ robo-signing:

http://www.dailyfinance.com/2010/10/02/robo-signing-scandal-spreads-documents-show-citi-and-wells-also/

http://en.wikipedia.org/wiki/2010_United_States_foreclosure_crisis

Robo signing is pretty well documented. Perhaps there’s been some important prosecutions, but so far the only thing I’ve found is a few mid-level people.

Foreclosure fraud is well documented. If you think I’m wrong provide some evidence showing that there’s no large illegal activity.

Jon Corzine and MF Global is another example that bears watching. It’s still farily new, so maybe he’ll be prosecuted, but I’m not holding my breath.

Looks like the big lie needs to be stamped out here, too; the big lie being that the bubble (and subsequent crash) were caused by congressionally mandated minority lending programs. Here you go:

http://www.ritholtz.com/blog/2011/11/examining-the-big-lie-how-the-facts-of-the-economic-crisis-stack-up/

“Looks like the big lie needs to be stamped out here, too; the big lie being that the bubble (and subsequent crash) were caused by congressionally mandated minority lending programs.”

Like the foreclosure paperwork issue, this is another red herring.

Borrowed money that isn’t repaid has to come from somewhere. Banks and or government are middlemen who take a cut, but the bulk of the burden goes to depositors, taxpayers, stockholders and bondholders. For the last two, consider that pension funds are often the ones holding the stocks and bonds.

I don’t think the people described above care about who takes the eventual hit nor the mechanics of how their gain is transformed into other’s losses (big banks, small banks, government or even the people’s committee on housing credit).

How many people who are “protesting the banks” send a check to the Treasury to compensate their fellow citizens for losses incurred to FHA or Fannie/Freddie?

lyqwyd–

It appears the Nevada DA is doing a real prosecution, flipping low level types to get the higher-ups. So far the first underling was found dead, on the day she was to receive her plea-bargained sentencing (one year, suspended). Yesterday they announced the indictment of three new underlings. Hopefully they’ll take depositions before sentencing on these ones.

@tc_sf

are you saying the foreclosure fraud issue is a red herring? I strongly disagree. It’s not the root cause, but it’s a pretty major symptom (but definitely not the biggest), and failing to pursue prosecutions would be an even bigger symptom of the problem.

@Delancey

I saw that, and we’ll see how it plays out. We don’t yet know if that death is foul play. They are not investigating it as a homicide, but it certainly seems suspicious. On the other hand it could just be coincidence.

But as my first linked article pointed out, we are 4 years into the crisis, and only a fraction of the actions taken during the S&L scandal have been done so far, even though this crisis is orders of magnitude bigger than the S&L scandal, and the root causes have been completely ignored, and in many ways made worse (TBTF banks are only bigger now).

lyqwyd, agreed. The dead witness just makes the Nevada prosecution sexier. The real story is that one of the states is actually prosecuting.

tc_sf, focusing on the moral weakness of individual borrowers is your personal red herring. It gives you clarity for a complex crime and lets you have a good harrumph. Me, I want to see jail time for the individuals who created the perverse lending environment and pocketed 8 figure bonuses apiece on phony profits. Because if none of them go to jail, this will happen again. (some would say it’s going to happen again regardless, but I would argue some jail time would delay the next great theft a couple decades)

“robosigning” or some other such “trendy” catchphrase may be negligent but you did not show it’s criminal. In any event, you should show where the people being asked to pay the mortgage have, e.g., already paid it off.

The fact that a bank can’t find the note does not mean that the individuals did not take the money out and didn’t pay.

but the bulk of the burden goes to depositors, taxpayers, stockholders and bondholders.

Let’s not forget, it could’ve been much worse. Many of the losses were shipped overseas via securitization. Without the MBS machine, none of this would’ve been possible.

UPDATE: The Details Behind Yesterday’s ‘Day Of Action’ Home In San Francisco

“are you saying the foreclosure fraud issue is a red herring? ”

Look at the timing.

“November 2006, Gage took out a $525,000 adjustable rate mortgage that started at 11.99 percent.

Her first payment was due two months later, but she never made it. She didn’t pay the next month, nor did she pay the following month.”

How can you think that defaulting on the first payment months after getting half a million in 2007 could be related to any title issues banks would be having nearly five years later.

The lag on the 1479 Quesada detailed by the editor looks to be three years and in general the forclosure timeline is so long that I don’t see how any current title issues could be causal at all.

Another way to look at it is to consider how many of the above borrowers will be cutting a check to the bank after any potential title issues are solved.

@wrath

The first link I provided in response to you points out actual fraud. Fraud is criminal. Delancey pointedc out several prosecutions in Nevada for criminal fraud.

The issue is not whether the person took out the loan. I have no problem with somebody being foreclosed on for not paying a loan they took out. The issue is that many foreclosures were done using forged or illegal prepared documents. There is evidence of 100,000s of thousands of fraudulent documents.

The banks or their contracted companies did 2 pretty big things wrong:

1) Lost documents and then transferred mortgages without recreating the documents in the appropriate manner, thus breaking the chain of title. This was not criminal, but it was illegal.

2) Much worse is that they falsified paperwork. Some of it was through negligence, and some appears to have been done in an attempt to cover up point 1 above. This was fraud, both illegal and criminal.

I’ve already given you links covering this issue, and it’s pretty well documented (by the way, this is not a trending topic, it’s already come and gone in the public eye, but the issue remains).

Here’s a video from 60 minutes covering the issue, including forged documents used in an attempt to foreclose.

http://www.youtube.com/watch?v=eClDqlPgBRg

You think it’s wrong it’s your time to provide some counter evidence.

@tc_sf

I’m not sure I understand what you are saying. I may have missed something, but I don’t think anybody suggested foreclosure fraud has anything to do with this property. I’m discussing it in the general, not in any relation to what is going on with the Quesada property.

“I may have missed something, but I don’t think anybody suggested foreclosure fraud has anything to do with this property.”

See “johnny”‘s posts above. The other homeowner, Vivian Richardson, called out the foreclosure as illegal and the one above tried to sue in federal court and “lost for failing to state a relevant claim.”” To the point above that people were not getting their day in court.

That;s what I meant by red herring. That both this issue and anything about congressional programs were not relevant to any of the OOH cases discussed above.

” I have no problem with somebody being foreclosed on for not paying a loan they took out.”

Then even if there was an error that rose to the level of fraud, is the victim not some other bank rather then the homeowner?

@tc_sf

Then it sounds like we were talking about two different things. I misunderstood what you were referring to.

Regarding the second issue, yes the “victim” was some other bank or investor or what have you. I’m not really concerned with who is the “victim”. I’m concerned with the system being so broken that hundreds of thousands of mortgages can be fraudulently transferred, and that this is only 1 of many problems in the system, and in my opinion a relatively small issue, compared to some of the other issues out there, such as the Citizen’s United ruling, TBTF banks being bigger, legislative capture, etc.

The issue with foreclosure fraud/ robosigning is that the fraud was conducted in a blatant and systematic manner, and now that’s it’s public knowledge there is no serious investigation, and many government agencies are trying it sweep it under the covers.

@lyqwyd

assuming there were forgeries, if the person actually took out the loan, why do you care?

isn’t the forgery a red herring to distract from what otherwise would be a clean foreclosure? I mean, is there evidence of foreclosure where full payments were timnely being made on the mortgage? In that situation did anyone get kicked out of their house?