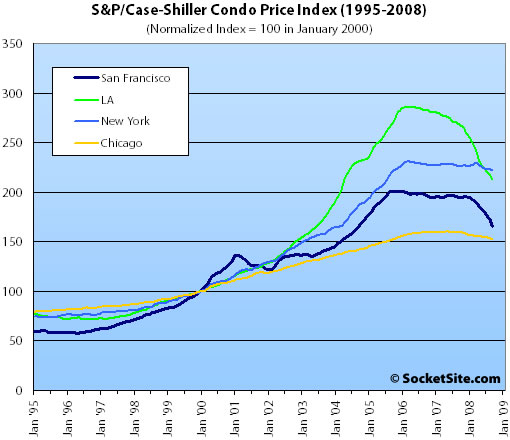

According to the newly released S&P/Case-Shiller Condo Price Index, condo values in the San Francisco MSA fell 3.3% from August ’08 to September ’08, are down 15.0% on a year-over-year basis, have fallen 17.2% from a high in October 2005, and have dipped below levels last seen in October 2004.

The SocketSite S&P/Case-Shiller condo footnote: The Condo Price Index includes San Francisco, San Mateo, Marin, Contra Costa, and Alameda in the “San Francisco” index (i.e., the greater MSA) and is imperfect in factoring out changes in property values due to improvements versus actual market appreciation (although they try their best).

∙ S&P Launches Condo Indices; Adds Seasonally-Adjusted Data [S&P]

∙ September S&P/Case-Shiller: San Francisco MSA Decline Continues [SocketSite]

I posted this in an earlier thread, but it’s interesting how the condo data shows a much smaller decrease in value than the data for all homes. As SF has a disproportionate number of condos, this is more evidence that it home prices in the city have held up better than the generic CS numbers would indicate. We wont know until they start publishing data by city or zip, but SF seems to still be holding up relatively well.

My guess is by December the San Francisco line will be at or under 150. The line is already headed in that direction, and this doesn’t even include the October meltdown.

Considering the SF line started in January around 200, that’s a 25% decline.

So, yes, the SF condo market has held up well, until year 2008, where it falls off a cliff.

If you adjust for 3% inflation per annum since 2000 and assume 2000 prices as FMV, it implies a further decline of 16% in SF, 37% in LA and 44% in NY. Of course, if this happens any property purchased or refinanced in the last seven years is underwater…

DataDude has it right. Since this graph is scaled over such a long period of time, it somewhat masks the big drop starting in late 2007 in SF. Just as with SFRs, the SF condo market is tanking right in line with the rest of the state, but it started about a year later and is now picking up speed. If you graph this for a shorter term, say since 2006, the picture is very different.

wow, five comments and no one has made the “can we see just SF county” comment on CSI thread … color me impressed

I wonder if the data here is totally accurate.

Surprised to see LA being more expensive than SF. It should not be.

ester:

The CSI data shows the “increase” (and decrease) in price not the “actual” price of condos…

ester, remember it’s the LA MSA and the SF MSA not just the specific counties. Condo’s in SF might have been ridiculously expensive but that did make condos in Oakland (or Vallejo etc) ridiculously expensive.

“If you adjust for 3% inflation per annum since 2000 and assume 2000 prices as FMV, it implies a further decline of 16% in SF, 37% in LA and 44% in NY.”

That math seems about right, but if you index at inflation + 2% (which seems like a better proxy for real estate appreciation), it suggests that prices are only 5% higher than they should be.

BTW, this assumes appreciation in SF proper over the years was as high as this MSA chart indicates….which I personally don’t think it was. In other words, we could both be overstating the extent of any remaining decline. I guess time will tell.

I don’t think we can assume 2000 represents FMV for SF prices. If you take a look at the other CS graph posted yesterday (the one that dates back to 1987: SF MSA vs. Nation) you’ll see that for SF, prices increased about 10% in 1999 and 30% in 2000.

Anybody who lived here in 2000 will remember that there was about 0% vacancy in rentals. To buy a house or condo, you had to bid way over the asking price and accept no contingencies. Agents would set a bid date and collect 10 – 20 offers from buyers, fostering an auction mentality that drove prices up.

