∙ Treasury Yields Drop to Record Lows as Bernanke Cites Buybacks [Bloomberg]

∙ U.S. Consumers Seen Facing ‘Liquidity Squeeze’ [Bloomberg]

San Francisco real estate tips, trends and the local scoop: "Plug In" to SocketSite™

∙ Treasury Yields Drop to Record Lows as Bernanke Cites Buybacks [Bloomberg]

∙ U.S. Consumers Seen Facing ‘Liquidity Squeeze’ [Bloomberg]

Yep, all the Bernanke (short term) rate cuts have done nothing to the long end of the yield curve. Pushing on a string. So now he’ll buy treasuries to bring down 30 year rates, and hopefully help home owners refi and stay in their homes with a lower monthly payment. Or new home owners buy (at higher prices–because all people seem to care about is monthly mortgage payment).

The equity bubble that morphed into a housing bubble is now transforming in to a treasury bubble. It’s just kicking the can down the road, far as I’m concerned.

This will cause house prices to land at a higher equilibrium than if left to market forces. I’m not saying I agree, I don’t, but one thing for sure is the government believes it must take big steps early to thwart whatever economic tsunami is coming.

Maybe the new new deal will prove once and for all socialism never works. How do you think we got in to this mess in the first place?

Just because the 10-year rate drops don’t expect that to feed through into mortgage rates in a one to one fashion. The Fed is acting to lower the cost of money to it’s member banks in order to increase their profitability and provide the income stream to write-off their losses.

The governments “War on Savers” is one of the few wars that they’re actually winning.

@ Diemos: war on savers = exactly!

What do you suppose the average maturity is for a bunch of 30-year mortgages? Not 30 years, with all the refis and repayments. Probably more like 10 years.

I think this buyback is also aimed at the mortgage market (unfortunately).

I think the cost of credit to consumers and businesses is actually rising. It is not clear why we need the lower fed rate when we have injected liquidity by other means. Now it is time to raise rates so the lending starts (if Warren Buffet is going around bailing out companies for preferred stock that pays 20%, we would be wise to take that as indication of the real cost of credit… If I just borrowed money at 20%, I am sure as heck not going to lend it back out at 7%!).

The war on savers is currently being lost just as it did in Japan 1990s. Savers’ cash is worth more and more month after month in terms of RE, gas and even some consumer goods.

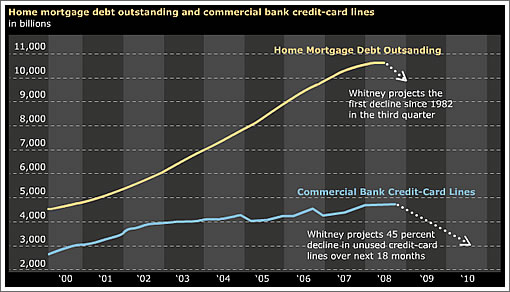

The Fed is fighting it with all its might. But credit destruction (old and new) is accelerating according to those charts. Collapsing RE prices, aversion from the banks to support unrealistic RE prices the prediction that credit card issuers will force credit lines down will precipitate this side of the equation.

This crisis is only in its first loop. We have seen only the financial results of the first crisis. Now will come the results of the overall downturn on all asset classes. Less credit + recession = lower assets prices = more recession and less credit.

The Fed will try to get us out of this sand hole by digging some more. Yeah, that will work…

The cycle will be broken when RE prices/expenses and savings rates will be back to realistic historical standards (and then some).

As I read somewhere, you “can’t patch a busted dam with water”.

The policy responses have been idiotic, and demonstrate just how little rigor and consistency there are in Bernanke’s “Fisher-ite” worldview.

It’s amazing that these fools continue to aggrandize their power without a real word of protest from the population. The average US citizen-voter deserves exactly what is coming!

Most of this criticism seems baseless. Can any of these views be defended at all?

DataDude says Bernanke rate cuts are bad, but what is the alternative. It is pretty clear that raising the rates would cause a wave of corporate defaults and put great pressure on labor markets. You seem to think there is a better way, but that is obscured to me.

DataDude says the housing and equities bubble is becoming a treasuries bubble. Sort of. Treasuries don’t sustain bubbles, so that is more like the path out. What exactly is your better bath and how does it avoid problems?

