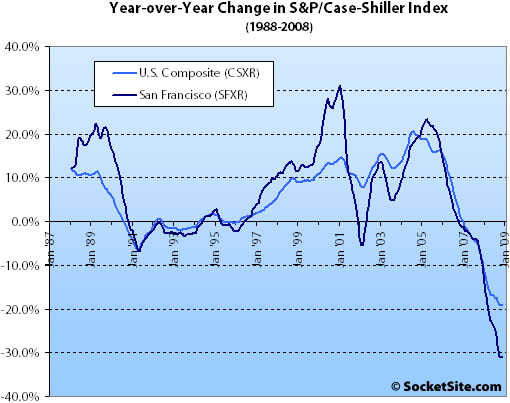

According to the November 2008 S&P/Case-Shiller Home Price Index (pdf), single-family home prices in the San Francisco MSA fell 3.0% from October ’08 to November ’08 and are down 30.8% year-over-year (down 31% in October). For the broader 10-City composite (CSXR), year-over-year price growth is down 19.1% (having fallen 2.2% from October).

All 20 metro areas, and the two composites, posted their third consecutive monthly decline. In addition, eight of the MSAs posted their largest monthly decline on record – Atlanta, Boston, Charlotte, Chicago, Dallas, New York, Portland and Seattle. Although in decline over the past few years, some of these regions have out-performed on a relative basis, when compared to the national average. It is clear, however, that the decline in home prices is affecting all regions regardless of geography or employment opportunities.

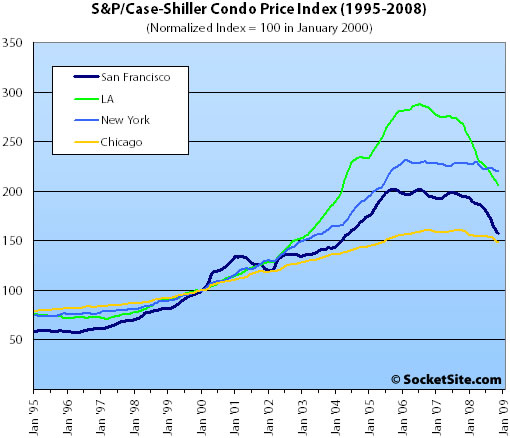

Condo values in the San Francisco MSA also continued their decline falling 2.7% from October ’08 to November ’08, down 19.2% on a year-over-year basis and down 22.0% from an October 2005 high.

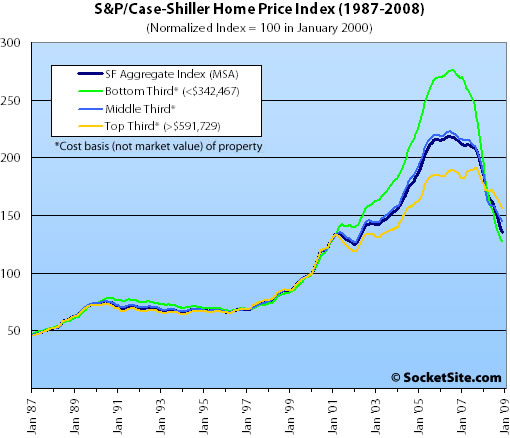

And San Francisco MSA single-family home prices once again fell across all three price tiers.

The bottom third (under $342,467 at the time of acquisition) fell 2.2% from October to November (down 40.2% YOY); the middle third fell 1.6% from October to November (down 26.9% YOY); and the top third (over $591,729 at the time of acquisition) fell 1.9% from October to November (down 14.6% YOY).

According to the Index, single-family home values for the bottom third of the market in the San Francisco MSA have retreated to December 2000 levels, the middle third has returned to February 2003 levels, and the top third has fallen to June 2004 levels.

The standard SocketSite S&P/Case-Shiller footnote: The S&P/Case-Shiller home price indices include San Francisco, San Mateo, Marin, Contra Costa, and Alameda in the “San Francisco” index (i.e., the greater MSA) and are imperfect in factoring out changes in property values due to improvements versus actual market appreciation (although they try their best).

∙ Home Price Declines Continue/Home Prices Indices Set New Record Annual Declines [S&P]

∙ October S&P/Case-Shiller: San Francisco MSA Down Across The Board [SocketSite]

We’re at a point now where — in the last ten years — condos have exhibited a CAGR of only a few percent annually. Now, I know that the bears will point out that typical housing appreciation is low single-digit percentsages, and that this is, at best, in line with where it SHOULD be…

… but still. If you guys think that condos in the city are going to fall another 20%, then that’s just over the top. There have been strong, legit reasons for growth in SF over the last decade, and condo values should be noticeably higher than they were in 1999.

Any more decline would equate to an overreaction.

SNB, the slope of that graph isn’t flattening.

Go ahead and call the bottom, near the bottom, whatever, but as long as jobs are being lost, we’re a long way from the bottom. And how many jobs disappeared yesterday? At least a hundred thousand. In any economy in which more than a hundred thousand jobs can disappear in a single day, I can predict with 100% accuracy which way real estate prices are going.

What is the difference in the rate of change of the prices going up vs the prices going down? Down already looks like a much sharper, faster line….

SNB, growth doesn’t matter all that much if it isn’t income or population growth, which is more or less hasn’t been. The median income in SF is still in the low 50s. Even in a very poorly planned city like SF (price increased because demand cannot be met), median home prices right now still look unsustainable if credit stays tight (as it very much should). That’s not even taking into account the recession. The graphs for median home prices in Tokyo and urban japan from the 70s – 90s are instructive. This is not the first housing bubble to happen this century.

I think we will be going into overreaction, because this is how averages are built. But this is not the current situation. There is still a big bubble to pop in some areas where the expectations were too high too long. 20% more to go? I think so, but then again we’ll see in 2-3 years. This economic downturn is still in its infancy and the effects of mass layoffs haven’t impacted all of us yet (though 2 of my friends at MS are in serious trouble).

The long trend I believe is that SF RE will always appreciate if you look 20-30 years down the road, and so is every place where population goes up and new wealth is produced. SF has a lot going on for it on so many levels. Not top shelf, but right next to the big guns.

I hope we will have less intense bubbles/implosions in the future, though. Of course we need bubbles to unlock sleeping money (or debt, it’s more and more mistaken for money…) and build new property. The devastation in the wake of the Great 01-07 Bubble is huge. Too many people are burnt. Had we stopped this bubble in 2003 we’d be in much better shape.

