Bay Area Notices of Default (NODs) fell 12% on a year-over-year basis in the fourth quarter of 2008, down 9.6% in San Francisco proper (from 353 to 302). And while the number of new NODs in San Francisco also fell 25% from the third quarter, the lead time changing state law took effect in September is likely to still be skewing the comparisons.

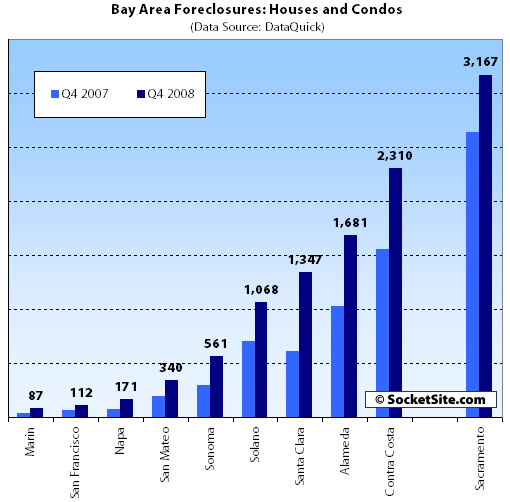

At the same time, actual Bay Area foreclosures rose 68% year-over-year (from 4,573 to 7,677) with Contra Costa (up 48% to 2,310), Alameda (up 64% to 1,681) and Santa Clara (up 120% to 1,347) leading the way with respect to volume.

Fourth quarter recorded foreclosures in San Francisco totaled 112, up 70% on a year-over-year basis but down 42% (80 homes) from the third quarter 2008. Think aforementioned state law (reducing the number of pipeline foreclosures) and last month’s foreclosure moratorium by Fannie Mae and Freddie Mac (which was extended through January 31).

Most of the loans that went into default last quarter were originated between October 2005 and January 2007 [versus October 2005 to February 2007 last quarter]. The median age was 29 months, up from 21 months a year earlier.

We continue to move from those who were simply undercapitalized to begin with to those who had a bigger cushion in the bank.

∙ Temporary Drop in California Foreclosure Activity [DataQuick]

∙ Actual San Francisco Foreclosures Up 36% QOQ (191% YOY) [SocketSite]

to say ‘most of the loans’ and then give the median is really annoying. How did the median go up by 8 months if the ‘most’ range only changed by a single month. A full graph of the distribution would be nice…

Do we have any evidence other than intuition that we are simply seeing foreclosures on people who had more cash cushion? If I knew I was going to inevitably foreclose anyway, I would just get it over with and keep the cash I have left, rather than put it all into the house and lose it all anyway.

I wonder how many of the foreclosures coincided with a job loss or some other event that the owner might hope were temporary. In that case, you might spend all your cash hoping you get a new job before you lose the house.

Umm.. wasn’t there a moratorium on foreclosures/NODs for the last couple months of the year? Of course the numbers went down yoy.

[Editor’s Note: That there was (a Fannie/Freddie foreclosure moratorium starting November 26 and extended through January 31) and since added to the post. Cheers.]

WHAT?!

According to SocketSite posters, things can only get worse not better.

This is shocking.

We continue to move from those who were simply undercapitalized to begin with to those who had a bigger cushion in the bank.

I did not look at the raw data that made up this DQ news release, but I’m not sure I agree with this statement.

There is another reason why origination date range could remain similar but age of defaulted loans could increase…

The loan TYPES may be changing which could explain the fact that the origination dates are similar but the median age was 8 months longer.

Specifically:

last year’s defaults may have been primarily in the subprime ARM space, many of which have a recast date of 2 years.

This year’s defaults may be on ALT-A and Option ARM products, which often have 3,5, or 7 year recasts.

Given the different loan types with different reset/recast dates, it was expected that loan ages of defaulted loans would INCREASE over time.

If memory serves, using the original data from Ivy Zellman’s research from way back in early 2007 we would expect the “honeymoon” period to be right about now when most of the Subprime 2 year recast loans had recasted, but the 3-7 year ALT A and Option ARMs had not yet begun. The lull was anticipated to be Jan 2009 until July 2009.

In fact, I predicted this pattern long ago here on socketsite, but am too lazy to pull up my posts from >1 year ago.