Times have certainly changed, but maybe not in the minds of sellers, because many of today’s sellers were yesterday’s buyers who jumped in to SF under these ridiculous hyper-inflated conditions.

Wow, this graph is MUCH better than previous ones, because it is obviously more focused on SF proper.

My initial reactions:

*Prices on these condos never went up as high as did SFH, so the drop wont be as bad.

*Prices flat-lined for years, unlike SFH, which peaked then fell. This means that appreciation is no better than SFH, but the pain of dropping wont be as bad.

*Assuming we get back down to the 150-level soon, how much lower could things go? Over the course of nine years (2000 – 2009), you expect about 50% appreciation, which is what SF condo owners will experience this decade…

Looking at this graph, 2000 had already seen 10%+ increases in prices since ’97. Some of it was a catch-up from the very soft 91-97 market but most of it was a side-bubble was related to the dot-com bubble. It started to pop in 2001 but the MoaB prevented that from going its full course.

In short, we had a bubble on the top of another bubble. Of course, SF has changed a lot in 10 years and a chunk of the increase is justified.

But I don’t think we can say “fair market” is 2000. If a monetary bubble is inflated ($100Bs rescues coming weekly), then prices will stabilize sooner. Maybe 2002? If they fail in this scheme, I’d suggest running for the hills if you haven’t done that yet because 1998-2000 here we come.

@ NewBuyer – my guess is SF condo prices flat lined in 2005 due to so much condo capacity being added. The supply curve kept moving to the right. Does anybody have numbers on how many condos were added to SF’s inventory by year?

It’s easy to add condo inventory (build a new multi-unit building like in SOMA).

But it’s difficult to add new SFR inventory (where does new land come from in a city surrounded by water on 3 sides?).

Because there is such a glut of condos, my guess is condo prices will fall by a greater percent that SFR in SF.

I don’t understand comments like “*Prices on these condos never went up as high as did SFH, so the drop wont be as bad.”

The drop doesn’t depend on the rise, it will bottom out based on a variety of factors: fundamentals, desirability, salaries, etc. Condos are less desirable and plentiful than SFRs; I therefore see no reason why SFRs will fall by a greater percentage than condos.

2001 gave us a taste of things to come in the SF condo market. Despite a rapid easing of credit and lending standards, the poor economy from the dot-com bust nevertheless drove down prices significantly. The downturn we’re entering today dwarfs the short and mild 2001 recession. Condo prices need to fall about 40% to bring them even close to in line with comparable rental rates, and rents are likely to drop considerably as well in the recession, as they always do, further pressuring prices. We also have a ton of new buildings, and you can’t buy anymore with nothing down (and no-down loans have been widely available since the late 90s). We’re in a triple-whammy: deflating bubble plus dramatically reduced numbers of qualified buyers with the new down payment requirements plus serious recession. And you can add the Alt-A recasts to make it a quadruple. I would place Fronzi’s worst case scenario as the most likely.

My guess is that we will blow through 150 and maybe begin to level out at ~125, but this will not be the bottom. We could possibly dip to around 75 when all the option ARMs recast next year and beyond.

@ Trip – what’s the deal with Alt A recasts, please explain? When is this likely to happen?

Condo prices are a function of supply and demand. The supply curve (sellers) kept getting pushed to the right with the addition of new units year after year. Plus, owners who were just laid off or facing unaffordable loan resets will sell, pushing the supply curve further right.

The demand curve (buyers) is now being pushed to the left for many of the same economic reasons, plus it’s harder to get financing. And down payments have been wiped out. Plus, many buyers will wait for prices to fall more, or will opt for rentals that are becoming cheaper.

When the supply curve moves left and the demand curve moves right, prices fall dramatically. The curves won’t move as much for SFR, but they will move. Therefore, condo prices will fall by a much greater percent than SFRs in SF.

