“Nearly 40 percent of homeowners who received a loan modification that reduced monthly loan payments by 20 percent or more were at least two months late again within a year…”

UPDATE: A plugged-in reader comes through with a link to the original report.

∙ Borrowers with modified loans falling into trouble [The Associated Press]

∙ 9% Of HAMP Eligible Delinquent Loans Modified, 91% To Go [SocketSite]

∙ OCC and OTS Mortgage Metrics Report: Third Quarter 2009 [pdfdownload.org]

What’s the deal with the confusing newswire pieces on this subject? Once again it seems to be talking about different topics. There’s HAMP, there’s HAMP’s relative ineffectiveness, and then there are other mods. Here they cite 31,000 HAMP recipients. What percentage of that 31,000 got 20 percent monthly payment cuts? Because it’s been reported that some HAMP recipients didn’t even get a reduction. ? Even if it’s 31,000 X .40, it’s 12,400. Practically nothing. Odd. Why bother? Oh. That’s right. To sell papers.

Seems no one every learned from ole King Canute

The blurb would have you believe that it’s an irrepressible tide. Wouldn’t it? Placing it in the context of this blog and repeating the 40 percent of 20 percent reduction would make it seem like this is a significant trend, woulnd’t it?

If you read about HAMP, you’ll gather that it’s probably more like 1/10 of 31,000 got a 20 percent reduction. Forty percent of them are delinquent. That’s like 1000 people. This is continually some of the weakest reporting I’ve seen. What’s worse, these wires get grabbed and talked about on blogs, sometimes by big names. People walk away with ideas that aren’t even conveyed. The scare words are much bigger than the event.

Sort of like how someone can pull out one number (say 31,000) and misuse it as the total number.

31,000 is the number of modifications that have been made permanent. It is a poorly written piece, on that I will agree. But there is nothing there for you to support the conclusion that the number they are referring to is 40% of 1/10th of the 31,000. It is entirely possible that the 40% number includes people that are delquient on modifications that have not yet been made permanent (and will therefore not be made permanent since one of the conditions is for a permanent modification is to make the modified payment for 3 months).

So, yeah I agree with you that people shouldn’t be using these numbers to make assumptions like your assumption that this is only 1,000 loans.

Have you read about what the HAMP mods first iteration actually wound up being? A lot of them didn’t even get reset to lower payments. The notion that a great deal of them were reset to 20% less than previous isn’t supported by anything I’ve seen about HAMP. So that’s where I’m coming from, there. But even if you want to take the numbers totally straight it’s a drop in the bucket.

Of course, instead of just yammering away, rotely criticizing everything that indicates a continuing downturn, or making up hypotheticals that would explain away such indications, one could actually read the readily-available source material.

http://www.pdfdownload.org/pdf2html/view_online.php?url=http%3A%2F%2Ffiles.ots.treas.gov%2F482114.pdf

But it’s far easier to just shout “You’re an idiot.”

Nobody called anybody an idiot, anywhere, except for your rote — yes, rote, because you always come at me the same way — paraprhase. Skip down to “Modified Loan Performance” in your own link, and see that delinquencies for the the later iterations of modification programs are actually DECREASING. Why? Probably because they’re actually now significantly lowering payments. The older iterations weren’t even lowering payments, and folks were saying “screw this.” Reference page 6 from your link.

Huh, what a shocker, and thanks for the report, anon@12:25PM. The data show that both HAMP and non-HAMP loan modifications are extremely likely to re-default, which is what I said earlier. Poorly written pieces in the news, sure, but the data are clear.

Note my four points on this thread: https://socketsite.com/archives/2009/12/rent_versus_buy_default.html

Where do you get “extremely likely” ? The trend is the opposite. The most recent quarter examined 2009 shows a decrease in seriously delinquent mods. This has been trial and error.

That’s a horrific redefault rate. This is a disaster: even the people getting 20% lower payments are defaulting en masse.

There’s no hope. What a catastrophe! Etc! Etc!

I mean, the conclusion drawn is, I quote: “This lower three month re-default rate may be an early indicator of sustainability for loan modifications that reduce monthly payments.”

Meaning, basically, the old mods weren’t reducing payments very much. And often not at all. People weren’t happy with that. Their mentality was not changed. They were resolved to bail out before, and so they bailed out again.

This is pretty much what I’ve said in every single thread on the topic. Where you get “extremely likely to default” when the report you’re ostensibly trying to pass off as having read ad summarized is not known.

The AP story linked by editor is an early version; it has since been re-written into a longer and (somewhat) more useful piece: http://www.usatoday.com/money/economy/housing/2009-12-21-foreclosures_N.htm?csp=34

This article mentions at the end that the signs of re-default are improved — 20% of modified debtors have missed two out of three payments, compared to 35% earlier. That appears to be a positive trend; however note that (1) the original debtors who modified may have been worse off, and (2) 20% is still rather high.

