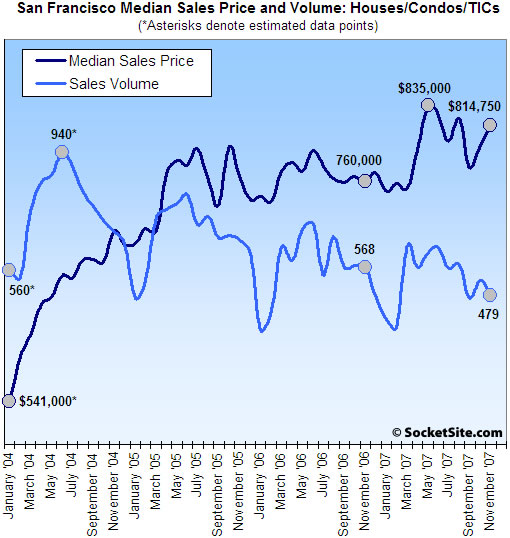

According to DataQuick, sales volume (i.e., demand last month) for existing homes in San Francisco fell 15.7% on a year-over-year basis last month (479 sales in November ’07 versus a revised 568 sales in November ’06) and fell 8.9% compared to the month prior (526 recorded sales in October ‘07). As we noted last month, it appears as though October’s uptick in reported sales activity was at least partially driven by a delay in September closings rather than a much ballyhooed rebound in buyer activity.

At the same time, the median sales price in November was $814,750, up 7.2% compared to a revised November ’06 ($760,000) and up 2.5% compared to the month prior. And yes, for some strange reason we’re still thinking mix.

For the greater Bay Area, sales volume in November was down 36.2% on a year-over-year basis and fell 6.5% from the month prior (5,127 recorded sales in November ’07 versus a revised 8,042 in November ’06 and 5,486 this past October). The recorded median sales price fell a nominal 0.3% as compared to the month prior but was up 1.5% on a revised year-over-year basis.

At the extreme, Solano County recorded a 50.2% year-over-year reduction in sales volume (and a drop of 14.8% in median sales price) while Contra Costa County recorded a 46.0% year-over-year drop in sales and a 6.9% drop in median sales price despite a reported 1.3% growth in population from July 2006 to July 2007.

∙ Bay Area home sales stuck at two-decade low; price picture mixed [DQNews]

∙ San Francisco’s Sales Volume Up And Down In October [SocketSite]

∙ Listed San Francisco Home Sales Volume Down/Down In November [SocketSite]

∙ JustQuotes: CA DOF Estimates Population Growth In San Francisco [SocketSite]

The median price (half above, half below) is a nearly useless measure. Relatively few higher end homes sales shift the median price upward. Average home price is a much more useful measure, one that gives some idea of how the entire pot is boiling.

Hmmm, I wonder where DQ gets its numbers. The November sales figures I see show 178 SFRs and 230 condos/TICs = 408 total. See:

http://www.rereport.com/sf/

Altos research shows 501 SFRs and 831 condos/TICs on the market at December 9. So inventory has crept up to 2.87 months worth if you believe DQs numbers and 3.26 months if you believe other sources. Not Miami, but continuing the move in a bearish direction.

Average isn’t any better, MCM. A single sale of a $20m mansion ruins the average. Median doesn’t have that problem.

Really, you want to see median and average together. Or maybe just a histogram 🙂

Looks like there were 408 reported listed sales as Trip points out (178 SFH + 230 condos). Does this imply there were an additional 71 sales (unlisted new construction, etc)? Where does DQ get this data? Current active listings are “only” 968 (480 SFH + 488 condos). I understand the impact of mix and it would be great to see the data on a district basis – but, if prices are indeed dropping, one of these months we should see a clear YOY decline for all metrics.

Cracks me up how if prices rise, it’s the mix. If prices fall, it’s not mix. Whatever!

If the mix in fact changed to a new paradigm six months ago, then we have the same mix as a six months ago. It’s not like each month’s sales alternate between McMansions and crackhomes.

No matter what kind of curved trendline one wants to employ, the trend is obviously upwardly-shaped though flattening after May-05.

anon, medians ARE down from six months ago.

“As we noted last month, it appears as though October’s uptick in reported sales activity was at least partially driven by a delay in September closings rather than a much ballyhooed rebound in buyer activity.”

Yeah. A bear would deduce that.

Or, conversely, a bull would say that October’s uptick was a reversion to norm as there was far less out and out panic in September than there was starting the second week of August. A bull could also look at this new data and posit that November’s data also was more in keeping with traditional buyer slow-down patterns.

The outlying counties are starting to really get hammered now. Sonoma County’s median is back to $500,000 for the first time since May 2004. Look at Solano and even CoCo.

Will San Francisco be an island among the chaos? I doubt it.

The outlying counties have been getting hammered for some time now, particularly Sonoma. SF, much of Marin, parts of San Mateo, and parts of Alameda and Santa Clara have been the “islands” for closer to two years than one year at this point.

I heard the DQ guy on radio (AM 740) at about 1:30PM today.

The amazing thing is, the percentage of jumbo loan dropped like a rock YOY from over 60% to 44%. Yet, the median price increased.

What does it mean? To me, it means a lot of people have money. They had money for larger down payment, but chose to take bigger loan instead (why would not? with the mortgage rate at below 6% last year). Now it is harder to get jumbo loans, so they put up higher down payment.

Another interesting thing is the radio news lady was grilling the DQ guy on whether the price will crash. The DQ guy pretty much avoided the question and said “the bay area RE has always been and will always be experience.”