Just to add: On all these graphs, the dot.com bubble effected housing prices between Jan. 1999-Jan. 2001 quite noticeably. How will that additional boost in prices to SF, that the nation obviously did not experience on the same level (according to the graphs) effect our housing price downturn?

San Francisco is rich–really rich. So is NYC, Chicago, Palm Beach and Boca Raton….

Let’s see what happens…

In addition, eight of the MSAs posted their largest monthly decline on record – Atlanta, Boston, Charlotte, Chicago, Dallas, New York, Portland and Seattle

This is telling. Several of these cities were the last bastion of hope for “it’s different here”. specifically Charlotte, Seattle and Portland and Dallas, that had avoided losses, and even shown gains, until recently. The Pac NW has lagged the rest of the country. Until now.

Also, Boston was one of the first MSA’s to drop, but then held steady. It is intriguing (but who knows if it matters or not) that Boston is dropping quickly again.

One last thing:

I often hear about how SF is different because it’s core areas are holding up while the outlying areas are suffering. This is what is happening everywhere.

Central SD is holding up better than outlying SD county as example.

SNB – You can check the Chicago Mercantile Exchange (CME) Case Shiller Index (CSI) futures for the San Francisco Metropolitan Region (SF MSA) here.

http://www.paperdinero.com/CSI.aspx

There is no sign of flattening at least through May of 09 according to the futures. Mr. Shiller was speaking on CNBC and stated that the futures contracts did not predict a bottom, nationally, until mid 2010 or approximately 18 months from now.

Of course the SF MSA Could turn around sooner, but expect a continued decline for the foreseeable future.

Wait, I thought we called last week The Bottom? So what’s today, the Super Bottom?

There, I said it. We’ve reached the Super Bottom.

Wait until next month to see if we hit the Ultra Bottom, the Mega Bottom, and the Super Duper Bottom.

You’ll be seeing more bottoms over the next two years than you would at a vegas lounge act.

“Noe Valley ZIP code 94114 was among the few in the Bay Area where home prices were up in November. (Michael Macor / The Chronicle)”

http://www.sfgate.com/cgi-bin/article.cgi?f=/n/a/2009/01/27/financial/f060156S62.DTL&tsp=1

Anybody have more info on this blurb from the Chronicle?

There have been strong, legit reasons for growth in SF over the last decade, and condo values should be noticeably higher than they were in 1999.

this line intrigues me. Fluj would sometimes use a variant of this argument (at least, I took it as a variant of this argument) what are some of the strong legit reasons why SF should cost more in 1999 than 2009?

1999 saw a major internet bubble that was centered on San Francisco. Thus, SF RE was influenced by that .com bubble. thus, one could say that SF RE was bubble-supported (which is different than saying it was in a bubble).

The bubble popped in 2001, but SF RE did not fall back down as one would predict given the loss of income from the .com implosion. clearly partly due to the credit/housing bubble that took over.

Thus, I have difficulty figuring out when SF RE was last at “normal” valuations. Should we use 1999, during the heat of the internet bubble? that seems odd to me. Should we use 1992 during the recession? I’d argue no again. how about 2002 during the recession? Or 1996 (post recession and pre-.com bubble?)

Regardless, I personally see no particular reason why SF RE should cost more today (in real terms) compared to 2000 when it was at the height of the .com bubble. I can see every reason why it should cost more (in real terms) than in 1992 when SF was in recession and it was before the great demographics shift.

Ex-Sfer: If SF real estate should cost more than in 1992, than it should cost more than in 1996, as home prices were about the same in those two years.

It is hard to say what prices “should be.” The prices in 1996 were a little lower than in 1989, so it makes sense that prices would rise once the economy took off again in the late ’90’s, even if in part to compensate for the years that prices did not keep up with inflation.

Also, from 1995 to 1998, interest rates dropped substantially– I refinanced from 7.75% in 1995 to 5.75% in 1998, and interest rates remain much lower than they were before the past 10 years of appreciation.

I think ex-SFer means what are the reasons that SF RE should cost more in 2009 than in 1999?

Dan:

I don’t disagree with you. my questions were more rhetorical.

in the end SF seemst to have been a boom/bust RE market for at least the last 20 years. this makes finding “true” valuation difficult.

one shouldn’t use recession years (1992) as the baseline, and one shouldn’t use boom years (2000) either…

so the likely answer of non-bubble/non-bust valuation would probably be sometime between 1992-2000. thus my rhetorical question.

I use 2000, because I feel that I KNOW that RE was highly valued in that year. I also BELIEVE that there is little different demographically between 2000 and 2009 (income, population, etc). Thus, I have been trying to ask why people feel 2000 pricing isn’t possible.

in other words, why do people feel that SF today is worth more than SF at the height of its .com bubble?

==

as for the intest rate issue: several things have changed over the years. interest rates are just one. A bigger one IMO is the mortgage interest rate deduction that came about in 1997. I forget when the exclusion on taxes on capital gains in housing was passed, but that also had a role.

A bigger one IMO is the mortgage interest rate deduction that came about in 1997. I forget when the exclusion on taxes on capital gains in housing was passed, but that also had a role.

I think the mortgage interest deduction has been around for decades. In the 1986 revisions to the Code, mortgage interest got special treatment because it remained deductible, while other forms of personal debt (credit cards, auto loans) lost their deductibility.

The capital gains tax exclusion (250K/500K for principal residences) came about in 1996.

Just two examples of the distortive policies of the USG that have now come back to bite us.

SF has the other, very large, distortion of Prop 13 since 1979. This is a very big deal in SF, but is not such a big deal in other parts of California where the housing stock is newer (significant percentage of the stock built in the 1980s and later) and the restrictions on growth were not as severe.

I actually think 1995/96 prices in SF were still a little bubbly (for their time) and would have continued to correct (at least in real terms) had not the credit/finance bubble heated up in earnest during the second half of the 1990s.

What’s that old saying…

“Which house is your primary residence?”

“The one that I’m selling.”

And I saw when the Lamb opened one of the seals, and I heard, as it were the noise of thunder, David Lereah saying, Come and see.

And I saw, and behold a white horse: and he that sat on him had The Exemption; and two hundred fifty thousand dollars was given unto him: and he went forth conquering, and to conquer.

It’s pretty remarkable that the bottom third has fallen to December 2000 levels… and has every indication of continuing to fall. I expect the middle and top tiers to follow suit back in time to 2000… and if the middle tier travels back to the mid-1990s, so too will the other tiers. Eventually.