When we talk about recasts, we’re talking about a simmering problem in areas, such as SF, where certain types of Alt-A loans were common. In brief, many such loans (neg-am, pick-a-pay) permitted the borrower to pay no principal for a number of years and often also included a teaser interest rate for a few years on top of that. Those are now starting to “recast,” meaning the principal will now start coming due (and at increased payments since it has been deferred) and the teaser rate will adjust higher. This will increase the monthly payment considerably, perhaps doubling it. And one cannot refi out of the problem since most of these were no-down loans and a refi requires 20+% down. This is our “subprime” problem, and is likely to result in significantly more units put on the market, either through foreclosures or because the owner simply cannot afford the new higher payments. It We are just entering this period, whereas the subprime problem (a different but related problem) started hitting a couple years ago. Here is a good synopsis:

http://calculatedrisk.blogspot.com/2008/08/reset-vs-recast-or-why-charts-dont.html

Another issue behind Alt-A is the “no-docs” element. You could make 50K and claime to be making 200K to get approved for your loan. If you need to refi, I doubt they’ll let you lie on your application like the good-ole-days.

A lot of the Alt-A were done with the “hopes” that:

– Prices would appreciate and you’d profit for over-extended leverage

– You could refinance when/if needed using the same trick.

Alt-A had a reasonable purpose. Not everyone is salaried. There are more and more commission/fee-based jobs and you have to cater to that crowd.

But it was used and abused by “specuvestors” doing a bit of flipping on the side of their day jobs. Think a Realtor or a Contractor buying a fixer who redoes it completely all high end to resell it with a huge mark-up. Some did it with Alt-As.

While I NewBuyer may argue that this focuses more on SF proper because condos are a much larger percentage of transactions in SF than in other components of the MSA, I would argue that the data might be skewed dramatically because in other parts of the MSA houses can be had for what you used to pay for a condo in those markets. Said differently, condos in these other markets (e.g. Contra Costa) may have taken huge hits and may be skewing the data.

So once again, as I did during the run up, I will bemoan the fact that the CS index is not granular enough. I would prefer city or census tract level data. You can’t make any more of this data than broad regional trends.

@ Trip – thanks. These charts are great (although they’ve probably changed a wee bit with refis and Bair/FDIC intervention). And these definitions are also helpful:

“Reset” refers to a rate change. “Recast” refers to a payment change.

Recasts peak in 2011 — which is why most experts say that’s the year housing will bottom out (even though the politicians are saying the bottom is coming sooner: next year).

It’s one thing to roll an ARM into a fixed–because the remaining principle gets repaid, just at a lower constant rate.

But with neg-am and pick-a-pay, in addition to the rate resetting higher, the principle has actually grown! Dear dog, how could anybody ever think that was a good idea? I wonder if we taxpayers will have to eat this increase in principle so that owners can stay in their homes?

DataDude, you are exactly right. These are a ticking bomb and an absurd product. On your last point, so far, the government has not been too keen on bailing out individual borrowers. That very well may change (but who knows). Regardless, I think it is quite unlikely that any bailout would extend to the $1 million-plus homes that are the norm in SF. That would never sell to the 99% of the country who can’t envision spending that much on a home. And the odds are nearly nil that any bailout would extend to non-occupants. This will be a big factor in continuing declines in SF housing.

DataDude,

Upside-down mortgage holders are not owners. They are renters with a lien.

“*Prices on these condos never went up as high as did SFH, so the drop wont be as bad.”

I think you are being misled by two things:

1) The graph of condo prices rose from 100 in 1/1/2000 to 200 at the peak. The graph of mid tier home prices rose from 100 in 1/1/2000 to 220 at the peak. Not much difference there. It just wasn’t as bad as LA. You are seeing the flatness of the graph because it has been scaled to show LA, which rose more.

2) The graphs above are for the MSA. Home prices in SF doubled while home prices in Antioch tripled, that was because everybody in the burbs wanted a home. So the MSA SFR stats skew higher than SF prices, and that means SF SFR prices aren’t falling as fast as they are for the MSA.

But for the same reason, in Antioch, condos weren’t as popular as they are in SF. So SF condos likely appreciated more than they did in the burbs. Therefore, condo prices in SF will likely fall more than condo prices in the burbs.