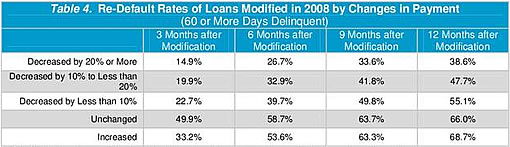

Per anon 12:25 pm’s link, almost 40% (38.6%) of mortgages that are having payments slashed by 20% or more are 60+ days delinquent again within one year. There are at least 20,000 of these modifications. This compares to 66% of “modified” mortgages that have no change in monthly payments being 60+ days delinquent within one year.

So you do buy a 27 pct pt reduction in delinquencies, though at a cost of shaving 20+ percent off of payments. Thus, unless the length of the mortgage is greatly extended or the modification is only temporary, it will not be in the lender’s best interest to reduce payments by 20+ percent (unless the property is ridiculously underwater).

Horrible written blurb article is horrible. Thank you for posting the link to the full report. No thank you for saying people were calling each other idiots on this thread when that wasn’t happening.

Imagine that, folks adopting the same attitude as the banks who gave them the loan:

Brent White, an associate law professor at the University of Arizona who has written about this issue, says homeowners should make the decision on whether to keep paying based on their own interests, “unclouded by unnecessary guilt or shame.” He says borrowers can take a cue from lenders that “ruthlessly seek to maximize profits or minimize losses irrespective of concerns of morality or social responsibility.”

“This article mentions at the end that the signs of re-default are improved — 20% of modified debtors have missed two out of three payments, compared to 35% earlier. That appears to be a positive trend; however note that (1) the original debtors who modified may have been worse off, and (2) 20% is still rather high.”

That 18% re-default rate (you rounded to 20%) for 2009Q2 loans is for 60+ delinquent. That jumps to 34% for 30+ delinquent, which is still better than prior 45%-55% re-defaults for older loans at the same age. Let’s see what happens at 9-12 months when it really matters — the gaps have narrowed for older vintage modifications at 9 months.

In the very short-term we have seen some improvement for 2009Q2 modifications, but a significant number of people are still re-defaulting very quickly. The modifications early on were hitting up to 70% re-defaults (30+) after 12 months. Even modifications with 20% lower payments are approaching 40% re-defaults at 60+ at 12 months and exceeding 40% at 30+ at 6 months.

Furthermore, we have no idea why fewer of those loans have defaulted — it could be mix of loans (note that portfolio loans have a lower re-default rate, whereas private + government-guarantee + quasi-government-guarantee all have much higher re-default rates) or higher payment cuts or more principal reduction or something else.

Option ARMs aren’t performing particularly well — almost 1/3 are 30+ delinquent or worse.

Also note what some of the “home retentions” actions are — only around 13% currently involve principal reduction, although most of those are in portfolio loans, which explains why portfolio loans are performing better. But principal reductions aren’t saving Option ARMs, even though they have more principal modifications relative to other loans.

“Extremely likely to default” is how you termed a decreasing trend. “Big shocker,” you said. Then you concurred that it’s actually decreasing and went on to theorize wildly.

70% redefault rate at 30+ days delinquent at 12 months isn’t “extremely likely to re-default”? Whatever, dude. No theorizing necessary when the data’s on my side.

I don’t know how many times you need to hear this to understand it, but here it is again. Defaulting on what? What really were these so called first iteration HAMP “modifications” from 2008? They’re defaulting on loans that weren’t modified. It’s in the report you said you read. It’s in the links you throw up. Know it. You’re mixing up timeframes and schemes when you throw out your blanket statements. Cut it out.

I mean, your 70 percent number is from an increase! No wonder they defaulted. Come on man. Really now. The data reads that decreased rates, and furthermore decreased principal in the case of portfolio’d loans, are showing lessening signs of default moving forward. You can holler about “Small wonder! This’ll never work!” and link to first gen HAMP all you want. It’ll remain disingenuous. This is the third, and last time I’ve had this argument with you. Read what you link to.

As usual, you can’t point to anything specifically wrong or say anything substantive, but yet you criticize what I said. And I’m talking about both HAMP and non-HAMP numbers, as usual, and you’re still obsessed with HAMP because that failed program is the only thing you can criticize.

I encourage everyone else to read the report themselves and draw their own conclusions.

For me, it’s pretty clear that recent vintage modifications have done better in the short-term (i.e. within 90 days of modification, even though still 35% delinquent), but that has happened before when modifications became slightly more aggressive, and the cracks started showing up at 9-12 months. We’ll see in a few months if we’re getting extremely high re-defaults again at 9-12 months or if these recent modifications will hold. But I’m not holding too much faith when they’re already at 35% 30+days delinquent.

That act is tired.

In this thread I supported my correct points by not only directing you and others to a specific page in the report, but quoting directly from the report.

For your 12 month 70 percent figure, I now direct you to the top of this page. Look at the lower right hand corner. See “Increased.”

Your theorizing about “that has happened before when modifications became more aggressive” doesn’t have merit. This is all quite new. The numbers you quote are always from 2008. It’s been trial and error, tinkering and implentation; a gradual shift toward actual, streamlined interest rate reduction.

Read pages 20 through 37 of the report, especially 31, which I’m quoting, and then get back to me on whether you see 70% or not. In no way am I relying on the chart at the top of this post.

