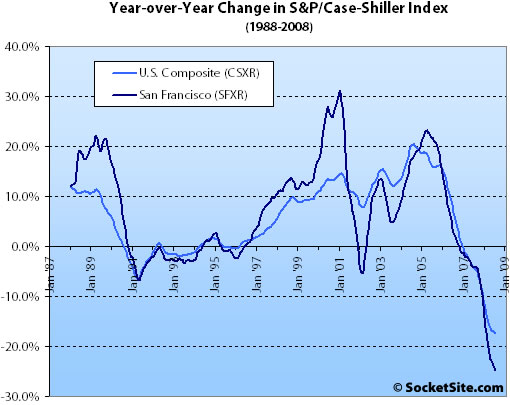

According to the July 2008 S&P/Case-Shiller Home Price Index (pdf), single-family home prices in the San Francisco MSA fell 1.8% from June ’08 to July ’08 and are down 24.8% year-over-year (once again, a new record low).

For the broader 10-City composite (CSXR), year-over-year price growth is down 17.5% (having fallen 1.1% from June).

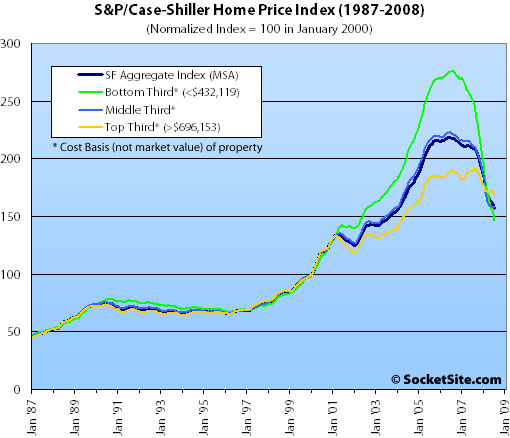

Prices fell across both the bottom and top price tiers for the San Francisco MSA while the middle tier was unchanged. The bottom third (under $432,119 at the time of acquisition) fell 4.1% from June to July (down 41.3% YOY); the middle third remained unchanged from June to July (down 25.2% YOY); and the top third (over $696,153 at the time of acquisition) fell 0.6% from June to July (down 11.1% YOY).

And according to the Index, home values for the bottom third of the market in the San Francisco MSA have returned to May 2002 levels, the middle third remains at December 2003 levels, and the top third is approaching February 2005 levels.

The standard SocketSite S&P/Case-Shiller footnote: The HPI only tracks single-family homes (not condominiums which represent half the transactions in San Francisco), is imperfect in factoring out changes in property values due to improvements versus actual market appreciation (although they try their best), and includes San Francisco, San Mateo, Marin, Contra Costa, and Alameda in the “San Francisco” index (i.e., the greater MSA).

∙ Continued Record Home Price Declines [S&P]

∙ June S&P/Case-Shiller: San Francisco MSA Continues Decline [SocketSite]

Why is it that the S&P index continues to decline, but homes where I look in Russian Hill for example continue to stay stubbornly high?

Is this really the SF index, or are there other parts of the Bay in this index? Honestly, I don’t see much of a drop if any in San Francisco.

If I was Congress, I’d vote NO on the bailout too. I don’t care of Main St. gets crushed. It’s all about survival of the fittest. It comes down to job survival, and if you’re an underperformer, then you must be weeded out for the good of the economy.

Roger, are you fluj?

Read the posting. Yes, the index includes neighboring counties. And you are either yanking our chain, or blind, when you say you don’t see any price drops in San Francisco. Heck, even the realtors stopped trying that one more than 6 months ago.

Roger,

See the editor’s footnote: SF includes Contra Costa, Alameda, etc.

Thnx Sparky. I see it now. Also interesting to note the “top 3rd” is outperforming the other two categories. I guess not even the “top 3rd” is purely SF. It would be great to see a purely “SF” chart then.

Good to see the markets rebounding! Survival of the fittest!

The top third has been stable at March 2005 levels for 6 months now.

middle tier is also stabilising it seems.

How is continued decline “stable”? Month to month data points do not make a trend.

We’re nowhere near a bottom, except in outlying areas where sales have picked up.

Here are the “top tier” numbers for SF since that tier’s peak in August 2007:

8/07 191.29

9/07 190.78

10/07 188.51

11/07 182.65

12/07 178.88

1/08 175.75

2/08 171.32

3/08 171.25

4/08 170.87

5/08 172.36

6/08 169.95

7/08 168.93

Down just under 12% in 11 months.

January 2000 was the baseline, at 100. February 2005 was 166.42. March 2005 was 172.01.

Draw whatever conclusions you will from those numbers. My prediction: it has all hit the fan much more strongly since these numbers (which are 2 months in arrears and which are not seasonally adjusted). We’re entering a recession (or depression) and the recent declines hit even when the economy was relatively strong. Jumbo rates are higher and lending requirements have only continued to tighten. My 2 cents is we’ll see the decline in the top tier in SF accelerate and surpass the lower tiers, which will also continue to decline but perhaps more slowly. This is exactly the pattern we saw in other markets that have been hit hard — Las Vegas, L.A., San Diego. The downturn hit the lower tiers first then the top tier around 8 months behind. SF simply started this pattern around a year after those other markets. The growing spread between conforming and jumbo loans should move this process along even further in SF. The looming Alt-A resets will also be a bigger deal here. We’ve already started to see all this develop with the growing inventory and increasing number of reductions.

easy one roger,

look for the remodelled unit that’s dark/damp and for sale after 1-2 years, maybe no parking and located in ‘real’ bernal or ‘real’ glen park-that’s where you find the price declines.

My personal experience is very different from this index. I bought a 2/2 TIC with parking on the Preside side of Pac Height for $620K in Q405 to Q106. 1300 sq feet. Tell me where in Pac Height can you find a deal like that TODAY??

I still don’t understand why there isn’t a pure SF county breakdown of this data.