A lot also rides on jobs and where the layoffs of 2009 centered. So it’s not very wise to read too much in the statements above, as anything can be quickly overwhelmed by layoffs.

from a TA standpoint, looking at that chart, i would fully expect SF and all of the markets except maybe NY to hit 100 in the next 2 yrs

From a fundamental standpoint (home price vs. income)(home price vs. rent)(historical appreciation)(home price appreciation vs. employment trend lines)(credit availability), it looks clear to me that we will hit 75 in the next 3 yrs or so.

Caveat: govt intervention. who knows what those idiots will do to screw up the way markets naturally work

@ San FronziScheme

Excellent distinction: renters with a lien 😉

But don’t forget property taxes, maintenance and insurance, to add insult to injury.

Ha Ha Ha, stupid homeowners. Laughing at others misery= SS holiday spirit. Can’t wait til X-mas (X-mas ’12 that is ;))

Just a quick note on adjusting for inflation (paraphrasing my Econ textbook): If you adjust for inflation you may get a lopsided result if you don’t also adjust for wage/salary changes during the same period.

Can’t imagine the wage/salary changes since 2000 make the trend any rosier!

Inflation generally refers to changes in the CPI, which is a measure of price changes for a basket of goods and services consumed by households. The CPI does not include housing.

One of the great lies of the last 10 years is that inflation has been low. Huh? Yes, maybe bananas and long distance calls are affordable for most Americans, but housing is not.

I don’t understand why some say this chart needs to be adjusted for inflation. THIS CHART IS INFLATION. Housing inflation, not CPI.

@DataDude, Welcome! For a little perspective on the magnitude of the problem locally (put down all hot liquids before reading):

In the Bay Area, almost three- quarters of mortgage loans taken out last year [2005] allowed borrowers to delay the payment of principal and, in some cases, interest, according to data from San Francisco research firm LoanPerformance.

EB guy,

Great article find. That was a gem to read.

Actually, the CPI does include 2 elements for housing:

– Rent of primary residence (rent)

– Owners’ equivalent rent of primary residence (rental equivalence)

from EBGuy linked article:

“In the 25 years we’ve been making that loan, I can’t identify a single delinquency that is due to the structure of the loan,” says Herb Sandler, the company’s co-chief executive”

see, there’s nothing to worry about.

btw. Herb Sandler personally made $2.4billion from the sale of his company the year following this article.

One thing about the toxic alt a’s is if you are adjusting today, your rate is pretty good…MTA at 2.25% plus 2.5% is a 4.75% fully indexed rate.

I refied out of a negam in 2005 into a 30 year at 5.75% (with a 10 year IO option) so am included in KP’s scary numbers but not sure they should count these loans as toxic. There were many 30 year fixed with 10 or 15 year IO periods in 05 and 06.

I think the reports on the alt a situation may be somewhat overblown. I do not fully trust the anaysis to account for all the refi’s and sales that have been done post origination of these Alt A loans. Time will tell…

@ San FronziScheme

You’re right, rent is included in the CPI:

http://www.bls.gov/cpi/cpifact6.htm

If I understand correctly, rent is given a relative importance of 32.8% and owner equivalent rent is 23.8% — meaning in most of the country, it’s cheaper to own than rent. Plus, my guess is that in the Bay Area, people spend a greater portion of their income on housing. So the CPI includes housing, but since it includes the entire nation, it understates the housing inflation of San Francisco or New York, for instance.

Said differently, if the CPI were based on the baskets of goods and services consumed by a San Franciscan, including housing, inflation wouldn’t be 3-4%, it would be double digit.

agreed peanut gallery,

I’m in this group as well my rate isn’t as good as you posted, it’s 4.9%. But, this makes the monthly so low that the original minimum is now larger the the neg-am option, and the interest only option. So, basically most people are paying off their loans although very slowly. Certainly not toxic though. The real Alt-A apocalypse will only occur with high interest rates.

from the article linked in my name: Sept 2008

“Alt-A loans fared comparitively worse, with 2006 vintage first liens recording 60+ day delinquencies of 25.26 percent, up 9.44 percent from the prior month; the 2007 vintage saw delinquencies rise a whopping 16.43 percent to 22.65 percent, Clayton said.”

this is when interest rates are at an historic low.