On the other hand, Sonoma took a big hit (12% down?). If anyone wants to get into the wine business, it might be a good time….although I think there is still room for another 12% down.

Regarding the mix of Jumbo loans, people could also have found it economical in the current climate to combine a conforming $417k loan with some other type of non-jumbo loan (HELOC) to make up the total purchase price, rather than just take out a Jumbo loan…. I read that some mortgage brokers were using this technique to finance house purchases in SF.

John – the use of jumbos is falling but I don’t think you’re drawing the right conclusion. I have friends that had to shift from a single jumbo to a conforming plus a second when the credit markets tightened in August and according to their mortgage broker lots of others were being forced to do the same. It’s not that they have so much money they don’t need the jumbo it’s that they don’t have enough money to qualify for the jumbo any more.

I guess I’m doomed to be that guy that constantly explains the definition of median over and over and over again.

MCM, “a few higher end homes” don’t do anything to the median. That’s the whole point of a median in the first place. The top 2% has ZERO impact on the median. Zilch. Nada. They could sell for $10 billion dollars each and the median wouldn’t budge a penny. What *will* make the median shift upward is if the lower end homes stop selling completely. This has the effect of moving the middle upwards. And that is exactly what is happening in lower end neighborhoods like the Excelsior, Bayview, etc. The sales volume for lower end homes has dropped like a rock, and the result is medians are rising. If lower end homes stop selling completely it’s completely possible, indeed likely, that the prices can drop for every single home in San Francisco, even the upper end, and the median will still rise upwards. It’s quite perverse, isn’t it?

This is the problem with using Median. A better way to measure prices in SF would be to sample all homes with no remodeling between the two most recent sales. If you can sample enough homes the price difference plotted out over time should give you some indication of what real prices are doing in any given neighborhood. The problem of course, is that most homes have some remodeling done at some point, particularly over the last five years (one of the reasons Home Depot has grown so spectacularly), which makes it very difficult to remove as a factor.

Here’s a blog post on using the median for real estate prices, for those that care:

http://submedian.blogspot.com/2007/11/what-hell-is-median-and-why-should-i.html

Within the next year or so, you will see that this nonsense about median/average or $/sq. ft. will become all academic…..

The data is nonreliable, and it is dirty. It is the nature of real estate data. You will never be able to draw sensible conclusions from price data, and I think that is purposeful by the REIC.

Not to be so pompous, but none of the discussion is really on the mark.

The fundamental problems with the data relate primarily to: (1) price data is not adjusted for renovations and upgrades, which can be very substantial in bubbles as people foolishly allocate capital to consumption items like homes; and (2) the $/sq. ft historical measures do not reflect the rampant addition of square footage in these remodels (or earlier renovations) because they key off the historical tax data. Ever approach a realtor at an open house and ask, “Hey, this house is really big (like 3000 square feet)” And the realtor looks at you and says, well “1800 square feet according to the tax records” and give you that blank smile. Maybe james can explain to us how the true $/sq ft is reported (that is, the measure adjusted for the addition). Hint, it isn’t.

Other time-series data distortions include: (1) survivorship biases; and (2) adverse deselection, because owners are reluctant to “take a loss”. I’ll leave it to one of the realtors on this blog to explain these, because I am sure they have thought a lot about them…..

In the end, it’s hard to decipher what any of this data means… it’s got a lot of “noise” and there really aren’t that many data points given the size of San Francisco (much of it due to the opacity of the market)

Bears can extrapolate what they feel from the data, and Bulls extrapolate the exact opposite.

I like to take a step back and look over longer time horizons… it smoothes out some of the noise

What is clear, is that sales volume is down substantially from its peak of 940 in June of ’04, but then has oscillated significantly since then, with each peak failing to go as high as the previous peak. (there are 4 waves… each successive wave has a lower peak, but the trough is about similar)

as for price, there is obvious RAPID appreciation early on in the graph (Jan 04 to May 05) and then it slowed considerably into an oscillation with the second to last reading popping quite high.

what does this mean? Who can say?

I will not “see” anything significant until I see an increase in inventory combined with decreased or flat sales (which signals that sellers are forced to put or keep their homes on the market but buyers are not biting). this has been the harbinger for all of the bubble markets that I’ve watched implode.

They tend to start with sky high sales prices (median, average, etc) and low inventory, then sky high sales prices and high inventory, then plateauing sales prices and higher inventory, and then slowly falling sales prices.

SF still has respectable sales, and LOW inventory. no crash yet.

but as I’ve said, it will take YEARRRSSSSS to play out. it’s like watching the paint dry of a painting of grass growing.

Fluj: This has nothing to do with being a bull nor a bear.

In 2004 sales volume increased -5.7% from September to October

In 2005 sales volume increased 0.8% from September to October

In 2006 sales volume increased 1.1% from September to October

In 2007 sales volume increased 12.2% from September to October

In 2004 sales volume Decreased 5.2% from October to November

In 2005 sales volume Decreased 1.8% from October to November

In 2006 sales volume Decreased 0.9% from October to November

In 2007 sales volume Decreased 8.9% from October to November

The trend into and out of October 2007 simply doesn’t look all that traditional (nor normal) to us (at least not relative to the past four years).

There are two obvious reasons why sales volume is dropping significantly: (1) there has been a serious shift in mindset and would-be buyers now realize that prices are likely to be anywhere from a little to a lot lower in the not-so-distant future; and (2) financing is now unavailable for a huge segment of the population — everyone but those with stellar credit and a very large down payment, which is an even bigger paradigm shift that #1 given the lax lending standards that lasted up until about August ’07.