Frankly, they could issue data by zip code and let us mix and match the results how we like, depending on what we want to prove 😉

Given the lengths (some) folks will go to live near a muni stop, a “true” SF index would be useful, if only to gauge psychology.

thank you ester.

i wish we could get the editor to highlight apples like yours-but i guess that would not play well with the crowd…

Dear Editors,

Can you just add something about how CSI data for only SF county is NOT available so that we can end the people requesting SF only data EVERY month.

Yes, this index is bunk. I bought a 5/4 SFR in the Marina last year for $27,000. It comes with a helipad, submarine port, wallpaper made of whale leather, and has teleporters so I never have to ride the yucky bus. Tell me where you can find a pretend property like that TODAY?

Additionally, I plan to call Bob Shiller and ask hime to come out with a “My House Index” or “MHI.” Naturally, the MHI will go up 10% a year in perpetuity. Because it doesn’t matter what all the indicators say (like this index, DataQuick, even the CAR), I know that MY HOUSE has only gone up in value! Whee!

S&P could make the data available for SF only but they don’t. You can draw your own conclusions about why but a good guess might be that they don’t want people trashing or discounting their index by pulling out its separate parts in the various MSAs they have constructed. That said, the SF MSA probably has too few transactions to be meaningful on a monthly basis.

@anono

could also be due to the sample size (being pretty small)

Dude, MHI is through the roof… MHI goes up each time the contractors leave 🙂 For some reason, the bank is not returning my calls.

“Several months ago, Satchel posed a challenge that was something like to find any home in SF bought in the last three years and resold within the last 6 months at a higher price that had not been remodeled (i.e. was a true apples to apples comparison). I don’t recall that anyone ever met the challenge.”

Posted by: Trip at July 17, 2008 8:18 AM

paco?

Thanks Ester. I had a similar experience, though more recent.

Got into a 2 BR 1 Bath TIC in Lower Pacific Heights (Pine and Broderick) 6 months ago for 525K.

So I would like to know if anyone has stats on TIC, Condo price drops (if any) in San Fracisco. Not Alameda, Not Contra Costa, Just SAN FRANCISCO. And just TICs, CONDOs.

“My personal experience is very different from this index. I bought a 2/2 TIC with parking on the Preside side of Pac Height for $620K in Q405 to Q106. 1300 sq feet. Tell me where in Pac Height can you find a deal like that TODAY??”

Try puttuing your TIC up for sale and see what you get offered. There are several large 1 bdr 1 ba condos(not TICs) in pacific Heights in the 600s. I would venture to say it would be difficult to sell a 2bd 2ba TIC in Pac Hts now for much more.

Anyway, why would anyone buy a 2bd2ba TIC enar the presidio when you can rent a 3bdr house in the presidio for $3000?

Tell me where in Pac Height can you find a deal like that?

2010

Hi Trip,

Thanks for your data/analysis. It is interesting to see that August 2007 is the peak, not the prior years. Now of course, we’re 11% down from the peak, but that’s just not that scary.

What is scary was the 7% drop in the Dow yesterDAY. Most people I know just buy in live in their house and enjoy life. Not many in SF are buying b/c they want to flip. They’re buying b/c the housing stock is generally much better than the rental stock, and they just want to enjoy life.

No point working all day and not have a great lifestyle you deserve. Secret is to spend your money somewhat equally throughout your life.

It is too bad S&P doesn’t have a SF only index. More fun this way I guess.

spencer,

I dont think that you can really compare a 1/1 to a 2/2 and call them apples. I don’t have to put my unit on the market to figure out how much it is worth today. One can simply look up MLS at those that are 2/2,2/1 that are in contract.

When I do that, I can up with a rough guesstimates of $700K to $750K in TODAY’s market

What’s really interesting in this 3-tier graph:

Bottom Tier is back to 2002 prices

Middle Tier is back to 2004 prices

Top Tier is back to 2005 prices

It’s bit of a time machine. Less painful then stocks, though:

Dow is back to 2000

Naz is back to 1999

S&P is back to 1998

That’s a lost decade for stocks. I wonder if we are seeing a lost decade for RE.

typical spencer mis information

“Anyway, why would anyone buy a 2bd2ba TIC enar the presidio when you can rent a 3bdr house in the presidio for $3000?”

have you seen the rentals? i guess its b/c you don’t mind low ceilings w/popcorn, carpets, hollow doors and crap quality b/c that’s what you are used to in your rental.

show me a 2/2 in pac hgts that will sell for anywhere near this price. not on pine/bush, not “lower” pac hgts. and no, your 1/1 condo does not qualify…

Apple to apple:

there is a current listing in Dist 7 on baker street, sold last year for $260Kish (can’t remember the exact), listing now for $300K

there is another one is dist 8 that came up last Friday, and went into contract over the weekend. On taylor. sold last year for $760K. listed last week for $799K.

So, i really don’t have to put my unit on the market today to find out its worth.

“I dont think that you can really compare a 1/1 to a 2/2 and call them apples. ”

You can’t call them apples but I think a 2bd 2ba TIC is more comparable in price to a 1 bd 1ba condo, than it is to a 2bd 2ba condo

I never said that 2/2 tic is an apple to a 2/2 condo, which can be anywhere from $900K to $1.1M in today’s maket.

By the way, why would you buy when you can rent for a lot cheaper? Because with a purchase, you are locking into a fixed “rental” for the next 30 years. Where, on this planet, can you lock in price for 30 years on anything? For a 6 month put/call option, you are paying 10% of the stock price. If you were to buy a put option for 30 years, it is probaby 100X of the stock price.

“but I think a 2bd 2ba TIC is more comparable in price to a 1 bd 1ba condo, than it is to a 2bd 2ba condo”

any factual basis for this “thinking” ?

any more thoughts on crappy presidio rentals?

Fun back and forth.

Typical Case-Shiller Socket Site exchange: the tsunami is sweeping across the land and we hear the very few people on higher ground saying “tsunami, what tsunami?”

Maybe it’s wishful thinking, or maybe “it’s different this time”.

so fronzzz,

would you suggest that people sell into this market-get out while the gettin’s good (or bad as the case may be)??

is that what smart guys would do?