One can mount an array of arguments why the middle and upper tiers are “different” and shouldn’t suffer in equivalent fashion. I’m not a buyer of those arguments, although I do think they have some merit. Evan (at 7:48am above) suggests median prices will still suffer pressure “if credit stays tight.” I will quibble with that wording – credit now isn’t “tight.” It is more “normal” – if you want it, you have to be able to supply some equity toward the purchase and demonstrate the capacity to make good on interest and principal payments. On a relative basis – compared to the rank credit idiocy of the past XX months – it seems tight. But if you stand me in a pack of midgets, I appear to be 6’4″….

I use “XX months” above because I don’t know how far back to dial the comp-history. That is, I’m not sure how far back one must go to begin carving out prices that are grounded in the bedrock of “value.” First, any leveraged asset class that suffers sustained investor revulsion has no theoretical lower bound until it hits over-the-barrel cash-financing. I’m not saying we’re headed there, but that does define the theoretical bottom. Second, if we use a simple rent-v-own model, then the pricing of houses should relate in some manner to the discounted cash-flows available from them. I have seen no few number of formerly-available-for-sale homes get listed as now-available-rentals… and news reports are replete with accounts of renters having their rental foreclosed out from underneath them… which suggests that rental income on underwater “owners” is broadly insufficient to cover the carry on the asset. Which means some portion of these weak-handed rentals will eventually land on the market for sale in some manner of distress, further pulling down comps on which the banks rely for extending credit on the collateral.

Which brings us back to the first comment by SNB, who insists, “Any more decline would equate to an overreaction.” That’s just not true. The incapacity of owners to charge sufficient rents to carry the economic costs of recent purchases is tied to the earning capacity of available renters. If everyone in the Bay Area (as defined by Case-Shiller…) suddenly received an overnight 50% pay hike, then rents would be expected to drift upward to some meaningful degree, because that pool of renters would have greater disposable income to commit to housing. Such a hypothetical might raise rents sufficient to cover the economic costs of ownership. The same holds true, of course, for the purchase of Bay Area homes: double regional incomes overnight, and you’re going to see the price of housing appreciate.

But therein lies the rub.

It works both ways… which is why long-term housing prices are closely tied to regional income. I am not claiming that the Bay Area and San Francisco don’t “deserve” some sort of price-premium over Cleveland. Duh. But that premium must be tied to the long-term capacity of locals here to earn and pay it and/or to pass it on to the next generation.

This all matters for estimating a fair price for those (“bitter renters”) like me who can & would happily buy a house today that seemed reasonably priced. When possible, I have been conceptually willing to concede a 2003-era comp and grow it at a 3% CAGR to estimate what a “fair” price might be today. That 3% value is a casual proxy for regional income growth.

The problem is that in the vast majority of cases, sellers are using a CAGR closer to 10% in the places I see for sale with 2003-era comps. That is not economically defensible. And it will be surrendered over time. And more will be surrendered if there is any change in the willingness of new generations to absorb any regional premium.

Finally, however, if the lower tier is down to December 2000, with no appearance of having carved a bottom, and I expect the other two tiers to follow it (especially given the option-ARM wave), then I probably have to dial back my 3% growth allowance to 2000-era comps to avoid being among the current set of knife-catchers who are wading prematurely into the market.

And outside of foreclosures, you can’t find that sort of pricing yet.

SNB – The Dow closed above 10,000 in 1999. Historically, stocks have averaged around 7% real rate of return. This translates to a 10% nominal rate of return, or about 160% over a 10 year period (well, technically the index itself should rise somewhat less because some stocks are paying out dividends). So by your logic, the Dow should currently be around 26,000, and the fact that it’s currently around 8,000 means that we’ve massively overreacted. We should all quickly go buy stocks before everyone else realize that the Dow’s true value is 26,000!

It’s going to get worse. If I’m reading this right, FHFA just proposed cutting the GSEs investment portfolios by 70%.

Though I assume that number will get whittled down, even conforming loans are about to become harder to get.

http://www.bloomberg.com/apps/news?pid=20601087&sid=aNbCGUkGQ0b4&refer=home

I also BELIEVE that there is little different demographically between 2000 and 2009 (income, population, etc).

Median family income is up about 30% since 2000. The population is now officially 824k, which is about 6% more than in 2000. How much of this is true population growth is open for debate though, since Newsom challenged the census estimate for 2007 and got them to up the population count by 35,000. In any case, there are assuredly more people in San Francisco today than in 2000.

In any case, this would support the notion that home prices might be about 30% higher than in 2000, not the 50% or so that we see.

“but still. If you guys think that condos in the city are going to fall another 20%, then that’s just over the top. ”

for condos, i think # may be closer to 35% more. 20% is a given IMHO. I think the only condo buyers who are realtively safe from losing money are those who bought pre-2001.

RE apprecition should be 3% annualized from 1995 to now. No reason that SF is “different”

NVJ – Unemployment is also almost triple what it was in Dec 1999 (6.6% Dec 2008 vs 2.4% in Dec 1999). This is the highest Dec unemployment for SF since at least 1990 (that’s as far back as the statistics I found went).

The fact of the matter is that 2000 itself was at the peak of the previous bubble – as you can see in the graph above, average appreciation from Jan 97 to Jan 01 was actually higher than from Jan 02 to Jan 07. The assumption that 2000 asset prices were in line with fundamentals seems extremely suspect (see, for example, the stock market).

How much higher is median family income than it was in 1997 then? I don’t have stats for 1997, if you do, it would be great to see them.

Many variables determine RE prices, and in SF, I’m not even sure median family income is the most important, since most folks rent.

It would be interesting to see “median family income of families who bought houses”, but I think that’s hard to come by. Does anyone have that info?

“median family income of those who bought” is going to be a restricted group to those who are rich enough to buy; i don’t see how it’s significant.

I think the best stat would be % of families that can afford a median home — over time, that should be relatively constant.

% of families that can qualify for a median home:

2007/8: 100%

2009: way less.

[“median family income of those who bought” is going to be a restricted group to those who are rich enough to buy; i don’t see how it’s significant.]

Not true. Not everyone who bought was “rich” enough to buy. They merely had access to cheap and easy credit.

Instead of % of families that could afford a median home, it would be more interesting to see % of households in SF in various income brackets and compare that to % of homes listed for sales at various price points – – but I’m sure this data will be hard to come by.

% of families that can qualify for a median home:

2007/8: 100%

2009: way less

No way! Way cool, junior. Did you learn that from Mr. Peabody and his Way Back Machine?

NVJ

those are good reasons.