Thus, demand is clearly much, much lower than just a few months ago. Of course, prices are determined at the intersection of supply and demand, and time will tell if supply falls to match the now lower demand or if owners will refuse to sell. The MLS data appear to indicate that demand is dropping much faster than supply.

Prices are up! Clearly, there’s no bubble.

Pay no attention to the man behind the curtain…

Trip,

“and time will tell if supply falls to match the now lower demand or if owners will refuse to sell

About the idea”

Just a few data points. Check out the anecdotal info I provided at the end of the “Satchel Does Deflation” post for some indications of pent-up supply in my immediate area.

Key paragraph in the DQ News article, “The number of homes purchased with conforming loans (up to $417,000) fell 12 percent in November compared with a year ago, while jumbo-loan purchases fell 58 percent from last year. ”

Which means there were relatively more low end homes sell compared to high end homes, which means the +7.2% YoY could actually be understated.

Loola, those data just indicate that relatively more homes were sold using conforming mortgages, not that more high end homes were in the mix.

Exactly, there were less high end homes in the mix, and the median prices still went up 7.2%, which means prices probably went up even more than the 7.2%.

With mortgages harder to get, looks like more cash downpayments. I think ironically, there’s a been a couple years of building pent up demand, which makes me nervous that i can’t buy a home in 2008, b/c the fed is cutting rates and bonuses are pretty large this year.

Loola, realtors ™ love people like you. I think you’re missing Trip’s point, btw.

No, that’s not right. I could buy a $10m property with a conforming loan if I put up $9.6m as my downpayment. Conforming loan volume definitively tells you nothing about the mix…

Socketsite, how can you look at these figures and draw exact meaning? You see what you see, my man. And you see it that way because you are sort of bearish. I can look at these same numbers and spin them a different way.

In 2004 sales volume increased -5.7% from September to October

In 2005 sales volume increased 0.8% from September to October

In 2006 sales volume increased 1.1% from September to October

In 2007 sales volume increased 12.2% from September to October

In 2004 sales volume Decreased 5.2% from October to November

In 2005 sales volume Decreased 1.8% from October to November

In 2006 sales volume Decreased 0.9% from October to November

In 2007 sales volume Decreased 8.9% from October to November

I can say that October traditionally starts the slowdown late year. I can say that 2005 and 2006 are anomaly years, with brisk activity year round and little month to month variance. I can say that August 2007 saw a very real scare. And I can say that August 2004 saw the emergence of a bull market.

It’s all in your own personal prism. I found it telling that you drew a bearish conclusion.

I don’t get it, you’re saying that a 7.2% rise in median prices in the middle of a massive credit crunch, while homes purchased with jumbo loans are down 58% is NOT meaningful and telling that prices could actually be indeed up even more in SF?

Is it not telling that with such a massive credit crunch, it sure seems like people have lots of cash and are just putting MORE money down? How is that a bad sign? That tells me balance sheets are very healthy.

I really don’t get the denial. There are so many examples of prices in SF 5-10% higher than comps from last year, and 20-30% higher than comps from 2 years ago.

Oh burn!! Loola got you on that one. Sure you could buy a 10 million dollar house with 9.6 down and a conforming loan but nobody does. I’m going to have to call bullshit on this data meaning that prices didn’t go up. I was looking in October 2006 and prices were lower… prices are now higher in 2007, and the graph illustrates it, and the sales illustrate it, and the places availible are even more of a rip off.

What they do next? Who knows. I hope they go down… to the point where buying is competetive to renting…till then I’m still out of the market. But pretending prices aren’t up in San Fran over the last year is denying the obvious.

Loola–its basic statistics. The bad neighborhoods get hit first since much were subprime financed and there are no subprime loans. Therefore the median prices go up and volume goes way down. Like it has. Also to Fluj–you run the numbers against the same month of the prior year. Your analysis is not statistically valid. You can either try and deny the market is collapsing or you can get ahead of it by either selling now if you need to or getting or preparing for it professionally if you are a realtor and want to stay in the field.

I don’t know how many times I’ve said it, but I’ll say it again. Realtors do not need bull markets in order ot make a living.

Why does one run the numbers against the same month of a prior year? Clearly fall 2006 was a different market entirely than fall 2007.

I just want to know. How many of you doom and gloomers will come on here and admit error if you’re wrong. Satchel said he would. Cooper, you just said “the market is collapsing.” come on now. That’s the type of hyperbole that’s creating consternation for real buyers in the marketplace, every day. The market is not collapsing in San Francisco.

Some of you guys need to get off this “Everyone is already getting creamed” shpiel, for real. It’s embarassing.

fluj,

You know I’ll admit that I am wrong! Show me the quote – I forgot it but I remember saying something like I would buy a bubble property in Marin if something happened – but I forgot what the something was. LOL!

But I’m not…. Real estate is a long-term thing. I’ve given you guys a lot of information about debt versus wealth, but it’s clear not many understand how it works. Oh well….

A deflation is being engineered. The Fed wants it. I know you probably haven’t ever really thought about the concepts I brought up, but you just might want to try.

Take a look at this chart:

http://research.stlouisfed.org/publications/usfd/page3.pdf

I know you are not a macro guy, but trust me, this is the only way the fed inflates. Now, tell me, why is the Fed shrinking base money when there is a credit crunch on? And why is the government so keen on keeping the homedebtors in their homes?

I’ve given you guys all a lot of hints to think about, but I guess I’m viewed as a crank.