Why don’t you go to MLS, and do a search on Dist 7 and 8, with your eyes open (please!)

Somebody says they bought well below market in ’05, and we’re using that hearsay as a comp to discredit the entire index?

2727 Jackson is a TIC building with 2/1 units under $600K, recently reduced.

2040 Laguna is a 2/2 condo priced at $699K. There are quite a few other 2/2 and 2/1 D7 condos well below $900K, like 2299 Sacramento #12, 2121 Laguna #6.

Craigslist shows several 2-bedroom apartments in the area for under $3K. If you like the Presidio, here’s one that’s in the Richmond, but 2 blocks from the Presidio. I don’t see any popcorn on this ceiling:

http://sfbay.craigslist.org/sfc/apa/860055291.html

Coincidentally, while I was typing this, my house went up in value another $5K. Seriously. Wonder how I’m going to spend it?

c’mon ester, that’s too hard. how about crappy stuff in far out neighborhoods? i can find lots of falling prices on crappy stuff so its just a matter of time before d7 and 8 start to crater…

so don’t believe your own experience. just listen to ss for the ‘real deal’ on sf re

“One can simply look up MLS at those that are 2/2,2/1 that are in contract.”

Without looking at the individual property, this means very little. The better measure is to look at recent sales of property that were last purchased in Q405 to Q106 and compare the relative increase or decrease on a per square foot basis. Of course, you must first determine that there has been no significant remodeling to confirm it is a real apple.

Anyone have any Presidio/Pac Heights apples that fit the parameters?

25th ave or pac hgts…

no big difference i guess…

paco, your tone is so tame, I suspect a bit of irony there.

To answer to your question, I’d say I think it depends on your situation. Overwhelmingly I’d say it’s better for people who live in their own homes to weather the storm if you can afford the mortgage (less than 30% of net salary).

1 – If you want to stay in the place, just stay the course. Otherwise why plunk 1000s a month when your principal will decrease by a mere 5% after 10 years?

2 – Of course if you think your house will be your retirement, think again. Millions of boomers did the same and will be competing for fewer and fewer buyers (statistically speaking, and the population is growing faster at the bottom than at the top).

3 – If you were in for the easy bucks, just sell now and take your loss. There’s a chance you won’t see 2006 prices anytime soon. I hope you kept your day job…

A house is not an investment. It’s a product in which you live. The idiot salesmen that brought us to this grand national mess are not gonna help us get out of it. Apart maybe from the REO salesmen.

Dude, good try, but here are the facts:

2727 Jackson is a TIC building with 2/1 units under $600K, recently reduced.

this is 812 SQ feet, not 1300. and without parking.

2040 Laguna is a 2/2 condo priced at $699K.

This is 1020 sq feet, not 1300. Plus, it is half a block to California.

There are quite a few other 2/2 and 2/1 D7 condos well below $900K, like 2299 Sacramento #12,

I actually called the agent on this one, larger building, no back yard. More co-op like to me.

2121 Laguna #6. this one for $779K, TIC, 840 sq feet.

One advise, when you try to make a point, do your homework first.

Sorry, ester, I’ll try to keep the dog from eating my homework in the future.

On the topic of fact checking, I’m highly skeptical about your supposed purchase. Because I was in the market at that same time, and NEVER saw any deals that good in late ’05. In fact, some friends bought a unit similar to yours (roughly same size, but a 2/1 TIC) in a nearby area. MLS listed, they got into a bidding war and ended up paying roughly $800K for the place. With no parking, and it was a fixer. They thought they were lucky to “win” it at the time.

So out of curiousity, how were you able to get such a good deal?

ester –

Not to be argumentative, but you just critized Dude for what you did in the first place. You said you knew the approximate worth of your place based on some other properties that may or may not be similar to yours. Dude then points out that the argument can be made the other way. You then point out how those properties are different than your property.

If you are going to state your home has a value based on some MLS listings you should also point out how similar those listings are to your home (e.g. similar square feet, similar fixtures, similar view, similar street, similar amenities).

As you have just shown in your last post, individual properties can vary widely. You have no idea how much your place is worth until you sell it. Barring that the only way to make an accurate estimate is take all of the factors into consideration not just where a property is valued less, but also where a property is valued more.

Roger said: “What is scary was the 7% drop in the Dow yesterDAY. Most people I know just buy in live in their house and enjoy life. Not many in SF are buying b/c they want to flip. They’re buying b/c the housing stock is generally much better than the rental stock, and they just want to enjoy life.”

I don’t know how many threads I’ve posted this in, but I’m getting a bit tired of repeating myself. Roger, the reason for the nearly 30% decline in the stock market in the last year is the 10% decline in real estate!

A 10% drop in real estate is devastating. Do the math. If you own a house, how much did you put in for a down payment? 10%? In San Francisco? $1 million house? Oh, guess what, you just lost all your money.

Maybe yesterday you had $100k in the stock market? How much you have today? $93k. No big deal compared to the homeowner.

The vast majority of equity investors don’t use leverage to invest. They are in pain right now, but like the nearly 100% of recent home buyers who used very significant leverage to purchase their homes, usually upwards of 9:1 leverage.

Those people are toast. And when the next 10% comes, and they realize they now owe $100k more than their house is worth, they have a real problem on their hands.

The stock market is nothing compared to that.

take most ten year periods and measure real estate returns vs the s&p.

now look at ‘real’ sf and la real estate returns vs s&p.

i’ve been invested in both (s&p and real estate) and i know where the money has been made.

do you?

finally I have some allies who understand the difference between Russian Hill and Novato.

I also was just in the market and found only one 2br with parking in Russian Hill in the mid 600ks. And yes it’s a fractional TIC. I can’t rent it out without price control but don’t care since I live in it and will do so for years.

Over the last eight years, RE in the top tier appreciated a reasonable but not outrageous 10% given how the job market exploded and a few thousand people made massive fortunes.

Was there a bubble in Novato? Yes. What does that have to do with good Russian Hil homes that ballooned at half the rate? Nothing!