I have median household income up 18% and median family income up 27% from 2000 to 2007 bsed on the Bay Area Census.

I have population decreasing 19,000 people from 2000 to 2007 based on Bay Area Census

http://www.bayareacensus.ca.gov/counties/SanFranciscoCounty.htm

but those income stats are intriguing. Inflation over that time period was officially 20.4%.

http://data.bls.gov/cgi-bin/cpicalc.pl

so household income DROPPED on a real basis (20.4% inflation with only 18% income growth)

and family income increased on a real basis (27% income growth vs 20.4% inflation)

Nice to see fluj (anon 2:15 PM) is back! His distinctive style is typically evidenced by derisive personal attacks.

Getting back to the subject of this thread, the SF MSA is now almost 40% below its peak.

It’s hard to make forecasts, especially because the nature of the distortions that have occurred over the last 25 years make it almost impossible to identify an “equilibrium” starting point from which some extrapolations could be made.

That being said, though, I’ll guess that about 2/3rds of the nominal decline in the lowest price areas of the MSA (and the worst hit parts of SF proper) are behind us, but that the more desirable areas are only 1/3rd into their nominal decline.

Those “tier” lines in the chart are going to meet again, but at significantly lower levels for the highest tier. Probably by end-2010 is my guess.

Volumes are shrinking in SF, meaning that the number of lifeboats on the SS Innovation Mecca will not suffice now that the ship is going down. We’ll probably start to see a scramble for the boats after Q1 2009, continuing until Q3 2010, as people gradually recognize the scale and length of the bubble in SF property values (dating from the late-1980s, at least).

A derisive personal attack = poking fun at the very unscientific little flame that was “way less” ? No it wasn’t. And you know all about derision too. What with your avuncular trading persona versus your sardonic r.e. persona … a derisive spectre definitely takes over your keyboard. Interesting mislabel there.

Editor, why is fluj allowed to change his handle without being subject to the infamous SocketSite brackets?

aw man! really now, dude. If “dude” posted as “anon” I don’t think anybody would care one bit.Least of all the editor. Because the anonymous hatred is so fun, right?

We don’t need any brackets: it’s pretty obvious.

I didn’t take it as an attack: it was just his poking fun at my use of my admittedly unscientific quantifier, “way”. Bonus points for the way back machine reference.

Let’s move off this. He (or anyone else) can make fun of me if he wants, it’s all just good entertainment. I don’t take it personally.

ex SFer: can’t comment on the rest, but I can say that San Francisco population actually increased substantially during this period and we now most likely stand at a bit more than 800k. From the Planning Department who took the lead on the recount (which btw gets the City more $$$)

“Instead of the initial 764,976 estimate (for beginning of 2007), San Francisco’s count is officially 799,185 — or over 34K more.”

The link you posted uses those 2007 ACS estimates that were successfully challenged by the City (in fact the Census Bureau, who also produces the ACS, significantly undercounted SF population at least back to 2000).

So can I start using the fluj handle? Or what if “mean anon” starts using it?

I thought there was an unwritten SocketSite rule that regulars stick with the same nicknames for consistency. Makes no difference to me, though. You guys can call yourselves Craven Moorehead or Rod von Hewdgendong for all I care. But if folks want to fake their own blog death and assume a new identity, let’s maybe drop the old vendettas and vitriolic baggage from your former lives.

San Francisco has attained the highest population on record with a population of 824,525 on January 1, 2008. This continues the significant upward trend in growth that began in 2006. The city grew by 1.5 percent this year.

http://www.dof.ca.gov/research/demographic/reports/estimates/e-1_2006-07/

Case Shiller numbers are not inflation adjusted, so I don’t know why would inflation adjust the incomes we are trying to compare them to.

But I guess we agree, if for no reason other than inflation alone, home prices have an general upward bias. That bias should be about 20% since 2000.

“We’ll probably start to see a scramble for the boats after Q1 2009, continuing until Q3 2010, as people gradually recognize the scale and length of the bubble in SF property values (dating from the late-1980s, at least).”

Advance apologies if you have fielded this already, but is there something specific to which you date the Property Bubble Advent when you invoke “late 1980s”? I find it all hard to disentangle: general credit laxness, national property bubble, local property bubble, and the normal gains property deserves.

Greenspan (may the Gods condemn him to have his eyes pecked out by a vulture somewhere near Mt. Olympus for all eternity…) could create excess credit/liquidity/money/inflation through his reprehensible and epically irresponsible monetary policies, but he could not target its “benefactors.” And he didn’t seem really to go permanently around the punchbowl-bender end until mid-1990 – he made one last-ditch effort at responsibility by invoking “irrational exuberance” in his 1996 speech, but thereafter entirely caved to the new-economy/permanent-productivity miracle nonsense.

My feeling is that residential real estate as an asset class really didn’t absorb the easy credit stuff until ~1999, when the Fed was unnecessarily anticipating Y2K issues. But equities were the asset of choice in the run-up to 2000; only thereafter did the credit madness begin spilling into residential real estate in earnest. Even in the Bay Area, a link I posted last week suggested that Option ARMs still constituted less than 1% of refinancings as late as 2003 (I think) – that percentage had climbed to ~35% a few years later.

That’s symptomatic of the loose-credit blow off, which obviously had already been proceeding apace for some period of time. But I guess I hesitate to trace the bubble back as far as the late-1980s.

Ah, this is the height of irony. After months of complaining about anons, fluj has now become one himself.

Brilliant.

There was a real study, done with real data, and not people speculating and pontificating on RE blogs(I’ll try and dig up the link) that shows that from 1895-1995 house prices increased at the level of inflation – no more and no less! That’s 100 years! What else would the cost of housing be tied to? From 1995 on RE ran with the bulls in the stock market to the low oxygen elevations. If you want a real comp, go back to 1995, add in compounded 3% yearly inflation, and bingo.

Advance apologies if you have fielded this already, but is there something specific to which you date the Property Bubble Advent when you invoke “late 1980s”? I find it all hard to disentangle: general credit laxness, national property bubble, local property bubble, and the normal gains property deserves.

Good question; I haven’t fielded it already (at least not specifically); and I agree with your general idea that it is all very hard to disentangle – probably impossible. That’s the main reason I sort of give a range, “late 80s”. Arguably, the structural misallocations really got started back in the 1930s, were kickstarted after the war, and were tubocharged with the unmooring of the dollar completely in the early 1970s.

But here are the factors why I think the late 1980s strikes me as a reasonable starting point to talk about the sustained property bubble.