Do look at the chart, and if anyone has an answer, I’d love to hear it.

About “inflation”, aren’t high oil prices **deflationary**? I mean, if the poor little American Debt Serf has to pay more for gas, and for food, and he still has to pay for his debts, doesn’t that leave LESS money for him to pay for other things? Wouldn’t that make all the other prices go down? Hmmmm.

I’ve said it. Inflation is not price change, although most people think of it that way. Inflation is inflation of the money supply, which is credit. Credit is contracting. The monetary base is contracting. Some prices are going up (namely oil and food) because of real demand for those commodities. That leaves less money for other things, like, ummmm, say real estate. But aggregate prices go down, because credit is going down.

So far, every time I ask a question, no one gives me any sensible answers. No one. How can the fed engineer general inflation? Give me the mechanism specifically. Perhaps I can learn something. Another question, if prices of certain things we need are rising, and credit is contracting, doesn’t that mean there is less money/credit to buy other stuff? And lastly, some of you are stretching to buy $1.0MM+ when you earn relatively low salaries of $200K or so. Doesn’t it worry you at all that there is a whole world of thought on credit/money supply that you may not be aware of – that you might want to understand before making such a HUGE commitment to service that sort of debt? Remember how it’s done – how the central bank takes the wealth of the citizens in order to assure solvency of the government and profit for the fed: “first by inflation, then by deflation.”

And I’m still waiting for james’ investment strategy for growing his wealth. I laid out mine in a minute after his challenge. I’m still waiting…

I think it is unlikely that a 15.7% sales volume decrease distorted the median enough to account for all the 7.2% median price increase. Whether or not it did, it is clear that prices in SF have been holding up quite well, despite the drop in sales volume.

It’s certainly possible that we are heading for an economic calamity of unprecedented scope, but we have not yet reverted to hunter-gatherers, and I doubt this will happen anytime soon.

One compares year over year because of seasonality. Different months are seasonally more active or less active than others. Back to school etc. One does not need to be hyperbolic to describe what’s going on. Rather, I’d say the people that though 100% returns in just a few years on real estate was normal are the ones that need a reality check. If anyone should be embarassed its those that did not see this coming or even worse those live in denial.

And some realtors can survive well–I chose my words carefully. But all those that entered the profession in the boom times will not all continue to do well and many will have to find something else to do.

Also. All these people are talking about programs to send checks to home owners to help them out–even Alan Greenspan suggested thi. Hey how about we just let the prices continue to fall back to a normal level. That long term is better for the market overall. The faster that happens, the sooner this crisis will be behind us.

“Some prices are going up (namely oil and food) because of real demand for those commodities. ”

actually, while crude inventories fell 7.6mm barrels this past week due to storms around the gulf coast, inventories in cushing,ok rose again for the fifth straight week, and gasoline stocks were up 3mm barrels. high oil prices are being driven purely by speculators and peak oil hysteria. even the head of exxon believes prices shouldn’t be above the 60’s given the supply situation.

if you believe in deflation and slowing US growth, there’s no justifiable reason for higher oil prices, considering our demand should be falling and we represent 25% of the world oil consumption. and you certainly don’t seem to believe the the US economy has decoupled from other world economies which would further erode the demand picture.

“I know you probably haven’t ever really thought about the concepts I brought up, but you just might want to try…. I’ve given you guys all a lot of hints to think about, but I guess I’m viewed as a crank…. So far, every time I ask a question, no one gives me any sensible answers. No one. How can the fed engineer general inflation? Give me the mechanism specifically. Perhaps I can learn something…. some of you are stretching to buy $1.0MM+ when you earn relatively low salaries of $200K or so. Doesn’t it worry you at all that there is a whole world of thought on credit/money supply that you may not be aware of – that you might want to understand before making such a HUGE commitment to service that sort of debt?”

Whew. What condescension.

So you took Ec 10. Big deal. I haven’t heard such bloviage since sophomore year when the self-designated contrarian conservative in the entryway would drone on trying to teach us all about the Laffer curve (yes, I know, you’re not a Keynsian — this is just an example of similar behavior from another wank).

Some of us are native to the West and have seen its cycles over many years. We don’t appreciate condescending lectures from Johnny-come-latelies (by the way, why move here if you hate it so? It’s a lot easier to keep market hours on the other coast). We have plenty of capital and understand macroeconomics also, at least at your level. We get it; we saw this coming. That doesn’t mean we are bound to answer your Socratic questions in the comments of somebody else’s blog.

I’m tired of wading through your self-aggrandizing lectures to the “little people” here. If you stopped moderating the comments and let an actual dialog take place, you might indeed learn something from people who agree with you on many points but are utterly put off by your grandstanding.

just because the fed is deflating the money supply (which they definitely are, i agree) doesn’t mean that the value of all goods is going to drop or drop evenly. there might even be price increases in certain goods and services depending on demand. not all assets are going to drop in some lock-step fashion as you seem to suggest.

there are certain assets whose prices rose strictly due to the availability of funds and are not supported by any fundamentals. real estate in the outer bay area comes to mind. as the money supply shrinks, asset prices will fall and are falling. it never made sense that someone should pay 600-800k to live 35 miles outside san francisco on a tiny lot crammed up to their neighbors. the bay area is the only city i can think of over the last 5 years where it got more expensive to move out of the city. i can move 8 miles into new jersey and get a place for the fraction of what it would cost in manhattan. granted, that means you live in jersey, but that’s beside the point.

also, you’ll see the same thing between neighborhoods in san francisco. it doesn’t make sense that living in the crossfire in bayview only got a 20% discount on price, or living in the fog in saint francis wood would be as expensive as presidio heights. rationality should return there.

satchel checker,

Please, no sniping. I was being sort of general, I admit. One week inventory drop is not a powerful trend of course, and you can assure yoursef I am all over Cushing, OK. You might also know about all the oil in barges off certain northern European cities. Hmmm. Maybe YOU can tell us which cities, and who is funding those transshipments??