I have not analyzed the raw data to confirm my hypothesis… however, I DID hypothesize that we would at some point see that defaulted loans were “older” and also of a different type of laon, and also that there would be a lull in early 2009.

According to SocketSite posters, things can only get worse not better.

Thanks for adding value.

That said, as some of you may have noticed I have recently been trying to see a silver lining and also post contrarian ideas such as the possibility of a W shaped recession, recent mild thawing in the credit markets, possible inflation in assets including housing in the medium term.

The actions over the last several days has disabused me of this optimism. Unfortunately, our govt still either doesn’t understand the problem, or is too intertwined with connected interests to effectively improve our situation.

based on the Fed Reserve statement today and this nonsense about the “bad bank” any chance of a “W” shaped recession is dwindling rapidly.

The Fed proposing to purchase long dated Treasuries is a sign of desperation. Unfortunately, it looks like our choices will be U or L shaped recession or depression (whatever that is).

Our govt is continuing and even accelerating its failed policies under GWB. It has no possibility of working. It never did.

Given what I stated above, I believe foreclosures will continue unabated UNLESS the govt begins outright purchases of mortgages (highly possible) or has some sort of national foreclosure moratorium (also possible) or passes cram down laws (also possible).

disclosure: I now anticipate a major equities collapse again in the short term (1-2 months) and will (not yet) invest accordingly. thus I am not completely unbiased in what I just wrote, but I will have “skin in the game”.

You’re starting to see the light, ex SF-er 🙂

No equities collapse yet IMO, at least not before we get a retracement rally to the 950-1000 level, but I can’t place too much faith in this conviction. I do think that prospects for the US have darkened considerably. We effectively jumped off the cliff when we passed the first “bailout”. In fact, to stretch the analogy, the bailout and the actions which followed simply built a Rube Goldberg structure on top of the cliff, so the fall is deeper. Politically, now, the die is cast, and they are only going to slow the descent a bit. The end result is the same – the ground.

Whatever.

The world is not coming to an end. If you bought your place and are going to own it forever, you don’t care if you could have bought it 50% cheaper the next day.

Is there a similar concept to “in contract” for foreclosures?

Really, jessep? I think I’d care if I could have cut my payments by 50% and if my down payment totally evaporated.

That’s one of the reasons I’ve yet to pull the trigger. I’d still be stretching (by my standards) to get in a house I like, even if it’s within 3x income, so I don’t want to commit too much of my monthly take home when prices are still coming down.

I also think they’ll try a national foreclosure holiday, in futility. ex SF-er, I’m starting to buy into the ka-poom theory at this point. LMRiM has mentioned he thinks the inflation is still years away, but how far off from the “poom” do you think we are?

“If you bought your place and are going to own it forever, you don’t care if you could have bought it 50% cheaper the next day.”

It sure would have made those monthly payments 50% cheaper.

That’s kinda crap jessop.

another way to look at it is, you could have bought a much,much, much nicer place for the same money the very next day.

LMRiM:

I’ve always seen the light. I was just hoping that the new admin would change direction. Thus I was trying to highlight that there was still a modicum of uncertainty out there. But this last week has proven otherwise. you and I have really only disagreed on like 3 things (the CDS problem, KaPOOM vs continued deflation, and the Treasury bubble) and even then our differences are slight and are more nuances of the same rather than differences. but I strongly believe that there’s no man on Earth who really understands 100% of what’s going on. There just is no precedent for some of this stuff (some of this wasn’t even done in the Great Depression!)

Dude: I hesitate to make a guess on the timeframe of the inflationary POOM, partially because too much is in central control but mainly because I’m a pretty poor timer.

We will have plenty of warning though… in fact, we may even see a head-fake once or twice (like a mini commodity boom) prior to the real POOM. My ROUGHEST of guestimates would be 2 years, give or take 5 years. 🙂

The govt is in full deflation fighting mode now. At this time they are failing as destruction of credit overwealms their efforts, and this is worsened by the slowed velocity of money. But each day IMO we march towards a time where inflation will come.

The Fed announcing it may purchase Treasuries was a big first step. (the Fed will create money to buy debt created by the Treasury… just think on that for a while).

creation of a “bad bank” would be another step.

Govt pseudo-control of banks (forcing them to lend more to less-worthy borrowers) would be a third.

but there are other scenarios as well that could ignite the flames. The above 3 are just the ones being discussed now.

back to foreclosures though: It seems nearly 100% likely that the govt will intervene in that process somehow.