DataDude says this “will cause house prices to land at a higher equilibrium than if left to market forces”, but I can’t see any rationale for that statement whatsoever. Housing markets were supported by a mania that is already dissipating. There are many examples of properties in bubble areas falling more than 50% so far with no bottom in sight and even 2000 era prices falling away. There is no evidence for the housing or equities corrections being limited to a partial collapse.

DataDude emits something about “new deal” and “socialism” apparently without understanding what these terms mean. All this looks more like the usual implosions generated by capitalist corruption to me.

diemos doesn’t like where rates are and supposes that there is a war on savers. Lots of investors are doing well and capital gains rates are still relatively low, so there is zero evidence for that. If you just want to be lazy and put your money in the bank then you are not going to get a great rate and you are going to have problems when corruption overwhelms the system. Regulations might possibly save you, but it is quite likely that you don’t want them.

joe shmoe says that “now is the time to raise rates”, but Paul Volcker has urged caution with rates and noted that this is a very difficult situation. If Volcker is concerned about rate increases dramatically worsening systemic destabilization, then why aren’t you?

San FronziScheme goes on about the war on savers and the Fed, but it isn’t clear there is a war on savers or that the Fed has the vastly superior alternatives that you are claiming. Prices for housing and other assets have been tumbling sharply, so the correction is continuing no matter what the Fed is doing. Also, even with bailouts there is a large number of banks that have gone under.

Laughing Renter takes a swipe at Bernanke, but Volcker himself has implied that there is little room to move in this crisis. How is it that one can claim to respect Volcker while disagreeing with what he says Bernanke has been and should be doing?

Putting all this together we see that even though the most respected Fed watcher Volcker says there isn’t much to be done, the Fed is expected to wave a magic wand and make things better. The Fed is expected to be headed by someone who understands and can fix everything even though economists themselves can’t even agree on how we got into this mess let alone how exactly we will get out. Even though sharply raised rates would likely trigger a wave of corporate failures, that is supposed to be done anyway. Even though all these moves would put tremendous stress on labor markets which is what got us the New Deal and all that way back when, this time we are supposed to flush workers like crazy while embracing the most conservative possible government policies. The result of all of this will be quick stablization and high interest rates for savers.

Blaming Bernanke, socialism, a supposed war on savers, and dams made of water doesn’t make any sense. It would be as useful to claim that with respect to the bubble the color purple comes from the wind. It’s not just wrong, none of it has any actual meaning or direct relation to the facts.

Don’t say mole!!

And for the traders out there.. thinking of loading up on AIG stock — at least that’s one company we know won’t be going bankrupt!

Mole Man,

I think I agree on most of your points. Prices are still falling and the correction is deeper than anticipated. No intervention seems to stop this from happening. I think this proves that when prices fall, they do not stabilize on the median. They need to cross the median and fall some more to rebuild the median after a big run-up.

I did not say the Feds had the means to succeed. They are trying hard but I think the collapse of asset prices is too big to prevent a deeper deflation. Sure it is not a real “war on savers” but from the savers standpoint it does look like it. There’s a chance for good behavior to be rewarded, encouraging an upcoming virtuous circle if only it was allowed to thrive.

All the talk about regulation always misses the mark. The Fed and the USG have had the means to regulate whatever they want at least since FDR packed the Court in the 1930s (technically, he cowed the Court into accepting massive Federal control over commerce through a “revolutionary” rewriting of the Constitution by the credible threat of expanding the number of justices on the Court).

Why didn’t they “regulate”? The answers are pretty clear IMO.

Either the regulators are not smart enough to figure out how to do it correctly within the current structure of our political system (that is undoubtedly true – no politiburo is smarter than the market when it comes to deciding how to allocate capital efficiently, and that is EXACTLY what interest rates represent as they should be a reflection of society’s time preference for delaying consumption now in order to invest and produce more in the future).

Or, the system is corrupt, in that it has become a corporatist model where large entrenched interests use the USG and the Fed in oder to ensure outcomes desirable to those interests (all under the guise of “helping” the economy, smoothing the cycles, ensuring aggregate demand, and all the other inteventionist-constructivist sacred cows). IMO that is undoubtedly true as well.

The sensible move economically is for the Fed to close up shop, go home, and allow a truly competitive market for money to arise, just as with any other commodity. (And there’s no reason there can’t be multiple currency systems, just as there are different brands of bread.)