There is a lot going on. It’s mot being “driven purely by speculators and peak oil hystoeria”, of course, but that’s part of it. There is a real demand component (a malinvesting China can generate a lot of import demand growing at something like 12% don’t you think?), a currency translation effect, likely a war premium, and God knows what else. Is that more clear?

Now, on to my substantive point. Can YOU explain how the Fed intends to engineer inflation? Can you give me the SPECIFIC mechanism for injecting the cash? Or is it some other method?

Can YOU explain why the monteary base is contracting, while the Fed is cutting rates?

Can YOU provide a plausible explanation for why the 10Y is at 4%?

Can YOU reconcile why the Deflator for 3Q GDP printed at something like 0.8% annualized, while CPI is running at 4%++ annualized?

And, hmmm. Can YOU tell me why the Fed uses something like 20 different measures of price inflation? Median, CPI, Core, Chain-weighted, PCE, Deflator? Who knows what else… Which is YOUR preferred measure?

Satchel checker, I thought I was magnanimous in not calling attention to your last snipe about SF being the only city to bust and then boom (basically your point). I figured you were a victim of some pulic school system, which spent more time on “justice” than real history. Hmmmm. LA in the late 19th century comes to mind – I think you’ll find that the city contracted by 50% following a similar land bubble (yes, they were even saying the same stupid things that you’ll hear every day today like they’re not making anymore land! and every other cliche as well). Maybe Chicago and something about a Great Fire? Hmmm. Miami in the mid-1920s – a maniacal real estate bubble and collossal bust, and yes, all the stupid stuff you hear in SF today. Exactly the same stuff, including the idea that all the wealthy were going to go there, no more land, LOL! All you had to do was drain the swamps, but the fools fell all over themselves buying it wgile it was still wet! I also sort of remember a string of burning cities in the South, and someone named Sherman. Yeah, who was that guy. Something about Greycoats, or was it that drunk general, hmmmm…. And, of course, don’t forget the Great Lakes cities, first queens of the prairies when agriculture was king, then to bust in the dustbowl, then to boom in the ramp up in WWII production, ahhh….only to bust again (at least some) in the great transformation to the FIRE economy (Financials, Insurance, Real Estate – but I’m sure you knew that…).. And don’t forget the Mack Daddy of all boom/bust, NYC. I’ll let you sketch the cycles there if you like.

Please, a little professional courtesy, and no sniping. Let’s have fun with this! And if you do have any answers for me I am sincerely yearning to learn. I have a good deal of capital invested in my view.

sigh,

“Whew. What condescension.”

That’s fair. Apologies to the board! 🙂

I just meant that even at $200K, you’re talking 5X income for a modest condo here, which seems crazy. Sorry if that came out wrong.

And ps, I never took any econ classes. 🙂

Satchel, as someone who is designs and builds large custom residences, what I cannot understand is what I am seeing in certain areas like Santa Barbara/Monteceito and down in Newport Beach/Laguna Beach. Newport is still selling homes above 7 million at a very rapid pace and when would these type of places eventually slow down? (It is not public record yet, but Nicholas Cage just sold his house in Newport for over 26 million) We finished a project in Calistoga recently that sold above 7 million before the paint was dry.

Good luck on trying to convince some that it is not as “unique” here as they want to believe. Our Bay Area economy is not nearly as diverse as urban regions such as L.A., NYC or Chicago, and as attractive as San Francisco is, it is not nearly the wealth magnate that we want to believe. The number of sales in the upper bracket is still small compared to some other areas even in California, and I see most of our clients wanting to build outside urban regions in places like The Stock Farm in Montana, and Bighorn CC down in Palm Desert, Kukio and Hualalai, and gated canyons around Napa Valley. More and more of our clients are choosing to have condos in the 1 to 2 million dollar range in the city, and their primary residences worth many times more, out in more remote resort areas.

“Please, no sniping.”

no intent to snipe, but you are throwing around stats to shut people down, and some of them are overblown or simply incorrect.

“I was being sort of general, I admit. One week inventory drop is not a powerful trend of course, and you can assure yoursef I am all over Cushing, OK. You might also know about all the oil in barges off certain northern European cities. Hmmm. Maybe YOU can tell us which cities, and who is funding those transshipments??”

Sure, just follow Oil Movements. it’s not like you have to have your own gps transmitters on those tankers.

“There is a real demand component (a malinvesting China can generate a lot of import demand growing at something like 12% don’t you think?), a currency translation effect, likely a war premium, and God knows what else. Is that more clear?”

your argument is circular. if something doesn’t comport with your worldview, then it’s malinvestment. it’s impossible to prove or disprove your point. however, if the chinese economy is directly and inextricably tied to the US consumer, their demand for oil will move up and down with US growth. consumption is a very small component of the chinese economy.

and i don’t argue that the fed is engineering inflation. that’s someone else. i believe there is deflation right now. my point is that there’s no reason for that to have an even effect across the market.

also, i don’t believe san francisco is the only city to never bust. hello gold rush? however boom-bust cycles are driven by more than just macroeconomic trends. san francisco and the bay area is in the early period of their cyclical upswing. and i would posit that san francisco in particular will continue to trend up (not necessarily housing prices, but the local economy generally) as the center of gravity of silicon valley slowly slides north as we move from silicon to biological and genetic basis for technical advancements.

satchel checker,

thanks for keeping me honest 🙂 And I can accept most of what you say. And now that I know that you are a deflationist too (I didn’t pick that up before), I look at your comments in a whole new light!