If you check out the chart on page 31, you’ll see 70% re-defaults at 12 months. And you’ll see that even the slightly more aggressive modifications from 4Q2008 which showed a 10% improvement at 90 days, ended up the same as 2Q2008 and 3Q2008 at 9 months, and 1Q2009 seems on the same trajectory.

You keep talking about HAMP 2008. I rest my case.

Once again, that’s not HAMP. Last check, the Obama administration rolled out HAMP in March 2009. But nice try at obfuscating the real issues.

Again with the 2008 as trend idea. What did those Q3 2008 loan mods actually look like to borrowers?

I obfuscated nothing. On the other hand, you’re using conclusive language based upon results of past programs — programs that have since been modified or yes, named and renamed. Do you see me making predictions here, or talking about what has occurred? The strongest word I used was “trending.”

By the way, on page 31, what are the nature of the re-mods discussed?

I leave it to judge for our readership whether I have been any more conclusive than you have. Done with you here — you, again, aren’t really saying anything constructive here other than “you’re wrong” without being able to back anything up.

You guys are arguing over the crumbs. Maybe an extra 1000 mortgages per month are being saved. 20 per state. Hooray…Not

Most people don’t and won’t qualify.

Property prices were rising, so the people I know who got caught up in this bought more house than they could afford to use the leverage to make as much money as possible. Living expenses were charged to credit cards and their incomes paid the mortgage and the minimum balance on the cards.

Periodically, they refinanced, took cash out, paid off the credit cards and started over. This caused higher payments which they could no longer afford, so they dropped down to interest only, and then option arms to get more and more money out but keep their payments the same.

They can neither refinance nor get more credit cards any longer. You can cut their mortgage payments by 20% and it doesn’t matter: they never had the money to make the payments in the first place, and now the mortgage is also financing several years worth of living expenses.

The modified mortgages are essentially crack to crack addicts. They’ve been robbing peter to pay paul for the last 5 years and the trial modifications are merely an extension of that technique. They stop paying the mortgage when they are simply out of options, and the bank gives them an extra 3 months to document income they don’t have and will never have. This is just what they have been doing for years.

During the time they stop paying their mortgage, they finally have money to start to pay down the balance on their credit cards and some money for living expenses. Having had a taste of how much better life is like that, the end of the bill collectors, the end of the stress, they go back to it and stop paying their mortgage. It’s just so much better than paying it.

And that’s how they redefault. You can drop principal (and bankrupt the banks when they have to recognize the loss) but it won’t matter. Most people will not qualify for a permanent mod. THEY DON’T HAVE THE MONEY AND NEVER DID. The few people who do qualify, and how many of them survive is basically irrelevant in the sea of people who will never qualify. The whole thing has been a ponzi scheme, with one bank paying off the next one. Bernie Maddoff to the power of a thousand.

anything constructive here other than “you’re wrong” without being able to back anything up.

How can you say that? I shed light on the prevailing trend. I showed that the early iterations weren’t even reducing payments. I correlated to nonpayment. And on and on. Now you’re using overarching, dismissive language on what I’m saying. Get a thesauraus already.

Summary:

SFrenegade: These numbers are bad.

Annon: They are getting better.

A dozen posts of bickering. Another socketsite classic.

I’d disagree with that summary. You’re leaving out that I’m asking how were they possibly supposed to be any good before. It went something like this: “Sweet! My loan mod is in! Oh. I’m paying the same? Someone else, a tiny bit less? A third guy, MORE MONEY? In unison ‘Screw this.'” Fronzigade looks at old numbers and wants to say what the future will be like. The amount of significant reductions from 2008 was miniscule by comparison to now. And that’s all.

I’d disagree with that summary.

Really? Shocking! Who could have ever guessed that you might do such a thing?

I wonder if you read this thread and noticed how I am capable of making points sans sarcasm. I disagreed with Rillion a few times without being snide about it. Maybe you can read my writing and learn something very important that you can utillize throughout the rest of your life. Food for thought.

anonn, summaries will always lack the fine details of the actual material, that is their nature. But in my defense I do think “they are getting better” incorporates some of your point that the prior modifications were inadequate and that the newer ones are getting better, hence the default rates are getting better.

Maybe you can read my writing and learn something very important that you can utillize throughout the rest of your life.

Sure, stranger things have happened. What would really surprise me, though, is if you began to understand the irony of some of your own posts.

I would be more surprised if you actually used irony properly in a sentence.

Loan mods will not work unless there is significant principal destruction along with the payment reduction. HAMP will work wonders once there is enough loss acknowledged on the lender side. Prices have gone down and are not coming back this time. Owners know this. Banks know this. Both are acting accordingly.

I would be more surprised if you actually used irony properly in a sentence.

I rest my case. 🙂

Hard to say if it will continue to get better on the loan modification front. After all, anyone remember the post from a few days ago on how jumbo-primes have worse default rates as time goes on? The 2008 cohort is already worse than the 2005-2007 cohorts. That doesn’t bode well for their potential modifications either.

https://socketsite.com/archives/2009/12/more_along_the_lines_of_a_figurative_san_francisco_tsun.html