1. Household debt began its sustained trend explosion upwards starting with the early 1980s. See the charts here:

http://www.financialsense.com/Market/shedlock/2009/0122.html

2. Mortgage securitization really began in earnest in the mid-1980s. Sure, it was around as early as the late 1970s, but guys like Ranieri really got going by the mid-1980s.

3. Housing received its “special subsidy” in the 1986 revisions to the income tax code, when the mortgage interest deduction (which had existed previously) remained while interest on most other forms of personal debt became nondeductible (e.g., auto and credit cards). This favored housing debt over other forms of debt, and helped fuel the view that houses were a store of real value and even “ATMs” (in the final stage of the blowoff bubble top).

4. In California (particularly in resource constrained places like SF), the effects of prop 13 began to become manifest. As property prices rose, partially due to general inflation and the trend lowering of interest rates from 1982-83 onwards, the recipients of the “gift” of prop 13 (legacy owners) apparently became more aware of the subsidy they were extracting from new entrants, and decided to preserve that for their kids. Prop 58, which allowed the grandfathering if the old tax bases by children and grandchildren, was passed in Novermber 1986.

5. The late 1980s (which I remember well) seems to me to be the time when asset price inflation (in real terms) began to be accepted as the normal course of things. This was seen in the stock market, which had fairly recently shaken off the miserable period 1966-1982. This acceptance resulted IMO from the trend disinflation and lowering of real interest rates following the 1980-83 period. (Note that even in the stock market “crash” year of 1987, stocks were UP on the year, for instance.)

Like I said, it’s not scientific, and I could just as easily be convinced that the bubble in real estate assetnominal prices dates from the late 1960s, as the dollar began to wobble and become unmoored, but I think the experience that began in the 1980s – that of falling price inflation (disinflation) combined with falling nominal (and later real) interest rates – led to large nominal and real price gains for leveraged assets. I am also very confident that we are entering a very different environment now (likely rising real rates and rising – or at least not falling – price inflation) and that is why I think price returns from real estate and other leveraged assets are likely to be miserable for years.

Saylor, umm, it was Shiller.

http://www.ritholtz.com/blog/2008/12/classic-case-shiller-hosuing-price-chart-updated/

Ex-SFer, LMRIM,

The mortgage interest deduction has been around as long as there has been a US income tax. Initially all interest was deductible. But in 1986, because of the rising tide of debt and the increasing loss of revenue represented by the deduction, the code was changed so that basically only business interest and mortgage interest were deductible. It has now become something of a sacred cow. Rather than making housing more affordable, economists estimate that it contributes about 10% to home prices. It’s probably time to get rid of it.

NoeValleyJim: although the census ACS number underestimate SF population, the DOF numbers you quote overstate it. It’s complicated (involving around the year 2000 the number of units in the development pipeline, units yet to be demolished as well as the historically low vacancy rates i.e. peak of the dot-com mania) but in a nutshell, the DOF overstates our populaion by 20k+.

Believe me, the City would LOVE to use a pop of 824k, (they would get more $$$), but the revised total as I said above is about 800k, still a population increase.

Agred, Salarywoman. But it wasn’t just because of revenue issues. In 1986, marginal rates were lowered dramatically, and in connection with this, many of the deductions that were used in the inflationary 1970s and early 1980s (including many of the real estate structures we now refer to as “passive loss” structures) were removed. It was touted as part of “simplification”, and I think it really was. However, the gangsters and banksters that run the US housing system managed to secure their pound of flesh by retaining the deduction for housing debt.

I agree it’s time for it to go, but it is a sacred cow, and will not go before the deduction for employer-provided health care does! (In other words, not before complete collapse or nationalization of the entire economy.) IMO those two tax distortions – housing and employer-provided health care (as opposed to privately purchased health care, which is not deductible) have done more to destroy the economic prospects of the US than any other policy (save fiat money, of course 🙂 ).

Thanks debtpocalypse, but i found the one i was refering to:

http://www.cepr.net/documents/publications/100city_2008_05.pdf

it’s been linked to several times on this blog, but in case you missed it. Page 3.

NVJ:

I like to use numbers that are calculated CONSISTENTLY. That’s why I used the 2000 vs 2007 numbers.

It would seem likely that SF was undercounted in similar ways in both of those years.

accuracy isn’t always as important as consistency in derivation of data.

regardless:

even if you say that SF has gained a 10-40k people

and incomes went up 18-27% over those years.

SF housing skyrocketed during that time though

anybody know the median home price in SF in 2000 vs 2007? it’s way way way more than 18-27% higher.

I think it’s more like 100% more higher.

does increasing incomes 18-27% and (arguably) adding a few thousand people justify doubling of RE?

seems unlikely.

NVJ:

there may be a miscommunication:

I have been trying to say that I feel it’s not unreasonable for future RE prices in SF to fall to 2000 levels in INFLATION ADJUSTED terms (not necessarily nominal)

I don’t personally foresee going to 2000 nominal prices, but wouldn’t bet against it either.

sorry for the confusion.

…the structural misallocations really got started back in the 1930s

…the distortive policies of the USG … have now come back to bite us

…from 1895-1995 house prices increased at the level of inflation … What else would the cost of housing be tied to?

It occurs to me that housing costs must indeed rise on average in lockstep with inflation. But that doesn’t mean that it’s a null game from any individual’s perspective.

The only way the housing market should move independently of inflation is if there’s a reservoir of wealth somewhere (serfs?) being tapped, or if there’s some structural reason to favor one asset class over another. The thing is, I doubt that a reservoir of fools or a structural misallocation can last forever.

For the past couple of decades, it seems that people willing to take on ridiculous leverage were the ones who got rewarded. And I agree with LMRiM that government-based distortions of the market have been significant.

Anyone care to opine on who will be the winners and losers in the coming years?

Example: will Prop 13 disappear, after it helped drive the market upward, but right before a new buyer like me could take advantage of it?

I actually think that over the long term, home prices should rise with income, not inflation. This is only about a percent or two a year difference, but it adds up over time. This is assuming that people tend to spend the same proportion of income on housing over time, which they seem to do.

The Case Shiller long-term study indicate that home prices tended to outpace inflation by about a percent a year and this was for the whole country.

ex SF-er, I don’t think SF home prices have doubled since 2000. The Case Shiller index has the top tier at about 160 and this is indexed so that 100 is the value in 2000. So that would be up 60%. We have used the top tier of the MSA from the C/S index before as a proxy for SF home prices and it has worked reasonably well.