Interesting idea you have about tech migrating fom silicon to “carbon” and that SF will reap the lion’s share as this migration occurs. You could very well be right.

Apologies for getting snippy with you. You are a great satchel checker – I take back my criticism, especially now that I understand we are on the same deflationist team!

Why would expanding business migrate to more expensive cost per square foot locations.? If someone can show any evidence of technology firms LEAVING the peninsula and south bay and coming back to the city I would be very interested in this as it would change my own long term outlook on ownership of investment properties in the city. I am NOT talking about opening a boutique satellite office for 35 creative types in South Park, but companies actually moving back to San Francisco. I understand you may be writing about new developing technologies, but as they grow larger would Mission Bay be the ideal sought after location for the majority of their employees?

Beoing moved their headquarters from Seattle to Chicago because it was cheaper for employees to afford housing than Seattle, and for the company to relocate in a premier building at a lower cost per square foot than downtown Seattle. Affordable Housing was listed as the number one desire of their corporate staff, followed by good public transportation and civic cultural institutions. We only score well on one of the three I am afraid.

(Loola) brought up an error of statistacal logic. Median prices CAN go up if sales go down and nonconforming loans go away for 2 reasons:

1) I’ve heard that people are doing 2 conforming mortgages instead of 1 jumbo (due to qualifications). Thus, the loss of Jumbo mortgages may not be hitting SF as much as many (myself included) thought it would so long as there are other alternative financing strategies.

2) the nature of a “median” set. the median is simply the middle number in a set, it is not an average.

quick example of a market where high end gets hit hard, low end does NOT get hit, and yet median goes up:

9 house sales:

400k, 400k, 400k, 400k, 410k, 600k, 800k, 1M, 2M

Median price is 410k

now conforming are knocked out

400k, 400k, 400k, 400k, 500k, 500k, 510k, 600k, 700k.

new median: 500k.

Median goes up, but you can clearly see that prices of high end stuff came way down.

I am NOT saying this is what is happening in San Francisco. Only that it is a possiblity, and a reason why many try to combine median with average values. and it highlites the importance of understanding what the statistic is telling you! (warning to bulls/bears alike)

===

Also:

Fluj: I’ve said I’ll admit to being in error if a downturn doesn’t come to pass… but as a reminder my call is that we don’t start to see any SF stress until late Spring 08 when ORH/Infinity etc open up… and we don’t see “pain” for 3-5 years… most of which being loss of home value through INFLATION. however, 5 years of slightly negative RE values with yearly inflation of 3-4% will still be deadly to many people.

as a somewhat boring aside for those of the geeky persuasion:

as we all have argued ad nauseum, there are massive issues with both median prices, and average prices.

thus, for those who are interested, what I did in my own personal market research years ago in San Diego was to look at EVERY sale in my area of interest (certain zip codes of SD), and then I excluded all properties that were above and below 2 standard deviations of the median price.

I then charted the average and median price for the REMAINING properties. this helped me exclude the major noise that the super high end and super crack houses exert on average pricing.

for me it was enlightening, and I felt it gave me a better handle on what was happening in MY segment of the market.

there are so few sales in SF that one could easily pull this off for oneself… but it takes some work. no relying on DataQuick! 🙂

I can’t see much financial argument for floating half your loan on a HELOC (with a significantly higher % rate) to avoid doing a non-conforming loan. Maybe I’m missing something but the price break you get on the conforming portion would likely get eaten up by the much larger portion of total debt financed by a 2nd.

In any case, there’s some problems with a lot of the econ discussion above. Inflation is about money supply (true) prices is the yard stick our central banks use to determine whether there is too much or too little money sloshing around the world. So you can’t look at rising prices (CPI, CPE, PPI, etc.) and randomly conclude deflation. Prices are rising, based on these measures. That’s signaling to the Fed that there’s too much money sloshing about.

Second, the Fed can create better terms for markets (e.g. lowering the rate at which banks can borrow from the Fed) but can’t force banks to borrow or lend. The credit crunch stems from lack of liquidity. Liquidity is a proxy for confidence. The Fed can’t manufacture confidence, force banks to lend to each other, or force banks to lend to you and me. So you can see the Fed lowering the cost of capital while simultaneously seeing banks shut off their spigots.

I understand the arguments over whether or not the median price data is indicating that prices are higher or lower. Bulls and bears interpret it differently.

I don’t understand the dissension over interpretation of the sales volume. It’s lower YoY for 34 consecutive months and November is the weakest sales volume of any November since DQ started keeping track in 1988. Sure you could look at noise over the last couple months and try to bend it to your view either way, but it’s just noise. ..

Ignore the data, “It’s a great time to buy or sell a house.”

^^^ pure snideness ^^^

Satchel: “I figured you were a victim of some public school system, which spent more time on “justice” than real history. Hmmmm.”

Satchel, your true colors may be showing. You purport to dispense rational advice couched in macro-economic terms worthy of an Oracle of Delphi, but I am beginning to wonder whether your analysis is more ideological than scientific.

“Don’t pay any attention to actual SF sales data showing steadily, gradually rising prices, the Almighty Bubble is upon us!”