I was just hoping that the new admin would change direction.

We do agree on most things now, ex SF-er. But that’s what I mean about seeing the light: why in the world would you have thought the “new” administration would have done anything differently? The same banksters have been in charge all along. The hucksters on the ticket change in order to dupe the peasants, but the banksters call the shots. They always have (at least in our lifetimes).

About inflation, again, I think we should always stress “price” inflation rather than credit/money supply inflation (as the Austrians do, of course). The implications are important for real estate. Real estate is a leveraged asset, and therefore will be correlated with measures of credit/money supply. Right now, narrow money supply aggregates are exploding higher (especially base money/bank reserves), while broad measures of credit are in full deflationary collapse (if the loans were truly marked to market, which is what counts for decisionmaking by individuals and firms in the end).

I think we could get CPI-type inflation in goods, services, etc. much faster than “years”. Even Japan in the early stages of its collapse had CPI inflation greater than 4% (say, prior to 1992 or so). But to get meaningful “inflation” in credit is a long long ways off, and is contrained by our inability to service existing debt (at 360% debt/gdp, it’s impossible, and the pool of real savings understands this). Under conditions like that, it is impossible to imagine the nominal price of real estate assets even keeping up with nominal price inflation, under any circumstances.

In any case short of hyperinflation, I find it hard to imagine that the nominal price of real estate assets won’t continue to decline for a few years more, at a minimum, although the bulk of the nominal price decline is likely to be done within 2 years or so, I’d bet. In a true hyperinflation, credit will be destroyed even faster than in deflation, and leveraged assets will trade towards their “cash on the barrel” equivalent value.

LMRiM

Can you give an example for the last paragraph. It went right over my pointed head and I’m interested to figure out how the hyper inflation deal works.

why in the world would you have thought the “new” administration would have done anything differently?

Hope. (trademark)

🙂

actually I thought that we had a chance for 2 reasons. Stiglitz (nobel laureat economist who often makes sense) and Volcker advising the new Pres, and the resurgence of economists like Mr. Roubini. I was wary with Geithner/Bair as Obama picks, but still held hope.

I was holding out to see what they might do.

I still do believe Govt can be a powerful force, for both good and mischief.

Today I would be much more optimistic if the new administration had done things like forced all CDS into an open marketplace, figured out which banks could achieve solvency and nationalized/wound down all the rest, stopped interfering with the clearance mechanism in multiple financial markets, etc etc etc.

but it was not to be.

That said, I agree with most everything you say. And of course, when I was talking about inflation above I did mean monetary inflation, not price appreciation in assets. However, the price appreciation in assets will be a “tell” that inflation may be starting.

I only have a slight disagreement with you. we are able to inflate out of a deflationary environment when we are the reserve currency and debt is denominated in our currency. I know you’ve read Ben’s papers. Many don’t think it can be done. I’m not so sure that it can’t. Perhaps it’s you who is the optimist? 🙂

my problem: trying to convince people who can’t be convinced.

Go back to your mass hysteria please. I tried the best I could.

I can’t correct or mitigate the cynicism and snarkiness on this blog.

No, jessap, your problem is your arguments make no rational sense.

Try this one:

“If you bought your place and are going to own it forever, you as a Realtor, I don’t care if you could have bought it 50% cheaper the next day.”

Then it would be believable and make sense.

I am not a realtor.

But there is no way of predicting markets in the short-term.

We are certainly in a negative feedback cycle but that when that will end is not clear.

Ok fine, my situation may be atypical: But if my property went down 50%, I couldn’t care less.

I love where I live and I don’t intend to move. I paid cash and couldn’t be happier.

Sounds good, jessep. Too bad buyers like you make up about .001% of the homebuyers in the United States. If falling prices weren’t a big deal, and most people paid cash, why are the incompetent policymakers falling all over themselves making an utter mess of everything?

Remember how people thought the Fed was going to avert a recession back in Fall 07 when they cut rates?

It’s a big deal, and these guys don’t have a clue. It would be great if the average buyer could pay cash – or at least could afford to put down 50% on an average house – but the banksters and the Fed made sure that wouldn’t be possible over the last 70 years of rigged credit markets.