I dug up some old DQ News articles that indicate about a 60% run up as well:

http://archive.dqnews.com/AA2000BAY08.shtm

Note SF median home price was 470 in Jul 2000 and it is 744k today. Though they were 400k in Jan 2000, so that is more like 86%. 2000 was a really insane year.

But yes, the run up has been more than warranted by the increase in income and population, just not as vast a discrepancy as is often stated here.

ex-SFer:

According to this site. SFHs ran up ~70% from 2000 to 2007 ($530k to $900k) and condos ran up ~50% ($530k to $800k).

But again, 2000 itself was already the peak of a long run-up of highly dubious sustainability. Median HH income in SF was $55,000. No way can you support a median house/condo price that is 9.6x median income, let alone one that is 13x median income (if you think that incomes grew ~25% during that period).

And yes, I am aware of the “but SF has a lot of renters that bring down the median income” argument. No, it cannot justify a price-to-income ratio anywhere this level. SF’s share of residents that are renters is not spectacularly higher than many other non-special cities.

For example, percent of residents that are renters (from city-data.com):

SF, CA: 65%

Newark, NJ: 76%

St Louis, MO: 53%

Cincinnati, OH: 61%

Atlanta, GA: 56%

Argh, posted and it timed out.

ex-SF-er: median family income for 2000 was 63,545 (2000 Census)

2007 ACS estimates are $81,136 (nowhere near as reliable due to the tiny sample size but I’ll go with around 80k).

-cheers, Jake

I actually think that over the long term, home prices should rise with income, not inflation. … assuming that people tend to spend the same proportion of income on housing over time…

Is that really true? Anyway, my question still stands: there are always winners and losers when the ground moves under our feet. Who will be whom going forward?

@NVJ:

I think that is a reasonable assumption for areas that are supply-constrained (goegraphic limits, like Manhattan, SF), or very dense areas where proximity to a source of income (Wall Street, Sand Hill Road) is important.

so it is as I have maintained for some time now.

SF RE was substantially higher in 2007 than one would have calculated if one used 2000 prices as a baseline of “normal” and then added in population growth and income growth from 2000 to 2007.

this is of course dubious to do, as 2000 was a bubble year in and of itself.

Thus, I still struggle to find an acceptable argument as to why SF couldn’t fall to 2000 levels (inflation adjusted).

“San Francisco has attained the highest population on record with a population of 824,525 on January 1, 2008. This continues the significant upward trend in growth that began in 2006. The city grew by 1.5 percent this year.”

NVJ & others, please take a little closer look at the breakdowns of what populations are actually increasing and moving to the city. I will try to post links on this when I get to the airport, but the population gain is not only from single 20 something University grads making 150K a year looking to buy Dwell style condos. Some want us to believe that the city is becoming one big affluent urban playground, and this may be true in some changing neighborhoods, e.g. especially Noe, but NOT for the entire city as a whole, especially the western districts. I don’t think a 1.5% population gain justifies the price increases we have seen in the city.

I will try to find the SFGate article that talks about the surprising influx of unskilled poor who still flock to the city, and have been living in extreme substandard housing, crowded far beyond what should be allowed. With the Mission becoming even more trendy, I see more and more urban poor moving to the far western districts of the city, as was pointed out in the article, that claimed that the majority of new residents in the city were unskilled poor.

Justin, to your point, and to all of these points, I would venture that there are a great deal more unskilled immigrant poor laborers living in very crowded areas than eveb the 824K speaks to. Ten people in a crowded Mission house or Richmond flat … is that really factored in? I doubt it. Illegal immigrants are likely vary wary of census. Plus, you’re only talking about one year. I think NVJim’s broader point is that the city is actually much, much more populus than is ever disclosed.

Justin & anon – The number of people in the 20 to 35 age bracket decreased about 30% from 2001 to 2003 – let’s call it the Connecticut Diaspora. Not sure if we saw an influx that demographic after 2003, but suffice to say that there are rapid fluctuations of that group into and out of San Francisco over time.

debtpocalypse at 11:49am yesterday – I am a fellow “bitter renter” who will likely catch a knife in the next few months. Your analysis, and NoeValleyJim’s, make me want to wait, but the tax implications for me make it a smart thing to do. So debtpocalypse, what about the interest tax deduction? Aren’t we bitter renters “throwing money out the window,” as my landowning friends used to tell me?

The number of people in the 20 to 35 age bracket decreased about 30% from 2001 to 2003 – let’s call it the Connecticut Diaspora

“Connecticut Diaspora” — love it. They sure did. But they started coming back in droves back in 2004 and have continued to do so. If the layoffs reach critical mass they’ll leave again. But right now? This city is probably more full of people than any time in the recent past.

I think NVJim’s broader point is that the city is actually much, much more populus than is ever disclosed

But the method of tracking WAS consistent, and thus may still be valid. Unless you think there was a marked change in the PERCENTAGE of “uncounted” people.

I think of it like housing “affordability”. For many years it was calculated a certain way by the NAR. it didn’t matter if it was exactly right or not, so long as the method was consistent. You could follow a trend.

Thus, I used 2000 to 2007 as the METHOD was similar. Now in late 2007 they changed the method, so using 2000 with 2009 is useless. (2000 uses the “old” method that under reported population, 20009 uses the “new” method…)

You also do not live here, so the anecdotal feel of the city will be lost on you.

Re: methodology, yes, I would guess that people both counted and uncounted people HAVE increased. I would also guess that they will be leaving if the economy continues to slide.

Have we transitioned from “the French will save SFRE” to “the Chinese will save SFRE” to “unskilled immigrant labor will save SFRE?”

I have lived here since 1991, fluj (and was here a lot before then). And my anecdotal feel of the city is that we are not nearly as crowded as 1998-2000. Those dot-com bubble years were truly amazing. Parking was impossible to find, every rental open house was flocked with dozens of prospective tenants, and you had to expect multiple offers and a quick sale on any entry level home (2-br or less) that came on the market. Ex SF-er’s point is valid — any effect from “undercounting” has not changed. The feel now is much more reminiscent of 1993 than 2003.

Have we transitioned from “the French will save SFRE” to “the Chinese will save SFRE” to “unskilled immigrant labor will save SFRE?”

Who said anything about “saving” anything? The south of the border unskilled labor will definitely leave if the economy continues to slide. Kinda like we, um, said.

But a two part question for you, Foolio. Have you transitioned from cynical to snide to sarcastic and back? and who the hell can tell the difference?

Feels like mid-01 to me.

That mean it’s time to BUY!!