I don’t get the impression that anyone around here has any intention of buying property, maybe ever. Perhaps it’s just that those who post are more polarizing and the middle ground readers don’t post? All I see in the comments are cheerleaders fighting with bears. Now there’s an image for you…

Back to the topic.

While it is true that some jumbo loans are replaced by multiple conforming loans, for the reason of qualification and even lower rates (at least for the 1st one), it is often NOT a good strategy for the buyer.

If the buyer is under AMT (which we didn’t even know what would happen until two days ago), only the first loan is deductable. Second loan is likely to have higher rate and not deductable.

Unless the total loan amount is very close to the conforming loan limit, I don’t see it being a good strategy.

So, I am with Loola and I have said this way earlier in the thread – people have healthy balance sheet and able to put down larger down payment.

Fluj, it’s not pure snideness to quote the text of a NAR ad, especially as said organization’s chief economist has been screaming “bottom” all year while constantly revising sales and price targets downwards.

“I don’t get the impression that anyone around here has any intention of buying property, maybe ever”

I’m actively looking every week, but then I don’t consider myself a bear even though I do think that prices will at best stagnate over the next few years. As for the market I’m looking at right now, I see a lot of properties just sitting there unsold at “wishing prices”. So no significant distress on the part of sellers, but not exactly the market of two years ago either.

John – it doesn’t matter wheter or not it’s a good stratgey, it’s being driven by buyers who no longer qualifying for a jumbo loan. Talk to some mortgage brokers.

From the DQ report on SoCal:

“Jumbo-financed purchases represented nearly 40 percent of sales this year before the August credit crunch, while last month they accounted for 22 percent. Also, the number of homes purchased with the highest conforming loan possible – $417,000 – has roughly doubled since jumbo loans became pricier and harder to obtain in August.”

It’s not only happening here/there.

You can’t stack conforming loans.

And Dave, “cheerleader” ? You want balanced dialogue, but you insert “cheerleader” into the mix?

Look at the language used on S.S. honestly for a second.

There are far, far more glee club type comments along the lines of “Rah rah witness the imminent demise!!!” from the bearish sector than the few “cheerleaders” questioning exactly how we’re supposed to be imploding amid record high median sales.

This stuff is not helpful. There really are lots of buyers out there thinking they can game the market right now. They can’t. The volume is down because sellers are just waiting it out. If they stay patient someone will usually emerge and buy the property at close to what they want. Two months for a sale is no sign of the apocalypse.

“The volume is down because sellers are just waiting it out.”

“The volume is down because buyers are just waiting it out”

Just as true or untrue!

Yeah, you’re right about that Amen Corner. It takes two to tango as far as that goes.

But we’re seeing buyers submit 10 and 15% under asking contingency laden offers, to no avail. These are offers that are still historically quite high. That’s down to sellers being patient more than buyers waiting on the sidelines.

fluj, I didn’t say anything about balance. A 50/50 mix of extreme bulls and extreme bears is balance, but still doesn’t represent the middle ground. I was commenting on the lack of representation among the middle ground, which is where I sit.

I just bought a foreclosed SFR in Noe. I don’t think I got a great deal, given the amount of work the place needs, but it was a haircut from the last sale two years ago. Deals are out there now, but not great deals. I waited two years until I finally saw something worth taking (and got tired of renting).

Did you actually go down to the courthouse steps, Dave? I don’t mean to pry too much. Without telling us too much about it can you elaborate a bit? Was it competitive?

Re the migration of $ from Sili Valley due to bio taking hold mention earlier (i.e. biotech, clean tech, green tech, etc.):

Just look at where many of these companies are based RIGHT now: East Bay and South City. Mission Bay is also making a strong play for more of them.

Baybio is a good source of info for those interested.

Not really, fluj. Everything has a price and these buyers’ prices are presumably 10 to 15% under asking. They _are_ sitting on the sidelines in terms of the prices sellers are asking:- that’s why sales have declined year over year for 28(?) straight months.

Here’s an example btw. 1483 Sutter #312. Orginally on sale for $1.05m, turned down offer for $950k a couple of months ago, now on sale for $970k, dom 107. Will they get more than $950k out of this?

I guess it’s a matter of semantics, amen corner. My take is that if they are actively submitting offers they aren’t on the sidelines. They actually think that it might work. They are dynamic. It is the sellers who are static in those situations. I can see your point, tho.

fluj,

You said “you cannot stack conforming loans”. Can you elaborate on that? I know it is possible to take multiple loans. What are the rules?

fluj, the sellers aren’t on the sidelines either by virtue of the fact that they have put their property on the market. I don’t see this as any different from a buyer submitting offers below asking. They are both in the market at a particular price point, it’s just that their price points differ:- hence continually declining sales (the most interesting stat I derive from all these numbers, btw).

No, I was not at courthouse steps. Investor bought the house and tried to flip it after doing nothing but a horrible spray paint job. It sat for months with a stupid price tag, flipper lost it to the bank, the bank auctioned it to some 3rd-party clearing-house-type-of-company based on the East Coast. That company put it on the market in the MLS and sold it through a local agent.

I suspect we got a “deal” b/c too many people were scared off by the amount of work needed. There were three bids but we got it for $20k under asking b/c we had the cleanest offer. No inspections and no contingencies. Not for the faint of heart… All told though, we paid $300k less than what the county had on record for the last sale.