Time to pay the piper!

@ Sunny Jim – I’ll post something later trying to clarify my ranting about hyperinflation versus nominal price increases.

..and now imagine if you only had to pay half that cash for the same house. You’d be even happier.

Um…actually tipster. I couldn’t have.

My whole building is sold out, and everyone on my floor paid cash.

I was in a multiple bid situation.

jessep, you wouldn’t care that you could have half the cash you paid for the property left in the bank? you wouldn’t care that you could have bought a much better place for the same price? Really?

If that’s true for you, fine, but it’s astonishing that you’d think more than a handful of people share those sentiments.

I obviously would have LIKED to have paid half, but with certain properties it isn’t clear that you could.

All you can guess-timate in my view is whether you are paying a fair price.

I don’t know why everyone is giving jesse so much grief. Many people I know love paying more than they have to for SFRE.

Their RE agents love it too.

“I don’t know why everyone is giving jesse so much grief. Many people I know love paying more than they have to for SFRE.”

Fair enough, I should stop reading this blog.

Ciao! =)

“My whole building is sold out, and everyone on my floor paid cash.”

jessep – I hate call anyone on this, but it almost seems as if you are making this stuff up as you go to support your argument. About the only way that I can believe the above statement is if your building has one unit per floor and you were the sole all cash buyer.

Please tell us that jessep != troll.

jessep, I’m in the same boat as you, except I did not buy cash. Whether I’m happy or sad about my decision really does not matter, I can’t go back or forward in time and pay less; paid what I paid when I paid it for something I wanted and am very happy with. I have confidence in America that this is a part of the ever present sine curve of which we just happen to be on the down side.

I also find funny that many posters believe the gov’t is the only one pulling the strings here. People will ultimately come out of thier shells and start consumption again once confidence in the markets take hold. Commerce will not come to a halt.

We are at an unprecedented economic time and while there are many intellectual opinions,which are great and insightful, they are limited. We forget that we have leading, current and lagging indicators in order to give inferences of the overall economy, nothing is absolute, and no one size fits all. Just like the universe, still too much that is unknown and beyond the scope of understanding for any single mind or brain.

Despair,

Could you please ask me these things before making wild accusations?

My building has 13 units. My floor had four units.

Do I sound like a troll?

Do I sound like a troll?

in general, no. but when you state that everybody on your floor paid cash, somewhat. I just assumed your not-caring-about-losing-50% comment was hyperbole and not meant to be taken seriously.

This is not to say that you are a liar (about the all-cash situation). just that it is extremely uncommon for people to pay all cash for a house/condo, even if they have the means to do so.

I also love my house, and will keep it even though I foresee a 30-40% drop in value. I also can pay my entire mortgage in cash right this second, leaving enough cash to live for 10 years or more without working one second. I have many friends/associates who are in the top 1% of income due to where I trained (breeding ground for the future affluent of America) and my profession.

However, I don’t think I know anybody who paid all cash for a home. That includes my hedge fund and VC friends, my Googleaire family members, my super-specialist doctor colleagues, my friends who own some of the largest private corporations in America, (you would know their last name) etc.

are you over 60-70 years of age (serious question)? because I do think paying all cash is more common in the “greatest generation”, but those times are decades past.

also: how would you know if the people in your building paid all cash? is it a co-op in Manhattan or a variant of a TIC in SF?

But there is no way of predicting markets in the short-term.

this is not necessarily true, unless by “short term” you mean minute to minute or day to day. but one can certainly predict markets in the near term without difficulty. Many of us have consistently done it right here

We are certainly in a negative feedback cycle but that when that will end is not clear.

I agree completely.

ex-SFer:

To answer your questions:

When the pond starts rising due to a downpour, you start going up in the world. That doesn’t mean you’re right. It could mean luck, it could mean you, etc.

My family has a long history of paying cash for everything. My parents did, I did, etc. I know nothing about you, your friends & their careers, or your situation

I am not over 60 years old and I am not a liar.

Just because current events alight with your predictions does not mean you are good at predicting.

“If you bought your place and are going to own it forever, you don’t care if you could have bought it 50% cheaper the next day.”

http://grammar.about.com/od/60essays/a/whistlessay.htm

“We are certainly in a negative feedback cycle but that when that will end is not clear.”

Aaaiiieeeeaaaa!