Of course, that is not going to happen, and no one who believes in a libertarian/hard money approach to economics thinks it will. That it is infeasible is no criticism of course worthy of addressing, as it is impossible for Keynesians to ever throttle back aggregate demand during periods of boom by running government surpluses. Neither the Fisherite school (monetarist, Keynesian, etc.) nor the Austrian approach offers a practical solution, but at least the Austrian approach is rigorous and seems to have better predictive ability.

Anyway, as I have been saying for a while, the US economy is toast now, and it will go into a secular decline. Housing prices are the least of our concerns (which is going to become clear over the next few years).

“Or, the system is corrupt, in that it has become a corporatist model where large entrenched interests use the USG and the Fed in oder to ensure outcomes desirable to those interests”

The Achilles heel of all economic systems is that they require an unbiased referee to function and the rewards for capturing and subverting that referee are enormous. So society goes through an endless cycle of renewal, growth, corruption and fall. Really, “Systems of Survival”, Jane Jacobs, you’ll find it interesting.

@ Mole Man

Thank you for your mostly snark-free rebuttal. I will reply in kind.

You’re right that all the intervention doesn’t seem to be helping.

The Fed’s job should be to control inflation. Period. They do this by raising and lowering interest rates. Greenspan decided to overstep his job. Instead of focusing just on inflation, he kept rates low to stimulate the economy. This is part of why we had an equity bubble: when rates are low, investors favor stocks over bonds, which drove up equity markets. Plus companies and consumers take on more debt, for investment or to buy goodies, which drove up equities. Low rates also fueled the housing bubble.

While the Fed can use interest rates to tame inflation, it’s much harder for them to prevent deflation. So in the face of falling prices, Bernanke doesn’t have a ton of options right now, thanks to the asset bubbles Greenspan helped create.

In terms of what’s the better path, I’m afraid it might be too late. The better path was for Greenspan to keep rates higher and stick to his job: inflation tamer, not stock market magician. The better path was for Congress not to seek creative financing ideas from Freddie and Fannie so that people who can’t afford homes could afford homes, all these so-called toxic mortgages. And while I agree with you that corruption contributed to our current woes, I would argue that it was government intervention (Greenspan, Freddie, Fannie) and not capitalism that fueled the fires.

When it comes to home buying, most people look at the monthly mortgage payment to gauge affordability. Therefore, a housing market with lower mortgage rates will settle at a higher equilibrium price than a housing market with higher mortgage rates. Agreed?

By buying treasuries, the Fed is trying to pressure mortgage rates lower in hopes that housing prices will bottom out at higher price levels. This will also help people facing foreclosure: they can refi into lower monthly rates and will be less inclined to walk away because they’re less likely to be underwater.

I’m not sure the credit clog is as big as everyone makes it out to be. From everything I see, qualified consumers and companies can get credit. So it’s not a clogged drain, per se. The problem is that many companies and consumers are becoming less and less credit worthy, so why lend to bad apples who can’t repay? Even though short term rates are almost 0%, this means little to hopeful borrowers, because lenders aren’t lending at 0%, they are pricing in huge risk premiums. So Bernanke’s rate cuts will probably have little effect on whether companies default or not. Again, your point that intervention doesn’t seem to be helping.

The Gov has already put $8 trillion at risk in this bailout, and I’d guess we aren’t even halfway through. So, here’s a quote from Thatcher that I’ll leave you with:

“The problem with socialism is that you eventually run out of other people’s money.”

I meant to chime in somewhere after the Citigroup bailout. The real question in my mind are all of these bank assets so vast and complicated that it’s unknowable how much it will take to eventually fix it?

Wouldn’t it then be better to simply guarantee all the deposits as well as other transactions that were riskless or close to riskless and let all the major banks fail?

Right now it seems like we are printing money to try and get lending going again but at the expense of destroying the world’s currency with no real progress being made on the inherant problem.

Would it not be better to just spend the money on economic stabilization and perhaps create a temporary 100% government owned bank while all these other banks go into liquidation?

Sure it would mean no CP market, no high yueld market etc for 4-8 quarters but that’s sorta what we’ve got anyway right? So instead of pumping in all this fake money to try and salvage these poorly run banks. why not let some new ones form and use the government to fill in with a wholly owned new bank to provide credit while new companies and banks are formed to fill the gap of the bankrupt institutions.