Enjoy finding your 4br in Pac Heights for 500k in 2010. Continue to throw rent money down the toilet until then.

Dude, you might be trying to be ironic, but let me try to answer it anyway – I don’t know how I got the deal, I am guessing it is partially timing. It was the week before thanksgiving, and I offered no refund on my deposit if the deal failed to close escrow for whatever reason (which was against the RE rules I was told at the time).. Got it for $623K which was the asking price. The listing agent was Brown & co.

Publius, I almost feel embarrassed that I have to answer your question. I suppose you know how people do comps: add $$ for the parking that you do not have, subtract $$ for the bigger SQ feetage….. How much do you know about RE???

Not sure if Paco’s comment was addressed to me, but yes, I do know where the money’s made:

http://www.forbes.com/lifestyle/2005/05/26/cx_sc_0527homeslide.html?thisSpeed=65000&boxes=custom

Real estate has historically tracked inflation nearly to the penny. That’s because in the end it’s just a place to live. There’s no innovation or new value being added to the economy by a new house. Equities have trounced real estate over the years, and it’s not really close.

This last 10 year period is an outlier that never happened before, and now we’re all paying the price for it.

ester –

Quite a bit acutally. In addition to being an attorney who has worked on real estate cases, I am also a real estate broker. And I did not ask a question.

You pointed out only two factors in the analysis. When using the market data approach to RE appraisals you take the current sales prices of similar properties and adjust for any differences. The key here being the “similar properties” and “adjusting for any differences.” I showed you several ways your property may be different in my previous post (just like you pointed out that Dude’s examples were different than your property).

For arguments sake I’ll provide another example. You said, “I can up with a rough guesstimates of $700K to $750K in TODAY’s market.” Have you visited any of the properties that sold for that much? What if they have a great view of the GG bridge or of alcatraz? Does your place have those views? I bet not based on the sales price of your home in Q405/Q106.

Again, the only way you can make an accurate “guestimate” is to look at properties that have two sales data points — one in Q405/Q106 and another in the last several months. After making sure they are true apples you can get an increase or decrease in value. Then control for the general area and you have some sort of accurate “guestimate.” Using square feet and parking as the only two factors will not provide anything close to accurate.

542 Laidley sold for $938k on 7/1/05 and for $950k on 6/27/08.

I saw it both times, it had not been significantly remodeled in between sales.

paco,

I hear you. I have stayed away from stocks (when you’re an individual investor, that’s probably safer) but got long rental properties from 1994 to 2003. Then prices got out of hand and I decided to liquidate starting early 2005 until late 2006. That was the best financial move of my life. I got lucky and picked both lows and highs, just following the simple rule of thumb of rent vs. buy. I bought at a ratio of 60-100 and sold everything at 250+.

Without appreciation, the rentals would have been a so-so investment even at 60. The cost of maintaining the place and interest payments ate 60% of the income even at a very low price point. Then think about places that sell for 700K but rent for 2500: you got to rationalize to the extreme to justify it as a viable investment/business. Or you just believe/hope that it will appreciate.

You gotta know when the game changes and react accordingly. I don’t want to be stuck on one tune, otherwise I’d sound like a broken record. I’ll be a bull again when the circumstances are more favorable. I hope to join you among the cheerleaders when that time comes, I love bull markets.

Thanks for the apple NVJ.

1.2% appreciation on that house. That seems consistent with the observation by some on this site that certain areas in SF are holding steady — at least for now. Any more data points for Pac Heights/Presideo?

There is an easy way to track down the SF-only figures. You can just identify data for all of the OTHER areas, then do the math. If prices are down 10% overall for 5 areas, and 4 of the 5 are flat, the remaining area is down by 50%, to use one example.

So I contacted homeowners getting ready to sell in every neighborhood in the bay area EXCEPT SF. They all said the same thing: “prices haven’t dropped at all in MY neighborhood.” They all had anecdotal evidence to “back up their claim.”

So, when I do the math, SF prices have apparently fallen by 5,632% in the last year in order to get a ten percent drop for the overall MSA.

542 Laidley somehow comes in line with the observation that the top tier is back to 2005 prices.

1.2% appreciation, compared with an instant loss due to buying/selling (think agent fees, taxes, other costs, like 10%?) and compared with another 10% inflation hit. And we’re not talking at what was the rent equivalent vs. interest payment and the opportunity costs (another 3% per year on 20% down?)

That’s an inflation-adjusted 8%+ loss + 10% expenses. Or a net 18% loss. Not a great investment.

NVJ – I believe your Noe Valley apple was a response to chuckie’s request for an apple with an initial sale within the last 3 years that shows positive appreciation? Technically it fails that test since the initial sale was 3.3 years ago, but I’m not going to argue that a few months make a huge difference (see below), and the property does show a 0.4% annual rate of appreciation.

More interestingly, this apple strengthens the argument that the CSI top-third tier is a good approximation of the “real SF” market. The Noe Valley apple is virtually unchanged from July-05 to June-08. Likewise, per Trip’s numbers, the CSI top-third tier was virtually unchanged from Mar-05 to June-08. Put another way, if you used the top-third CSI to predict the change in price for the Noe Valley apple, you’d only be off by a few months at most!

NVJ, I’ll take your word on the Laidley comp as you’ve always been very reliable on this site. So let’s modify the original challenge a bit given the CSI data — how about a straight apples-to-apples comp purchased from mid-2006 to mid-2007 that has been sold for more in the last six months?

The Laidley sale is an interesting example given the rest of this thread. CSI indicates that for the SF MSA we are back to early 2005 prices (for the top tier). Several posters have been adamant that these numbers do not accurately reflect SF, only its immediate neighbors. Yet the one concrete example that has been provided — in perhaps the strongest neighborhood in the city — shows a June 2008 sale at effectively the same price as July 2005, nearly exactly as the CSI data would indicate.

A question for people who know more about this stuff than me on 542 Laidley.

Property Shark shows two separate entires dated 7/1/2005, the $938k NVJ mentioned and a second one for $192,500 as well.