Negative feedback is the good kind. When the system moves away from equilibrium the feedback pushes it back toward the equilibrium points. This creates a stable system.

Positive (self-reinforcing) feedback is the bad kind. When the system moves away from equilibrium the feedback pushes it away from the equilibrium point. This creates an unstable and oscillatory system.

I agree diemos.

But so what?

That doesn’t bother me.

I want prices to go down not up. I don’t want to sell, I’m going to be buying more.

It seems like some (LMRIM and xsfer) agree on what you think shouldn’t be done – major fiscal and or monetary govt interference with natural mkt forces at work.

I think as time goes on some of your predictions may come to pass, such as direct govt purchase of mortgages and at least one foreclosure moratorium to ease some of the pain.

I even think the CDS issue will be washed out in the public laundry when the politicians get around to understanding it, its very size, and its implications.

But other than letting the bubble wind down with unmitigaged consequences, what more would you suggest for the govt to do.

The only entity that is too big to fail is the USG (and by extension the USD). Now that the two year long distraction of political campaigning is behind us, someday the pols will hopefullly realize this, come out of the grip of the so-called banksters, and some of the big, most toxic financial entities will be gone.

Just because current events alight with your predictions does not mean you are good at predicting.

True. for instance, if you take 1,000,000 people and have them flip coins, some of them will flip 100 consecutive heads purely by chance. it doesn’t mean they’re a good coin flipper even though it might look like that to spectators.

Perhaps all of my past predictions have been by chance. That said, some of them seem so obvious… such as “SF Real Estate will be negatively affected by recession.”.

It seems obvious to everybody now (and was to me years ago), but we had arguments about this very prediction on Socketsite just a few years ago.

There are other simple predictions as well. Things like “Real Estate cannot gain 10-20% per year forever”. but many people believed it could at one time.

Other predictions were obvious to anybody who understands finance. Such as “credit crises last a long time and do not resolve quickly”.

but I agree with you: it is possible that I am no different than a Hedge Fund Guru 2 years ago who did well solely because every market simply went up. (but in reverse)

also: it IS hard, if not impossible, to predict things like “what will the price of soybeans be in 1 week” or “what will be the bottom of RE”.

===

My family has a long history of paying cash for everything

I don’t doubt it.

what people find incredulous is that 4 out of 4 people on your floor also paid full cash for their units, and that you would know about it. (that’s why I asked if you’re in a NYC Coop as example, because then you WOULD know it… that may also be the case for a TIC… or perhaps you’re handy with the inter-toobz).

Note: my intention was never to call you a liar. It was only to explain to you why some people claim you are a troll. Paying all-cash for Real Estate in the last decade has become far more than passee… it has been considered foolish as you are “locking up” your money.

No reason to get upset when I give you the answer to your question (“Do I sound like a troll?”)

regardless, it’s an unresolvable question anyway because the only way for you to prove your claim (of everybody paying cash) would be to “out” yourself, and anonymity has its plusses on a blog.

you can read my predictions on the SS archives and see where I’ve been correct and where I’ve been wrong. (of course I’ve been wrong at times, nobody is 100%)

But other than letting the bubble wind down with unmitigaged consequences, what more would you suggest for the govt to do.

Amir, I wrote a long and eloquent post (or so I thought) but SS ate it. i’ll be more brief.

First, I don’t believe that there is “an” answer, and if there were “an” answer, I don’t believe that humans have the capability of understanding it. The problems in our economic system are severe and structural, and even the creators of the problem (derivatives) don’t fully understand how they work. Which is why we are where we are.

I’ve used the example of metastatic lung cancer before. Once you have metastatic lung cancer there is no cure. the cure was to never have smoked. we have palliative medicines, but in the end there’s nothing we can do. we aren’t smart enough (at least not yet).

our current problems are the financial version of metastatic lung cancer. The answer was to never allow us to get here in the first place.