“Aren’t we bitter renters “throwing money out the window,” as my landowning friends used to tell me?”

Your land owning friends are losing 2% per MONTH. On even a modest $600K condo, they are losing $12,000 per month. Rent on such a condo would not even approach $12,000 per month.

I wouldn’t buy in to that arrangement. And the losses are NOT tax deductible.

Yeah, well, anecdotally the south side of the city feels way more crowded than it did in 2000-2001. The city not only undisputably gentrified south since that point in time. Eighteenth street, 24th street, Valencia street, outer Church, Glen Park and Cortland commerce corridors are case studies for that, but the south side is probably where most of the illegals live. Think what you want. I’m not even talking about real estate here, foolio, you sarcastic BART policeman. Think before you shoot, brah. None of these folks are buying anything! It just feels more crowded.

Yes, those areas have seen improvements, but the biggest wave of gentrification was from 1995-2000 there. Note that areas on the south side (Dists. 3 and 10) are where prices have been hammered the most.

“Note that areas on the south side (Dists. 3 and 10) are where prices have been hammered the most.”

LOL.

Oh, I have. I’m fairly sure you have argued this effect upon mix with me too. Funny how that works.

Hammered in price, but not volume. D10 is up YoY. That’s very likely evidence of further southern gentrification in action. These are 20 % down days, mind you. Watch Geneva, Ocean, and Excelsior start getting wine bars in 10 years.

Nice attempt at a seque there, fluj! I’ve never argued that mix does not affect medians. But c’mon, don’t throw away your credibility. Here are some sales stats (free free to offer others if you have them):

http://blackstone-sanfrancisco.com/198.html

So D10 saw 484 SFR sales in 2008 and 461 in 2007. That is up! But it saw 566 in 2006 and between 600 and 800 a year each of the prior 10 years (only 589 in 2001). 2008 was a terrible year for D10 sales! Same story in D3 in the south. And even you concede this gentrifying south side district (D10) has been hammered on prices — of course, low sales volume and declining prices typically are correlated. I just don’t see any evidence backing up your hypothesis of a south side reinvention other than your personal “feel” for things.

I’m not boasting about how good it is or isn’t. And I didn’t say anything about 2006, either. That year was a highwater mark for both volume and probably price in the southernmost areas, sure.

But so what? That’s not what I ever talked about. Two thousand six has no place in a YoY decline chart, considering that only in September of 2008 did the shift really begin in earnest. Most of these charts and statistics are concerned with showing YoY, and by month at that. Who’s being dishonest? Clearly it is you, trotting out 2006 and trying to make it seem like I’m trumpeting record sales or some other nonsense.

It’s especially glaring if you look at individual months, YoY. The fact is (sales volume up) + (sales price WAY down, ~150K or so) is huge in YoY terms. Don’t really care if you aint feelin my feel, either.

Fluj, I gotta say, you’re rambling here. I really do appreciate your insight into things and you plainly have a much greater involvement in the trenches than I do (I’m just looking down from my 28th floor office, and all I can see from here are a few slices of Ds 7 and 8). But you can’t just make stuff up.

Trip, to simplify, because I think you missed my point.

2005-2006 D3 and D10 — Higher volume, higher price. No money down on a subprime financed 650K house

2008 — 20 percent down on a conforming loan 450-500K house. Greatly lower price. But higher volume than 2007 (2007 was a transitional year for the areas, seemingly)

Which buyer demographic is actually more well-heeled?

Is this a gentrifying? I said it’s “very likely evidence of further gentrification.” It’s just a theory.

But 2008 over 2007 is pretty remarkable in those areas, AND these folks are buying with cash money down payments.

Now that is a theory with some evidence that makes some sense! Still a little early to tell if this is gentrification or slumlords jumping into the market, or a little of both.

A tangent — if my number-crunching is right, the SF MSA just passed San Diego for the greatest drop from peak prices. We’re Number One!

2005-2006 D3 and D10 — Higher volume, higher price. No money down on a subprime financed 650K house

2008 — 20 percent down on a conforming loan 450-500K house. Greatly lower price.

Let’s put some meat on this hypothetical, from an actual D3 house in Oceanview, not too far from Ocean (where all the wine bars oare going to be in 10 years) and not too far from where people were telling me a few months ago 2/1 houses cost $2800/mo to rent (lol).

262 Minerva. Purchased for $630K in 2006 (so, pretty close to fluj’s $650K hypothetical). Now listed for $369K. Down 41.42%. And it’s still not sold.

http://www.redfin.com/CA/San-Francisco/262-Minerva-St-94112/home/1465061

Which buyer is better heeled? Tough to say. The future buyer will likely be someone who is lent the 3% by some scam nonprofit to make the FHA requirement. The 2006 purchaser probably put $0 down. It’s probably a wash.

It’s funny to watch how people resist the obvious, and try to concoct all sorts of stories as to why prices got as high as they did (“gentrification” spreading south, lol). It was a bubble. People fall for bubbles. In SF, it seems that people are particularly susceptible to “groupthink” (look at election results, or the number of Toyota Piouses on the road).

As for the jabs I always get when I offer an estimate of intrinsic or fair value (“Oh, you went to appraisal school over the weekend?”), just think of the incompetent who signed his name to a $630K valuation for that POS, 262 Minerva. Intrinsic value of 262 Minerva: around $200K, perhaps $30-50K higher if the interior is in better shape than I imagine.

There are whole neighborhoods full of people now that didn’t even exist in 2000. And SOMA is much, much denser. All the high rise condos and even most of the mid-rise stuff was built in the last eight years. There has been some infill development in most other neighborhoods as well.

It’s funny to watch how people resist the obvious, and try to concoct all sorts of stories as to why prices got as high as they did (“gentrification” spreading south, lol).

No, not what I said in that regard. I pointed to specific commercial areas in undeniably more gentrified southward neighborhoods as evidence of that. The more marginal southernmost neighborhoods are another phenomenon IMO. That is all very clearly said above. The “wine bar” thing was a joke.

Not going to get into your “fair value” stuff. It means nothing to me, except it always makes me wonder why you care.

LMRiM,

Thanks for your thoughts. I’d read that article you linked to via Mish about private v. public debt growth in the past few decades. My only issue with their data presentation is that I see no breakdown between the private debt floated by corporations and the private debt floated by households. It’s an important distinction in my mind, since one can’t assume that all that growth is household debt. I would love to see the same data broken out for households – I think it would tell us a lot about when to reasonably date things.