What does this mean?

Oh, and a little more info on the Laidley house:

FWIW, the place appears to have initially been listed at $1.095M in February and reduced to $998k in April before it sold for $950k.

FWIW, the place appears to have initially been listed at $1.095M in February and reduced to $998k in April before it sold for $950k.

Thanks for the info.

It’s not your typical bidding war. Maybe it was a Dutch Auction;)?

“Maybe it was a Dutch Auction?”

Come on now, I thought we had dispensed with the “rich foreigners will save SF RE” meme. 😉

Apples:

greenwich; on the front page of SS the other day. $600K more

4545 25th street: recently listed at $100K over what they bought for

Yeah, Euros are running for their lives.

http://www.bloomberg.com/apps/news?pid=20601087&sid=az1rLwgisBgg&refer=home

We’ll be able to snap up cheap European property soon if this lasts.

“Continue to throw rent money down the toilet until then.”

I will never understand this ridicuolous argument.

Why would I willingly pay a bank?

1) $150K down payment with high risk of lsing it all if i hold less than 10yrs

2) then $6000 per month

for the right to paint, remoddel the kitchen and say i’m a homeowner

When I can pay a landlord:

1) a $3800 deposit

2) $2000/ month

3) leave when i want

4) invest, save or spend the additional $150K + have an extra $4000 in my pocket every month.

Answer: I wouldn’t. Not when the comaprable mortgages are no where near rents. It is the homeowners who have bought between 2002-2008 (and who plan to hold for less than 10 yrs) who are throwing their money away.

I am stashing mine,.

trip,

when you asked,

“how about a straight apples-to-apples comp purchased from mid-2006 to mid-2007 that has been sold for more in the last six months?”

i wonder what that would prove?

selling soon after buying is a bad idea- doing so in this environment is an especially bad idea.

542 Laidley was discussed a little. A couple of quotes from f**j and Dude… very fun 🙂

“Glen Park is practically an unqualified upward market, guy. The north slope of that neighborhood has just seen a few $~3M sales. There are 25 solds, five pendings, and seven active contingent properties in the last six months VERSUS six active properties — only two of which have even been on the market for six weeks. Those two are 196 Lippard and 542 Laidley — and they are both around 800 a foot!

Ugh.

That’s it for today folks. I’m actually more than a little annoyed now and I don’t want to get mean. Just save all the baloney for your kids lunchboxes, or something.

Posted by: f**j at April 10, 2008 12:32 PM

Thanks f**j. Incidentally, 542 Laidley was reduced by $97,000 just today.

Posted by: Dude at April 10, 2008 1:43 PM”

https://socketsite.com/archives/2008/04/a_parkside_single_family_home_today_for_a_little_less_t.html

Some more info and pics on 542 Laidley:

http://california.neighborcity.com/San_Francisco/Bernal_Heights/detail/337483/542_Laidley_St_94131

Spencer, double check your math.

A unit that is renting $2000 a month, that sounds like a fix-upper type of 1/1 in Pac height, which would sell for $600Kish today.

With $150K down, your monthly payment would be $3800 a month, not $6000 that you had there.

True, it is still way cheaper to rent than buy TODAY, $2000 vs $3800. in 17 years, you would be paying more to rent than to own.

And this is assuming 0 appreciation.

At any rate, some people would always rent, and some people would always buy. In the end, thanks for those renter that I am a landlord today. Without you, this would be not a good business for me.

paco is starting to sound a lot like fl*j who anytime a soma apple showed a decline would write “for every one of these i know of ten others that appreciated” but could never provide a single example.

paco is a small time developer and he’s just talking his book.

“i wonder what that would prove?”

other than that prices are falling?

Der flujinator didn’t talk soma; and paco is correct what would selling quickly prove. Plus if any one ever gives examples they are ignored anyway.

How bout this one: 251 Arkansas

Good point regarding the rent v. buy TODAY. That is why many people that can buy today are sitting and waiting instead (until 2010?).

On a related note, someone posted a rent v. buy spreadsheet about six months ago that listed most of the issues involved in the decision. Does anyone have something similar?

paco: Presumably it would prove that you can save tens of thousands of dollars, if not more, by just waiting a year and buying in 2008 rather than 2007. Which in turn would be a very, very important piece of information for those of us currently considering buying.

Obviously past performance does not guarantee future returns, but there is no good reason to believe the downward trend will reverse itself in the next 12-24 months.

i’m looking for deals to buy-not sell.

generally, i would say that real estate prices globally are falling.

availability of credit-ditto.

my whole point is that while its easy to talk prices down its hard to find good properties to buy.

These stats don’t show the huge downdraft coming now that the tech stocks are getting crushed. Layoffs will be coming in techland late this year and early next year causing home prices in SF and the valley to crater.

gmh,

” it would prove that you can save tens of thousands of dollars, if not more, by just waiting a year”

same goes for the seller in this case. btw, i agree that prices are going down world wide.

i’m just saying that finding people that bought in ’06/07 and then sold in ’08 is not proving much beyond the fact that they are in and out too quickly.

i don’t think anyone should be in a hurry to buy right now and i’ve posted that before. BUT now is a great time to be well prepared to take advantage of the current and ongoing situation. if you are truly a potential buyer then you know what i’m saying. if you are merely a ss bear who is too smart to buy ever (“unless we get down to cs60” or some such bs) then you don’t.

I’ll agree with paco on that one. Can’t remember who, but somebody here recently posted that they bought a place in Fremont at a pretty attractive price that made buying a much better scenario than renting. So there are opportunities out there already. Just not in the 3 SF neighborhoods that many of you seem to be obsessed with. I guess I’m lucky that I don’t even want to live in 94123 or Noe – less competition for me when the dust settles.

paco,

your last posting is too funny, I know of those “ss bear who is too smart to buy ever” type of people around me.

I started looking in 2005 only because a co-worker wanted to buy. She was our SEC reporing director then, with a base of $135K. She dragged me along to every open house that she went to. Low balled a few times, never mentally ready to buy you can tell. On the flip side, I ended up buying 2. So, I guess it is a personal preference.