Right now- we are letting no banks fail. Which is exactly what happened with the crisis in Japan. they supported all their banks no matter how badly they lent out–and they still have not come out of this crisis. We swore we would not make the same mistakes Japan did- but it appears we are doing the exact same thing.

@ Laughing Millionaire Renter in Marin, you sound suspiciously like Satchel….

He is Satchel. How he ended up with that long-winded name is unknown …

The real question in my mind are all of these bank assets so vast and complicated that it’s unknowable how much it will take to eventually fix it?

Cooper, I know you are asking a rhetorical question, but clearly the answer here is “yes”

Would it not be better to just spend the money on economic stabilization and perhaps create a temporary 100% government owned bank while all these other banks go into liquidation?

I’ve brought this up before. it is possible that nationalization is our best course of action. (a la the Swedish Model) it will be overwhelmingly painful to our economy, but our economy MIGHT survive nationalization of the banking system.

Wouldn’t it then be better to simply guarantee all the deposits as well as other transactions that were riskless or close to riskless and let all the major banks fail?

the one difficulty here is that as banks are about to fail they then offer way-above normal interest rates on federally insured vehicles (CD’s, etc). then they steal the “hot money” and fail leaving the FDIC or similar with the bill.

That’s how I knew which banks to short this year. I watched their CD rates. I basically shorted every bank with high CD rates. works like a charm.

Right now- we are letting no banks fail. Which is exactly what happened with the crisis in Japan. they supported all their banks no matter how badly they lent out–and they still have not come out of this crisis. We swore we would not make the same mistakes Japan did- but it appears we are doing the exact same thing

agreed. but we’re doing even WORSE things than the Japanese. Not only are we “recapitalizing” these zombie banks, but we’re paying premiums and giving bailouts and so forth..

In my view we really have 4 options

1) nationalize the banks (what cooper suggests and what I’ve suggested before) with one caveat: the govt shouldn’t create a federal bank. it should nationalize the ones we have and wipe out all shareholders, bondholders, etc. Also clawback bonuses and what not. Then break the newly nationalized banks down to simple transaction entities. Checking, saving, vanilla loans, leters of credit, etc. Just enough to keep the “real” economy from crashing.

2) liquidate everything (what many of the Austrians espouse)

3) “recapitalize” the banks using taxpayer money and then use partial govt control to force the banks to lend. in other words socialize the risk and privatize the profit, but then have partial govt control

4) do a Frankenstein combo of recapitalization and “free marketeerism” which will quickly degenerate into handouts to the politically connected and creation of mistrust due to zombie entities. (this is the path we are on).

The big problem is becuase the government has been intervening so much –we have not had any kind of over correction phase. Every bear market ends with a over correction but we can’t have it because the government is tinkering.

Also i do think that the regulators in treasury and the Fed won’t consider letting these institutions fail becasue they are too close. Sort of when Franklin went to France

Mole Man, I am worried about everything, but the fact is that end rates to borrowers are rising and a growing spread between the fed rate and the rate to non-bank borrowers tells me lowering rates is wrong– especially when the treasury is going around handing out money. It also creates a moral hazard when the banks have such a vastly lower cost of borrowing, but are performing so badly. There is also a danger that spread will become entrenched and make it much harder to get out of this situation.

Frankly, Obama’s responsibility is to talk a consistent line about the economy and convince people that some particular course of action will fix things and then take that course. More than likely that will work.

In the short term it would be great if Paulson could just shut his mouth for a few days. As long as chicken little keeps running around saying the damn sky is falling, the damn sky is going to keep falling.

ex SF-er, another good post. I’m with you and cooper. I’d support your option 1 with a little (or a lot) of option 2. But you’re right that what we have is a Frankensteinian mess. Paulson can and will do plenty more damage in the next 7 weeks.

since the alternate handles appear to be all the rage now:

thought I would post this:

http://online.wsj.com/article/SB122833771718976731.html

suffice it to say if this comes to pass, our problems are just beginning, and may never end

Man I need to get me some of that 4.5% government cheese. Here I am paying 6% like a sucker but can’t refi because it isn’t likely that I have any equity left and don’t qualify for a loan modification because I can easily afford my payments because my housing costs are only 28% of my income.

Now I’m stuck making payments I can afford on a place I like while everyone around me gets a bailout. Oh well at least I got me a nice new alternate handle.

That is a great new handle. I wish I would have done something like that.