“It is becoming increasingly apparent that lenders and trustees can either no longer process all of their foreclosures, or are purposefully delaying the foreclosure process,” said Sean O’Toole, founder of ForeclosureRadar.

The recast or reset of option adjustable (neg-am) loans is not the only problem with these products. Another problem is that these products are currently no longer available. If a home owner can afford a house only with a neg-am product he is in trouble if he needs to sell even before his payment changes.

With the recession there haven’t been increases in salaries. The fall in the stock market would result in few buyers flush with cash from exercising their options. A buyer would likely need a neg-am loan to be able to afford to buy at these prices.

many of the loans taken out in 04 and 05 were at very low interest rates. One of mine was at 4% FIXED. I know that some people are underwater, on paper, but if the payments are affordable, I believe many are able to ride out the national meltdown in our economy. prices have not tanked as much as other parts of the country for a reason. I realize many posters are waiting for even more of a reduction, but how bad do things have to get on a national level (they’re pretty bad right now) before values fall 30-40% gien that this study only shows 17% decline from a high in 10/05. I for one am hoping things have hit bottom because the alternative is really a disaster. Prices could be $1.00 but that may still be out of most people’s reach when there is no money.

I agree you can’t get these loans anymore, but if you got it in the first place the payment has gotten better. bobT, my interest payment now is over $1000 less than it was in 2006. Like I said it will be interest rates that drive this not re-sets.

I don’t think we’re anywhere close to a bottom. Sacramento might be. But we’ve got a lot of bubble excess still to shed here in SF.

But Gavin and sparky both make good points. First, a lot of people who are walking away from loans are not doing so because they can’t afford to pay. They’re doing it because they’re underwater. Many locals may be current now, since prices are down just slightly in SF. But when the place next door sells for 20% less than you paid in ’07, what’s your incentive to keep paying? I bet foreclosures will continue to rise here even without adjustments/recasts. That’s also why redefault rates are so high on loans that have been worked out.

I think the reason so many of the 2006-2007 vintage Alt-A loans are going bad isn’t people not being able to afford the payments but people bailing out on houses that are worth less then they owe on them.

The Bay Area suffers from a “gold rush mentality” perhaps more than any other place on the planet. Young upstarts move here with dreams of striking it rich on technology stocks. They can move away, just as quickly.

Most of them are smart enough to do the math and figure out when it no longer makes economic sense to live here.

viewlover – you may _believe_ that people can afford their payments. the data is beginning to suggest they can’t. or they are choosing not to.

sparky: you may be better off, that’s great. but the data is suggesting that increasing numbers of people aren’t.

facts are stubborn things.

Everyone has a different bubble narrative, here’s my take:

And I looked, and behold a pale horse: and his name that sat on him was Fraud, and Casey Serin followed with him. And power was given unto them over multiple primary residences, to inflate with false appraisals, and with negative amortization, and with no money down, and with low initial rates.

This bubble is about inventory being removed from the market by marginal players and forcing up home prices. These players will hang on until the recast or negative cash flow forces their hand. Most do not even live in their “primary residences”. I believe there are plenty of these folks lurking in the Bay Area (thanks to Alt-A loans) and that they will continue to be a controlling force in this market by driving up inventory through foreclosure sales.

I’m sure there are many responsible borrowers like view lover who did fine with these neg-am type loans. But there are many others who were simply gambling on perpetual appreciation. The units they bought will be dumped back on the market — voluntarily or involuntarily. The whole Alt-A concept was really based on a ridiculous premise — because you’ve handled very small amounts of credit and thus have a decent FICO, we’ll give you a massive loan that you (effectively) don’t need to start paying back for several years . . . and you don’t even have to document for us your income or ability to ever pay it off. Doomed to blow up from the inception. Those who think this will not be a major drag on the market are in denial.

Lastly, it will not be a disaster when things correct, even if prices fall as much as I suspect they will. Prices in Sacramento are down 50%, and life goes on. Just means people can get back to living in homes rather than treating them as a slot machine.