She is now in Japan, working for GE. Wonder if she is happy these days looking at that stats from overseas.

She was primarily looking at studio in Marina.

“A unit that is renting $2000 a month, that sounds like a fix-upper type of 1/1 in Pac height, which would sell for $600Kish today.”

Nope… 4th flr 2bdr 2ba with in unit laundry and parking 2 blks from Fillmore; 1 blk from lafayette park

low ceilings, hollow doors, yummy carpeting…

Boy the kitchen in that link chuckle gave looks mighty new, I hope I am right about 542 Laidley being a true apple. I definitely remember walking through it and giving it a thumbs down because it was too far north, into the fog belt. I don’t remember anything about the kitchen one way or another.

I know some of you can access permits filed with The City, if anyone can check when that kitchen was remodeled, it might be nice to know.

And it was hard for me to even find that very weakly positive Apple, so I think that most people’s sense that we are at 2005 prices, even in the stronger southern neighborhoods, is probably correct.

sparky-the-bear, list prices don’t really prove anything, you need an actual sale for it to be interesting.

4th flr 2bdr 2ba with in unit laundry and parking 2 blks from Fillmore; 1 blk from lafayette park

I assume this is only $2k/month because of rent control then, am I right? When did you move in?

Ester

Your story is becoming stranger and stranger and you’re starting to sound like other RE sh(r)ills.

Are you saying you are not only a homeowner based on a great deal you got two years ago but you’re also a landlord of a cash-flowing rental in SF?

Anything else about your “situation” you’d like to adjust?

“I assume this is only $2k/month because of rent control then, am I right? When did you move in?”

I moved in apr 2006 and my landlord has never raised the rent

I am not adjusting anything. the fact that one is a homeowner does not mean that he can’t be landlord at the same time.

What is strange to you??

If you say you are a human being, and then you disclose that you are also a male/female, are you adjusting your status?

Paco, I really can’t tell if we are in agreement or disagreement on this. I’m saying that prices are still falling, and will fall even further and more rapidly in coming months, so it is not a good time to buy in SF. You’re saying “it’s hard to find good properties to buy” and “I don’t think anyone should be in a hurry to buy right now.” Sure sounds like we’re saying the same thing.

So is your point of disagreement that you might buy some place at some point in the future but you think others who share our view of the market probably won’t buy anything even when prices have fallen? Ester seems to think she understands your point, but I’ve tried to discern it and just can’t.

It sounds like both “ester” and “new buyer” are both real estate agents with a lot of time on their hands since there are not many actual “new buyers” in SF any more. Any real “landlord” is more likely to “invest” in timeshares than a “TIC” (I sold my home a few years back and bought a second apartment building with the profit). As it gets harder and harder to refinance we are going to see a lot of people walking away from TIC loans and making the other TIC “investors” very unhappy…

Posted by: paco at September 30, 2008 8:57 AM:

“look for the remodelled unit that’s dark/damp and for sale after 1-2 years, maybe no parking and located in ‘real’ bernal or ‘real’ glen park-that’s where you find the price declines.”

Posted by: paco at September 30, 2008 3:16 PM:

“btw, i agree that prices are going down world wide.”

You’re starting to lose it dude.

NVjim,

List prices don’t count, I’ll remember that next time an apple comes out at a lower price. But really, I just stumbled by those places while looking at the MLS. I’m not going to reseach what has sold, those are listed a lot higher than when they last sold. Someone can keep an eye on them and we’ll find out what happens.

A good way to spot the trend is actually Zillow. No, it is not accurate regarding individual properties. However, it plots the overall trend pretty well (probably with some lagging time), especially if you look by zipcode.

The trend has been very clearly down. However, depending on the area, the slope is very different. Some neighborhoods (in SF) has been down 20%. Some are down 5%, and some are essentially flat.

That matches the CS index pretty well.

However, I don’t understand why people are so into talking about how sellers come out. The problem is, despite the price drop (probably 5% in the neighborhoods I want to live in), it is now harder and more expensive for buyers and will be even more so with the big mess at the banks.

What’s the point of cheering for cheaper prices when you cannot take advantage of it?

“List prices don’t count”

List prices are wishing prices and no, they don’t count. An apple is an unmodified property that has recently sold and can thus be compared to previous sale prices. At best your example is an apple in the making. We’ll see how it turns out.

Plenty of people in other area of the country stubbornly clung to wishing prices for quite a while. Their rallying cry? (indignanty)”I’m not going to just give it away!”

“A good way to spot the trend is actually Zillow.”

I agree. The numbers aggregated by zip code are useful for seeing the trend.

“What’s the point of cheering for cheaper prices when you cannot take advantage of it?”

I can.

The past several years were like an auction where people were allowed to show up with as much monopoly money as they wanted. God help the people who put their own hard earned money into competition with other bidders using monopoly money. If you won, you lost.

“What’s the point of cheering for cheaper prices when you cannot take advantage of it?”

Because prices will continue falling until enough people can take advantage of it – that’s economic equilibrium. Despite the fear-mongering that Paulson’s spin machine is putting out, credit is neither frozen nor thin. Plenty of it out there for many purposes. It’s just more strict/expensive than it’s been the past few years (i.e. it’s no longer free and given to everyone – lenders have factored the risk premiums back in). As prices keep falling, more and more people will have the necessary down payment and income to buy property.

diemos

The only problem is, the situation is not good for the buyers either.

If we really want to look at apples… there is no question in my mind that if you buy the same property today, it will cost more than to buy 2 years ago. That’s from the buyer’s point of view. You have to put in more down payment, the mortgage is way way higher.

And if you lost money in the stock market over the last two years (OK, I made some in 07, lost some in 08, so it is not all bad), it would be adding salt on the wound.

John, I think you are exactly right that the SF market is not that good for buyers right now. Jumbo loan rates are considerably higher (conforming loans are about the same, though, or a bit lower now). It takes a heftier down payment. It definitely would be nice to be able to buy a place with no- or low- down and free up that money for other things. But those days are gone forever (a key factor driving down SF prices as the pool of qualified buyers is now a fraction the size).