LMRiM and I disagree on what “should” be done, as do nobel laureates and presidents and fed chairmen, precisely because it is so complex. (LMRiM typically espouses more of a “free market liquidation” answer than I do)

that said: it is my thought that the essential problem today is a lack of transparency in the markets which causes mistrust. counterparties cannot trust one another. This causes the govt to come in and try to fix things. Unfortuntely, to date their answer has been to try to cause LESS transparency. FOr instance, buy up assets at inflated prices, therefore nobody knows how much the assets are really worth. Or doing behind doors deals with major banks, so that nobody knows how insolvent they really are. what is going on with Citi? AIG? BofA? Wells Fargo? Nobody knows. And we never will, because the Fed/govt are propping them up and keeping us from knowing.

thus, what must be done is increase transparency. Here are ways one could do that. Note: it would very possibly/probably cause instant depression, which is why they do not wish to do this.

1) force all OTC derivatives including all CDS contracts into the open market, possibly through a clearing mechanism such as what happens on the ICE or CME. Many of the contracts will need to be re-written so that they are standardized so that they can “fit” into the clearing house

2) not to be too esoteric, but technically the cleraing house is the counterparty to all trades. It is unlikely that any current exchange could take on this role given the size of the OTC derivatives market. Thus it would likely need govt support

3) the govt/Fed/regulators need to send forensic accountants into every major national and regional bank and figure out which ones are insolvent, which are solvent but illiquid, and which are saveable

4) once it knows which are insolvent and unsaveable, they must let them fail

5) this will trigger a massive credit event. thus the need for the above clearing mechansim given the high risk for cascading cross defaults. Much taxpayer money will be spent supporting the clearing house, but I see no other way. (of note, these cascading cross defaults will likely cause instant depression, which is why nobody wants to do this)

6) the govt will then support those banks that remain, OR will nationalize the healthiest of the insolvent if none remain (the so-called Swedish Model), OR create a new national bank. this is important as we will need banking services if we are to have a functional economy. We just don’t necessarily need to have the CURRENT companies as our banks

7) the other phase of this is in the hands of Obama/congress. They will need to have a big stimulus, but not what is passed. The stimulus should be for things like tax breaks, unemployment benefits, basic healthcare benefits, welfare, etc to act as a safety net for our populace (like I said, we’ll be in depression). also help for states and municipalities and pension funds etc, all of which will take major hits through this.

EXTREMELY painful. I’m not sure that it’s doable. But it’s the only thing I see that could actually work. there are other ideas too… that’s the one that is in my mind foremost right now.

That said: our govt will never do this. instead, looks like they’re going to keep trying to pour more and more money into insolvent institutions in a futile effort (Citi, BofA, AIG, etc)

Jessop,

“I want prices to go down not up. I don’t want to sell, I’m going to be buying more”

but surely then you would be upset if you bought and it fell 50% the next day. That would have been one more house you could have bought if you had waited one more day.

ex SF-er,

I appreciate your response. As you imply, I don’t think there is or will ever be the political will required for your solution, given the consequences; not to mention the massive legal and logistic implications of rewriting these contracts.

Just as I suppose how difficult it is, to follow your analogy, for a cancer patient to come to terms with the fact that their cancer has spread, that there may not be a cure, and realize their mortality.

That said, to take your idea and suppose transparency of these assest and their market was maximized, two things come to mind.

By what pricing mechanism could they be possibly sold. And, more importantly, would there even be a market for them where they could be priced. In the midst of spiraling deflation, who would put their capital at risk for these illiquid, toxic assets.

It seems the only reason a lot of these insolvent banks are even still viable is b/c of the lack of transparency.

Even with a potential govt back stop, I just don’t think the legal hurdles could be overcome for a lot of these institution to expose themselves.

There’s also been recent discussion of creating a governmental ‘bad bank’ for these – in my assumption – worthless assests. Bad bank seems to be just inverse jargon for going bank rupt, on the taxpayer’s dime. LRMIM, is there a way to go short the American taxpayer?

Has anyone pointed out that San Francisco’s foreclosure numbers are way way lower than in the parts of CA where we are seeing huge declines?

Not sure how much bigger Sacramento County is versus ours, but those numbers are massive.

I’ve said it many, many times. The bubble largely applied to areas in the Inland Empire where land had essentially *no* value. Those are the ones losing 50% of their home prices. Prices also went up too much in areas where the land had *decent* value, such as Soma, Civic Center (in SF) or Redwood City. They are losing more like 25% of their value now. And the bubble appplied slightly to areas where land had *considerable* value, like Pac Heights or Menlo Park, where prices are going to be down about 10%.