That didn’t happen in SF.

It certainly didn’t happen in the firestorm area of the Berkeley hills ($1million+ homes) either…

Anyone care to guess/ provide an opinion where this puts the new condos on the block – selling price wise? Does the Tishman has deep pockets theory still hold true? What about ORH or Millenium?

Wow, that’s a steep downward slope on the SF graph, and that’s before the meltdown.

Nothing much sold this month: how many months before prices catch up to the new reality and we see even steeper drops?

You guys are crazy—condos in SFO need to go down another 50%…index value of about 90 or so.

I don’t have negative amortization loans. I did once but only for 1 year, interest only. I made the first payment before the due date and it reduced the principal so after a year I refinanced again and the principal was slightly lower than where it started. That was playing with fire but really helped with cash-flow. I don’t think they caught on to that trick. I have alot at stake in this market so I’m optimistic, but not really that dumb. But like many in my situation, I’m not selling unless I really need to, and I believe there are many people in my situation. People make and lose money all the time and then we die anyway, can’t avoid it.

Only about 7800 SFH’s were sold in San Francisco in 2005, 2006, and 2007 combined — a tiny fraction of the overall SF housing inventory. If even as many as 10% of these loans/homes are in trouble that’s, what, 800 homes? You people think that comparatively tiny number of at-risk homes will bring down the SF housing market?

The penchant for hyberbole here is breathtaking.

Hey, is the editor really deleting my not-that-snarky comment? I guess even being slightly less pessimistic than the average poster here is no longer tolerated, I understand. I can take my time and attention elsewhere. Good luck all, in whatever your endeavour may be. Don’t spend all your time in an echo chamber, try to get some alternative perspectives.

[Editor’s Note: The aforementioned “not-that-snarky” comment in its entirety:

As always, it’s not a matter of being bullish or bearish that resulted in its removal. The “lines meeting” bit has been done to death and is more likely to detract rather than add to the discussion about these indices. You’re better than that.]

Fair enough then. I think there is a reasonable discussion there but perhaps it can be approached in a different manner.

sanfrantim, you’re ignoring refis. Problem is far more significant than you think.

That didn’t happen in SF.

Forgive me, fluj, I am an ignorant plebe from the East Bay and perhaps this in not the “real” Ess Eff.

Sold on 5/27/2004 for $1,750,000 ($1,225,000 variable rate first from WaMu, $175,000 second from Greenpoint). Whoa Nelly, 20% down; that had to hurt.

For sale by bank for $1,499,900.

Forgive me, this is in Bayview, but was too good to pass up. REO (3bed + inlaw) listed for $429k.

Previously carried loans for $516k (variable first) and $129k (fixed second).

What did you say tho? Seema to me you said Casey Serin, multiple primary residences, rampant unchecked speculation by unqualified amateurs. Yet here is your example, complete with “real sf” buzzword … a 20 percent down purchase? A bad play? Sure was. What you said? Not close. Your aw shucks faux east bay novice routine was duly noted, and also deemed not in keeping.

fluj,

I will give you some credit as I pulled up Trulia and was truly shocked by the lack of green “foreclosure” pushpins in “SF proper”. Clearly the outright fraudsters were more on the periphery (see Bayview listing above for Casey Serin-type leverage). Ess Eff is a more sophisticated crowd with speculation involving real skin in the game (see condo tower reservations, TIC developers, and ‘homesitters’ to be done in by the ARM recasts).

EBGuy, Trulia’s “pushpin” tool is odd. The broad view of the whole city doesn’t really show anything. Zoom in tighter and scroll around — you’ll see loads of green pushpins all over the city.

Oh, they’re there, just a bit sparse for my taste (like, ya know, Piedmont sparse in East Bay parlance).

Also, is this an SF Used Home Salesperson conspiracy (or am I just missing the boat)? In the East Bay MLS advanced search options there is a REO check box. Can’t seem to find it in the SF MLS (and Redfin only gives me some listings in Daly City). This really cuts down on my propertyshark fun…

I think that SF prices will hold steady despite and overall decline in the housing market due to its population density and scarcity of developed land.