However, you’re ignoring another key factor. The SF buyer of two years ago is now down about 10% on the value of the home — that’s 100% loss of a 10% down and 50% loss of a 20% down. So a buyer today would avoid that loss. Form a total investment perspective, today’s buyer is much better off. Of course, next year’s buyer will be much better off yet.

Publius,

That was me, and you are looking for this:

http://spreadsheets.google.com/pub?key=pM4Gw0s2zSeAnOTnop5I7Lg

“You have to put in more down payment, the mortgage is way way higher.”

I thought the whole reason ALT-A resets aren’t going to be a problem in San Francisco is that mortgage rates are cheaper now than they were before. So which is it? If mortgage rates are way way higher get ready for round two of defaults which will drive prices down even more.

Ran the numbers on a $1M condo. Assuming I can buy it for 10% less by waiting but rates go up by 2% while I’m waiting I will have to hold for at least 16 years for it to be a better decision to buy today. That assumes I can’t refinance at a lower rate at anytime during those 16 years.

My portfolio was up in ’07 and so far is up in ’08. My down payment isn’t earning a lot but is safe. I like my odds.

“What’s the point of cheering for cheaper prices when you cannot take advantage of it?”

CASH

Some posters on this site, I have noticed, have the belief that the people on here can either “talk up” or “talk down” the prices.

I can see how that can work in the stock market. A few people piling on to buy or sell the shares of a company, especially a thinly traded one, can possibly do that.

I can also see how discussing a particular listing can help or hurt it.

But doing that to the real estate of a city like San Francisco? A blog like Socketsite?

Let’s be real, few in SF buy for short term.

My point is, someone who is not over extending, who can easily qualify for mortgage (no Alt-A, subprime crap), could get 5% mortgage rate 2 years ago. Now, it is more like 6%+ with 25% down.

I have been looking, and I am going to tell you that I can afford less house than 2 years ago. And if you were looking, you know that’s true.

I am the one who has been telling people cheap loans still can be had…however, even Penfed is asking for 25% down, and who knows with the credit squeeze what will happen. In comparison, it was easy to get 30-year fixed for under 5% 2 years ago.

And SFSal, read my posts carefully. I am not talking about people who bought. I am talking about people who want to buy, good credit, good income, it costs more to buy right now. I don’t care a bit how others are doing.

“I have been looking, and I am going to tell you that I can afford less house than 2 years ago. And if you were looking, you know that’s true.”

I don’t doubt you amigo. It’s amazing what you can “afford” when the bank gives you a loan you have no hope of every paying off and won’t be able to make the payments on after the teaser rate period.

If the bank gave me a zero-down interest-only loan with an initial teaser rate of 0.0000000001% for the first five years then I would easily be able to “afford” a $1T dollar property. At least for the first 5 years. Then I wouldn’t be able to afford it and I would default. Then the MBS that my loan was put into would lose money. Then the financial institution that held the MBS would go insolvent. Then the government would go into a panic throwing taxpayer money at the financial system.

By 2004 it was both obvious and inevitable exactly how this was going to play out. It’s like watching a damn Kabuki play. I’m reminded of Santayana’s corollary, “The only thing we learn from studying history is that we never learn anything from studying history.”

short prediction –

sf prices wil decline 10% over the next year.

reasons:

home eq and stocks are way down for almost everyone — say 25% for each

mortgage reqs are tightening fast and when they stabilile in a few months prime borrowers loan amts will be at least 10% lower then they were PRE meltdown (not even counting now).

prime rates will be at least 50 bps higher once banking industry is concentrated down to a very few players.

you have to really, really like something to buy now, whatever block it is on, because you can buy it less in 6 mos.

its gonna be different ; forget abt the broker talk.

John,

No question you are correct in all your observations. The whole point is that easy credit lead to unprecedented rise in prices. The converse also has proven to be true nationwide and in a lot of the 9 county bay area.

What remains to be seen is if real sf (d4,5,6,7,8) has immunity. I will note that real sf has been shrinking over the last year or so and d1,2,3,9 & 10 have seceded not too long ago.

Patelco is still offering 30 year fixed Jumbos for 6 3/8:

http://www.patelco.com/rates/fixed_rates.aspx

You need 20% down, but Patelco has always insisted on this.

I didn’t know that 30 year fixed rates ever got below 5%, but I wouldn’t be surprised if someone got one. For 0 points? That is a great deal.

Note that even if prices have “only” fallen by 10%, buyers also now have the luxury of full inspection and financing contingencies. That is something they did not have last year and it has value. If there is 50K in foundation damage, you no longer have to close. Last year you did.

Also, the stuff that you are seeing for only a slight discount is the stuff that is in tip top shape and location. The realtors are telling the sellers not to bother listing homes that have big problems or need a lot of updating or other work, though some are still making it to the market.

Two years ago, you had all sorts of crap hitting the market and all of it sold quickly. That stuff is rarely being listed any longer. When it is listed, it’s basically hitting 3% per year over 2004 or 2005 prices. That’s up from 2004-2005, though not by much, and WAY DOWN from 2006 and 2007.

Also note that the patelco rate is only for loan amounts up to 1M. On a 2.5M loan, you “merely” have to put $1,500,000.00 down. So they are hardly going much above the conforming limit and then you have to take up the slack.

Somebody was asking about purchases in 2006/2007 and sold in the last 6 months.

I’d say look at the 188 Minna condos for some large increases, though there have only been a handful of sales there in the past 6 months, and prices are definitely going down some very recently. However, the purchase price may be hard/impossible to find online, since these were builder sales…

Anyway, not universally representative, but a data point.

John wrote:

> Let’s be real, few in SF buy for short term.

John must hang out at the PU Club since that is one of the few places in SF where most of the people are long term SF residents. Most other places in the city I will bet that half the people in the room moved here after Art Agnos was mayor…

SFSal wrote:

> I thought the whole reason ALT-A resets

> aren’t going to be a problem in San

> Francisco is that mortgage rates are

> cheaper now than they were before.