Those who don’t believe me should sit tight, and buy their $400/sqft SFH in Russian Hill by mid-2010. Enjoy renting until then 😉

jessep,

A few conclusions that i got about SS to share with you:

1. there are a dozen (or so) posters here who seem to be older (55 and up), who had a lot of expenience with RE (watching on the sideline that is), who had a lot experience with life in general, and most importantly, who think that their experience is THE EXPERIENC.

You don’t want to get into a debute with them. Period.

2. Come to SS for entertaiment. From time to time, there are good posts that give me a good laugh.

3. if you are like me, looking for the next opportunity to buy, come to SS for info on price cuts since it will never miss feathuring these properties. Good info for me, at least.

4. So far, these price cuts are either with locations that I am less interested in (like SOMA and Noe), or with properties that are way above my budget. For a property that was asking 17M, it can come down 80% and I still can’t afford it.

5. Only thing that i agree, whole heartly, with the bears is that SF is overpriced, way overpriced.

SNB,

1. We will.

2. Land in various places doesn’t have zero value except to SF snobs like yourself. Lots of people lead very happy lives in the East Bay.

3. Land thought valuable can turn nearly worthless quickly. Two words: De troit.

4. People can’t agree on what should be done because people know that some segment of the population will need to be tossed overboard to save the sinking ship. They can’t agree mostly on who should be tossed overboard.

5. The stimulus program put forward will help somewhat, but it isn’t designed to fix anything, it’s mostly designed to put back in place the welfare system the republicans spent 12 years dismantling. Less than 15% goes towards infrastructure. The rest really is just welfare, either to individuals or to favored industries. That tells me the powers that be have given up on saving anything and are rushing to put the welfare system back in place to address what’s coming. They aren’t going to try to stop the locusts, they’ll just build up a store of supplies to tide things over when it happens.

6. Most telling: who laid off yesterday? Caterpiller. Caterpiller, the recipient of all that stimulus spending? Why did they lay off 20,000 people in the face of massive infrastructure spending? Because they know the stimulus isn’t going to produce much infrastructure, and the existing capacity will be far more the sufficient to handle the building that will occur.

6. Is jessap a troll? No, jessap has a different perspective. Jessap probably bought a long time ago and could not really care whether the value of the home purchased many years ago drops by 50%, it’s still worth more than he thought it would be so he’s happy. Anyone buying today would be nuts to not worry about that.

In support of jessep… I do know quite a few all cash buyers. I’m surprised that exSFer doesn’t know more given how many well off friends he has (do they buy stocks on margin too?).

I also know a few RE investors who own their own homes among other RE holdings and would love it if prices dropped 50% because they have plenty more cash and would use it to snap up a lot of price real estate. As one of those friends says, he’ll be the biggest buyer of SF real estate if a truly catastropic earthquake hits SF because he’ll get things for pennies on the dollar and a few years out will make a killing.

tipster – i may be wrong – but doesn’t caterpillar have a large international business that won’t be positively effected by Obamonomics? Plus no infrastructure spending has happened yet… and they need layoffs now… maybe they will be hiring again in 9 months

as for east bay… there’s plenty to like in the east bay… but if you live in an area where your home is on one side of the highway and on the other there are vast tracks of undeveloped land… that’s the east bay where some might overzealously ascribe “zero” to land value. think Mountain House as the perfect example… $1 million house in a planned development surrounded by miles and miles of land… why on earth would anyone plunk a million bucks on that? or think it could keep going up in value?

Quick math snark (sorry, engineering background): if a million people flipped coins continuously, you’d never see more than about 20 in a row.

To have a good chance of seeing 100 in a row, you’d need 10^30 people. That’s a lot of people.

I make a great living as an engineer but, without wall street bonuses or inheritances, I’ll never be able to save up enough to afford a SFH in nice SF. When the kids are born, I’ll have to leave. But renting is great for now.

ex SF-er: this thread is probably dead by now, but thought you should know (if you didn’t already) that one of your fellow Minnesotans has put forth legislation on the CDS issue. His solution doesn’t seem to be gaining much support, though:

http://www.bloomberg.com/apps/news?pid=20601087&sid=aEmXJKZFyaMY&refer=home

@Tipster

Be more objective, and don’t use terms like “snob”.

Guess what? Antioch, Vallejo, and other lower-value areas have built condos on long strips of empty land off of newly-built highways. These areas have very very low land value. They are getting hit really hard right now.