I’m still going to have to mull over when and how to benchmark value and grow it appropriately for one’s own purpose. I think I’d post-date the death of Bretton Woods. In thinking about it now, I think I’d move an earliest “value” benchmark to Volker’s 1982 high-rate policy to smash inflation. That action effectively reset the levered-asset pendulum, and those assets enjoyed a generation of appreciation supported by declining inflation expectations and concurrent accommodative interest rate policy. That interest rate dynamic came to be misunderstood as “only goes up.”

Admittedly, at some point, inflation expectations simply shifted from a CPI basket to readily levered assets (in my mind, first equities; later real estate). These assets were not understood to be suffering from (Austrian…) inflation, but rather, benevolent “bull markets.”

While I’d date the residential real estate bubble no earlier than 1982, I’d move it further up for the purpose of pricing a cautious purchase today. The credit madness was finally a Boomer thing – WWII era Americans remember the Great Depression. The Wall Street collapse of ’29 caused localized and limited direct financial duress – it was the indirect fallout from it that hit average Americans, especially in the form of losing one’s home. That experience burns a generational memory – I know my Depression-era parents still tell me about never having expectations of owning a home.

In 1982 the oldest Boomers (i.e., born ’45 – ’60, to pull generational demarcations from a hat) were mid-30s, and probably already well-established in the homeownership thing. But the youngest among them were still only finishing college, and had their starter-home and move-up cycles still ahead.

All these are general observations: California-specific and Bay Area-specific and San Francisco-specific trends complicate the thing. At the very least, a “bottom” cannot be put in place until prices stop falling – I think those who here who wish to keep insisting that the bottom is either “in” or “near” need to acknowledge that simple fact.

Two things we agree on. First: “I think price returns from real estate and other leveraged assets are likely to be miserable for years.” Absolutely. I’d only specify, “U.S. dollar-denominated real estate and other leveraged assets.”

Second (and related), you’ve mentioned spending 2008 adding to positions in Asia. Yeah – same here.

1stTimeBuyer,

We have a shared predicament. I’ve got a 2-year old, and a second in the oven, and a patient wife of 10-years who wants to own a home. She’s smart – Ph.D. in economics – and is firmly in my camp on further price declines. Since we’re looking at likely a $1m purchase, and we’re easily off 10% from the top in the East Bay BAP ‘hoods of interest to us, we figure our patience has put Boy #1 through college. I would estimate that our rent-controlled flat costs less than the taxes/insurance/maintenance on any purchase, so on a “throw it away” basis, I think we stay net positive. At worst, it’s a wash… and the landlord’s headache. And with another 10% down from current levels by summer’s end “easy” in my book (I’m with Tipster on this), I figure a little more patience purchases Boy #2’s college fund.

I further believe that we will remain upsidedown in any non-foreclosure purchase we make in late 2009 for several years. I don’t think the bottom will be in until 2012 – the ARM calendars indicate that there will remain a steady stream of recasts and resets that will result in a steady trickle of distress properties for quite some time.

So, if circumstance dictates that its “homeowner-time” in 2009, you wait as long as possible, bargain as hard as possible, and accept that you’re purchasing a levered asset that will certainly continue to decline in price. Gotta be comfortable with that, in my opinion.

Debtpoclypse,

All the data on aggregate debt in the US traces in one way or another back to the Fed’s Z.1 quarterly. The problem with the presentation is that it is typically in nominal dollars. Here’s a link to the part of the current Z.1 that is most relevant:

http://www.federalreserve.gov/releases/z1/Current/z1r-2.pdf

I found some nice picture graphs here that support a mid- to late-1980s time period as a “hinge point” for trying to grapple with fair value (but I can’t vouch for the whole paper – I haven’t read it):

http://www.bankofengland.co.uk/publications/workingpapers/wp206.pdf

(See Chart 4 on p. 13 especially.)

The basic problem with the composition of aggregate US debt over the past 30 years has been the growth in household and financial sector debt. These are of course flip sides of the same coin: the rentiers (financial companies) and the sharecropper/serfs (US households). This presentation and discussion has many pictorial representations, and gathers the data in one place (but the web page design leaves a LOT to be desired 🙂 ):

http://mwhodges.home.att.net/nat-debt/debt-nat-a.htm

BTW, best of luck with the new addition to your family!

PS – I’ve only just started buying Asian equity indexes, very slowly and deliberately. I intend to get to about a 20% net worth position in Asia by the end of 2010. Our annual living expenses are about 1.5% of net worth (roughly), so it is going to be a pretty big bet when all is said and done.

“mid- to late-1980s time period”

huh, I would have said the kink in M3 in 95 marked the beginning of the significant asset inflation. Ah, well.

LMRiM, I’m looking for a recommendation for a trading platform. Something for someone who is not going to be trading frequently and is mainly concerned with not being sucked dry by fees. Any recommendations?

diemos,

I’m looking for a recommendation for a trading platform.

When I was trading professionally, I had 5 screens in front of me: Bloomberg, charting software/application by a company called Aspen, a dual screen Reuters2000 platform (uh oh, I’m dating myself), and a proprietary trade entry and VaR system. All CRTs. What a mess that was.

Today I look at Yahoo Finance for charts, and I use Fidelity and e-trade for trade execution and custody (Fidelity is the larger account by far). I don’t miss all the old screens for a minute 🙂

For the type of trading I’m guessing you’d want to do, primarily what we used to call “position” trading based on macro ideas and perhaps some basic technical indicators, I’d think any of the well known platforms would be fine. Fidelity has something called Active Trader Pro that they give to people with high balances, but I hardly ever use it. Their commission rates are $8, and execution seems ok. They rip me off for a tick or two always, but they all do – no big deal. I’d think Schwab would be fine too. Otions trades through Fidelity seem to be routed often through Citadel. They rip you off for a pip or two as well, but my options trading has been very profitable the last two years and Ken Griffin can use the money these days 🙂

I’m guessing you don’t want to trade futures? With all the ETFs, and index trackers around, there’s really no need to anymore unless you really crave the leverage 🙂

I hope that helps. Let me know if you have some specific ideas about what you’d want to trade if it is not going to be just securities and maybe some options. I don’t trade CDS, so don’t ask me about that 🙂

Thanks LMRiM,

I’m beginning to wake up and pay attention to the markets now that most of the speculative premium seems to have been wrung out. I’ll probably start accumulating positions in companies toward the end of this year after the next big leg down.

I doubt that I’ll do much with the more complicated instruments. When I put my capital at risk I don’t sleep well at night if I don’t think I understand what I’m doing.

Cheers.