John, individuals can’t take out more than one conforming loan on an singular property. The conforming loan limit for SFRs is 417K, on through 2008. Nor can any lender can offer a second that’s equal to or greater than the first.

http://www.fanniemae.com/aboutfm/loanlimits.jhtml

I suppose some people are doing the following: $1M purchase, 400K down, 417K loan, 183K equity line or second. I wouldn’t, personally.

fluj,

So, if the first loan is a conforming loan, the second will have to be higher rate, right?

What’s the max one can borrow for the second loan, if the first one is conforming?

John, I don’t really know all the ins and outs to mortgage financing. These are questions for a home loan banker or a mortgage broker. I wanted to tell you the limit for seconds after a conforming in my last post but I couldn’t find it doing a simple search. Somebody on here will step up and tell you I’m sure.

“horrible spray paint job” = desperate attempt to cover up water damage or other fundamental flaws.

Other techniques that I’ve seen by hack flippers :

gluing down rattan “carpet” to cracked and crumbled too thin concrete slab

hastily installed sheetrock in what was once a damp basement storage area to create a 3rd “bedroom”

grass sod that has no chance in hades to survive a few weeks past the the offers date dropped down over substandard soils with no irrigation.

These folks give the good flippers a bad name.

Dave – sounds like you did your homework and I’m sure you are grateful that you waited.

“Why would expanding business migrate to more expensive cost per square foot locations.? If someone can show any evidence of technology firms LEAVING the peninsula and south bay and coming back to the city I would be very interested in this as it would change my own long term outlook on ownership of investment properties in the city. I am NOT talking about opening a boutique satellite office for 35 creative types in South Park, but companies actually moving back to San Francisco. I understand you may be writing about new developing technologies, but as they grow larger would Mission Bay be the ideal sought after location for the majority of their employees?”

I’m not suggesting that high tech companies that already exist down on the peninsula are going to migrate north. i agree, that seems highly unlikely (although I do think you’ll see more companies open substantial offices in the city vs. bussing people down to silicon valley)

my point was more that the next wave of companies will spring up where the ecosystems of the big players in the industry meet where you can find the engineers and scientists. nasa begat fairchild, which begat intel, which pulled in thousands of top flight engineers and scientists, who then left to create or help build the next generation of companies, and all the while stanford and berkeley pumped new talent into the system in the form of fresh graduates. san francisco played the supporting role, providing the services to keep that machine going, because there’s not a significant base of engineering companies, talent, or a stream of graduates. the south and east bay ruled.

but for the next wave, i would suggest the big players are the genentech’s et al of the world (the majority of whom center around south city, the east bay and increasingly mission bay) that are spinning out scientists and engineers creating and building the next generation of companies, and stanford, berkeley, and now ucsf play important roles feeding that beast with new biophysicists, genetic engineers, molecular biologists etc. (not to mention a boatload of grant money)

that just seems like a long term trend that will play in favor of san francisco in particular. instead of being a service provider, san francisco moves more to a hub position holding the whole bay area together.

I could be totally wrong.

“but for the next wave, i would suggest the big players are the genentech’s et al of the world (the majority of whom center around south city, the east bay and increasingly mission bay) that are spinning out scientists and engineers creating and building the next generation of companies, and stanford, berkeley, and now ucsf play important roles feeding that beast with new biophysicists, genetic engineers, molecular biologists etc. (not to mention a boatload of grant money) ”

this wave has already happened IMHO. 6 years ago Genentech and Gilead and Chiron and others were relatively small. genentech’s employee numbers have tripled and revenues quadrupled in this time. Gilead has more than quadrupled in both numbers and there are more than 20 new biotech in SSF since last. Amgen moved their clincial ehadquarters to SSF 2 yrs ago and Elan moved all their employees to SSF from San Diego last year.

SSF has always been the hub of biotech.

“I suppose some people are doing the following: $1M purchase, 400K down, 417K loan, 183K equity line or second.”

Fluj,

Why would someone put down $400k when the general requirement to avoid PMI is 20%? Wouldn’t a more typical scenario be $200k down, 417k first, 383k HELOC or second? Please explain, thanks!

Remember, I said I wouldn’t do it. If possible I would do something along the lines of what you mentioned. I merely used that scenario because I actually saw something similar. I picked $1M because it is a round number. As far as a 383K HELOC behind a full conforming first, yeah, that’d make more sense if it is possible. I want to say that LTV ratios and guidelines for seconds and HELOCS preclude that from being possible. 383 is nearly the same amount as 417. But I don’t really know. Anybody?

I guess no mortgage brokers frequent this site any longer

So…population is growing…tech companies are pumping out millionaire after millionaire…biotech is booming…rates are still low…and sales have been declining for the past four years?

Are you serious?

satchel,

you are very good at regurgitating what you hear on the morning calls from hq everyday. when was the last time you had an original idea? don’t take that the wrong way, everyone has to earn a living and i did the stockbroker thing for a few years out of college too. i had a fundamental problem with the model however in that you have to churn accounts to make money and to keep your job. when is that ever in the best interest of the client? that was rhetorical by the way. it never is.

the model is broken in your business and i’m sure you know it, reading your posts. you not only have a very good memory for reciting all that you’ve learned from your training which tells me you are also in possession of above average intellect. stockbrockers should not be rewared for transactions. they should only be rewared for growing clients assests. when they make mistakes or push the crap that their firm underwrites, tehy should get nothing.

that would insent the correct behavior.

thoughts?

as for my investment strategy, i thought the etf’s from bgi were brilliant when they first started and i couldn’t beat them so i joined them. real estate in places like sf and the peninsula are really tough to beat however over the last 10 years. i gave up trying and bought plenty to hold of that.