I’m sorry that land in Pac Heights is still extremely valuable, and that the 90-year old buildings that occupy that land are not really that valuable in-and-of themselves. It’s the land. And that’s why they didn’t double in price over a period of three years like all those condos that are Inland.

My parents have lived in Palo Alto for thirty years. Between 2004 and 2007, they talked about their home values “going up by a healthy amount,” but there was no doubling. Maybe it went from $1.5mil to $1.8mil.

Now compare that to places like Pittsburgh, CA where the average home price went up massively.

The bubble did not apply to “snobby” parts of the Bay Area, and we wont get hit nearly as hard, so keep waiting and keep renting.

In support of jessep… I do know quite a few all cash buyers. I’m surprised that exSFer doesn’t know more given how many well off friends he has (do they buy stocks on margin too?).

Maybe I wasn’t clear with my wording.

I wouldn’t be surprised if there are people who I know who paid all cash for their houses. But there’s nobody that did this that I know about. it’s not like it comes up at parties.

I do know people who discussed paying cash for a house, but upon further questioning one realizes that it wasn’t really a cash purchase. for instance, I have friends who did a cash out refinance on their primary residence, and used that cash to buy another place. but they still have a mortgage on their primary place… so it wasn’t really a “cash” purchase.

I have other friends who borrowed from their 401ks or from their investment portfolio to buy a house. So again, it looks like all cash but it’s not really a cash purchase (since there is debt tied to the house even though it’s not mortgage debt)

and I’m sure that I know some older people (in their 50’s or higher) who did this a long time ago as well. Clearly they can do it partially because they’re often selling their first house and taking the proceeds and rolling it into the new house. also because they have more savings. these would be true “cash purchases” (but remember, these types of home buyers often care significantly about house depreciation, as the house is their largest asset for retirement).

But I don’t know how I’d know all the details to confidently say “my neighbors and I don’t care about 50% drops because we all paid cash anyway”. especially about neighbors.

But maybe Jessup lives in a $10M condo with a bunch of other financial elite? who knows? but I clearly wouldn’t use that example as any sort of normative life experience.

===

FWIW: it’s not about buying stocks on margin. it’s about remaining somewhat liquid. I personally am fairly young (under 40), so couldn’t just plop down a million dollars on a home. even if I had the cash though, in the boom years it made more sense to put down 0-20% and then take out a mortgage, and then my investments returned far more than the interest I was paying on my mortgage.

in down years (like now) I still don’t want all my money tied up in my house. who knows what the future will bring? thus, I keep my fixed rate mortgage (30 years, 5.25% with a 0.25% reduction due to autopayment)on my house, and free cash in the bank so that I remain liquid through these trying times.

clarification:

I am not sure if my mortgage has a 0.25% or a 0.125% reduction due to autopayment. I think it’s 0.25% but there is a small possibility it’s 0.125% reduction

The difference in LMRIM’s two voices is remarkable. The paternalistic and helpful trading advice guy versus the absurdly dismissive real estate guy. Are we entirely certain Ex-SFer was the only one taking crazy pills?

you forget about LMRiM’s conspiracy theorist side… that Obama is yet another puppet whose strings are pulled by an underground secret elite who have controlled out country for many decades. That said, I love his economic posts.

exSFer… as a Realtor I see how my clients finance/pay for places, and while they are just anecdotes, they don’t mesh with most of the guesses that commenters have here… I find it’s more about personality… a conservative person will pay all or a big chunk of cash. A less risk averse person, or someone who is actively using cash for other invesments are more likely to get larger loans.

I hope that fannie and freddie start to do the streamline refi like FHA is doing. IF you are current on your loan you just need a job. No appraisal is required or tax returns. This will help the marginally underwater owners who no longer have enough equity to quialfy. The fed. needs also to keep putting money directly into mortgages so there are funds available. This will stem the tide. I think also that President Obama is building back peoples confidence.

“IF you are current on your loan you just need a job.”

Yes indeedy. No need to discriminate in lending just because a person doesn’t have a job. Having income and an ability to pay back the money is just so passe.

Yes indeedy. No need to discriminate in lending just because a person doesn’t have a job. Having income and an ability to pay back the money is just so passe.

Are you there Tipster, it’s me Diemos