The problems with many ALT-A loans will start when the IO period ends. A million dollar loan at 6% IO is $5,000 a month. A million dollar loan at 6%/30yr/am is $5,996 a month. The big problems are when the “pick a payment” loans (the loans that took out Wachovia) reset since over 80% have had neg. am. (and loan balances of more than the day of origination)…

PresidioHtsRenter,

On SS, once I used the 7-year duration (which is the average # of years held by owners in whole US) for some math, and someone else showed us the data showing that average SF owner stay for 10 years.

You can also use math – there are about 700K to 800K SF residents, so about 250K households. 30% are owners, so there are about 75K inventory. If average owner held 10 years, that means about 10% of that exchange hands every year – 7500 units.

That is about what we see from the sales data – 600 units per months (2008 has been even lower).

Another way to look at it – go to PropertyShark.com and get a free account. Search for a property in the neighborhood you are interested in. Go to the map section, and one of the map shows you when was the last sale of each unit in the neighborhood. You will see in most neighborhoods, new owners are few and far in between.

And I consider 10 year to be long term – not 2 to 3 years which SS likes to highlight.

If you ex out every district and property that’s lower, real estate is up! You can’t lose!

Ok, I’m just poking fun and that logic can be used both ways. Best comment on this thread so far is Dude’s “wallpaper made of whale leather” !

another rent/buy calculator for publius:

the NewYorkTimes version:

http://www.nytimes.com/buyrent

(don’t know how to activate this shortcut link)

[Editor’s Note: To Rent Or To Buy, That Is The Question (That Only You Can Answer).]

I appreciate Chuckie’s comment yesterday (6:15PM) regarding “talking” RE up or down. A lot of emotional reactions here IMO can be traced to people thinking they are on a team, bulls vs. bears, and that the volume and quality of one side or the other will somehow influence the market.

I just want to know when and where to buy… I know I will eventually. In the meantime I appreciate everyone who posts on here with concrete information and analysis.

Talking “RE” up or down?

I wish we could talk mortgage rate up or down.

Thanks fundy and missionite (and SS).

In the last two weeks, 30 single family homes in San Francisco sold above asking and 30 below asking. 6 sold at asking.

Condos: 18 over, 33 under, 12 at.

TICs are hard to track due to many developers only list one or two of the 3 or more properties in a complex in MLS. I just don’t trust MLS for TIC stats.

Po Hill

PresidioHeightsRenter,

First of all, I’m not a real estate agent. I’m a small business owner.

Also, stop acting like TIC’s are owned by a group of neighbors who share a mortgage. This is no longer what TIC’s are about.

TIC’s are now fractionally owned. If my neighbor goes bankrupt, it does not touch my loan or credit prospects. The ONLY difference between a condo and TIC for the most part is that rent control applies to a TIC.

NewBuyer if you have one of the (rare) individual TIC loans you will still be on the hook for the property taxes if one of the other TIC owners walks away. If you can’t convert to a condo it is going to be very hard (if not impossible) to get an individual TIC loan in the future.

yo renter,

“If you can’t convert to a condo it is going to be very hard (if not impossible) to get an individual TIC loan in the future.”

why do you say this? do you have any idea what you are talking about? your ignorance vs. the facts….hmmm, i think i’ll go with the facts.

So, paco, what are the facts? Why is he “ignorant”?

What happened to all the talk about the convergence of the lines indicating the bottom? Seems like that misguided notion has not been brought up.

the fact is TIC loans are getting more and more commen these days, and the gap between a tic or a regular loan has shrinked big time in the last 12-15 month.

I know these first hand, because I have a tic loan, have been approached to refinance my loan from 7.5% to 6.5% about 3 months ago.

And I don’t worry about a past due tax by a co-owner since the balance will be paid off from the proceeds of the property.

I was actually in a situation whereby a condo owner fell behind on HOA for 2 years, and that balance is paid off when I purchased the unit.

newbuyer,

Agreed 100%, the only material difference is the rent control on rental $$ increase.

smaller difference such like having to maintain a spreadsheet among the owners to calculate the tax since it came in one bill. Inconvenient there.

Treeman,

That was my concept. Now the bailout bill passed, I will stick to my theory.

And if it is a real bottom, we won’t see it concretely on CS graph until at least 3 to 6 months from now, simply because the way the graph is plotted.

Buy, buy, buy!!! You heard it here first, we hit the bottom – just won’t see it on a graph for a while.

Anyone who buys right now needs to have their head examined. Seriously.

“4545 25th street: recently listed at $100K over what they bought for

Posted by: sparky-the-bear at September 30, 2008 1:53 PM”

Now reduced by $200K, and lower than purchase price in 2007. After commission and transfer tax, the owners are looking at a loss of at least $200K on their Noe “investment”. Feel the burn.

http://www.redfin.com/CA/San-Francisco/4545-25th-St-94114/home/1397566

“4545 25th street: recently listed at $100K over what they bought for

Posted by: sparky-the-bear at September 30, 2008 1:53 PM”

“Feel the burn.”

I feel a bidding war starting in Noe.

Yeah but “list prices don’t really prove anything”, you can’t beat me up both ways. I already conceded that the contract price is the “apple”. I only brought it up because I came accross it on the MLS and know the developer and so I knew no work had been done.

Plus, I couldn’t care less what they sell for.

Is the demand for $3M Noe beefed-up mansions down? With Google still under 400, this could help validate dub dub’s Google lazy indicator.

@ spencer, who said on Sept 30th “Anyway, why would anyone buy a 2bd2ba TIC enar the presidio when you can rent a 3bdr house in the presidio for $3000?”

It’s because monktards like you trying to rent for $3000 in presidio will remain broke at the end of 10 years, whereas the person who buys a 2bd2ba TIC near the presidio will be sitting on fat equity when this blows over…

Go Figure ! Wait, before that, get your head out and unstuck from where the sun don’t shine !