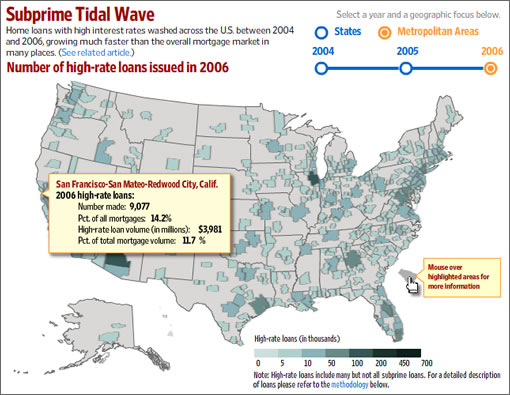

According to the Wall Street Journal, in 2006 a little over 14% of all new mortgage originations in the San Francisco MSA (which includes San Mateo and Redwood City) were “high-rate” loans. In San Jose (which includes Sunnyvale and Santa Clara) the percentage was 19%. And in Oakland (which includes Fremont and Hayward) it was 25%.

And while those percentages are likely to be both more and less than many expected, we will offer a few other MSA’s for perspective: New York 28%, Los Angeles 32%, Chicago 33%, Phoenix 34%, Las Vegas 36%, and Miami 48%.

And now, we’re not sure whether to be relatively relieved (in terms of the Bay Area) or absolutely frightened (in terms of the country as a whole).

∙ The United States of Subprime [Wall Street Journal]

∙ Wall Street Journal Interactive Graphic: Subprime Tidal Wave [WSJ]

And if you look at a mapping for DTI, and LTV, it pretty much looks the same.

But don’t worry! SF is immune! Buy now or be priced out forever! The collapse of the housing market in surrounding areas will have *no* *effect* on SF prices! Prices only go up!

Now that I’ve gotten the shilling out of the way, anyone want to guess what will *really* happen, as REOs go through the roof in outlying areas to SF Metro?

the accompanying article will be pretty eye opening for some …

http://online.wsj.com/article/SB119205925519455321.html

I’m somewhat surprised that the SF-San Mateo-Redwood City shows that only 14.2% of all mortgages were high rate loans… That’s one of the lowest percentages for a metropolitan area.

I’m not surprised that the bay area numbers are significantly lower. Given that something like 80% of loans originated in the city and peninsula are jumbo, this in itself indicates a lower percentage of sub prime. Even with the ease in lending standards (2000-2005), jumbo loans were more difficult to qualify.

^ Ah.. I see..

I think the reason the SF-San Mateo-RWC areas have a lower percentage is probably because a lot of the home purchases were not from first time buyers. I think many of the buyers in this market came in with a lot of cash from previous home sales and put more money down than first time buyers. Where as first time buyers would look at starter home outside the peninsula and SF.

That doesn’t mean they didn’t over buy or over extend themselves.

While this data is good I doubt it will accurately predict the market in these areas in the upcoming years.

Would only add that, last time I saw similar data, our MSA had a low % of subprime lending, but one of the highest average subprime loan balances, around $400K.

Jim D –

You see it happening currently – major price reducations. Can’t escape the fact that with all that new construction plus other obvious market conditions. To get top dollar you need a good product priced right – the days of bad locations, mis place emotion for poor products will vanish untilt he cycle comes back around…

Here is a great quote from the article:

“We had an aggressive home-mortgage industry trying to get people into homes they couldn’t afford at a time when home prices were very high. It turned out to be a house of cards,” says Karl Case, an economics professor at Wellesley College. “We’re in the early stages of the cleanup.”

again, not surprised that there are far less high rate loans in SF than elsewhere. Tons of people in SF make tons of money and also tons cashed out on their last home sale.

OK. I’m not afraid to admit it – I’m either dense or just low on caffeine today. Why would these numbers absolutely frighten our dear Editor?

[Editor’s Note: Or neither (and we simply weren’t clear enough). “Relatively Relieved” = stats for the Bay Area relative to the rest of the country; “Absolutely Frightened” = implications for the country as a whole.]

What surprised me is how much lower SF MSA’s percent of subprime buyers was than the other cities….many of which are also high cost by the way (e.g. – NYC and LA). While many people obviously over-extended themselves here, it seems that home buyers in the San Francisco MSA are in proportionately in better financial shape than in other parts of the country. I’m actually kind of confused with some of the posts here. Why wouldn’t this suggest that RE values here should be less negatively impacted than places like Stockton for example?

A lot of the posters are sanguine that this means that the Bay Area (and all of California really) is taking out good loans, unlike the rest of the country.

This chart is actually completely useless for determining that.

Here’s what they used as a definition in the methodology: “High-rate loans are defined as those having an annual percentage rate of at least three percentage points above a Treasury security of comparable maturity for first-lien loans and five percentage points for second-lien loans.”

Now, how would a 2/28 with a low teaser rate, or an Option ARM, or a 3/1 be counted? Maybe the greater use of ARMs in the Bay Area brings down the number of “high-rate loans”. I would speculate that anything with a variable adjustment is counted with it’s up-front rate in the year it is originated, and thus a low teaser rate is not “high-rate”. The methodology notes: “High-rate loans are considered to include many, but not all, subprime loans.”

Honestly, given the housing prices here compared with say, Texas or Nevada, I suspect what the data is showing us is that in the the last two years, a lot of people in California were taking low up-front rates just to be able to buy (perhaps in the hopes of refinancing later). In other places, where homes are more affordable, they are make payments with higher fixed-rate subprime mortgages.

Thanks ge! When I first looked at this I was wondering what exactly a ‘high rate’ loan was.

I admit the low numbers for the SF MTA surprised me as well, considering that last time DQ posted mortgage info +70% of all mortgages in CA were some from of ARM in ’05 and ’06.

But it seems that a high use of ARMs and other ‘affordability’ products are not necessarily reflected here.

I guess we will just have to wait and see how it plays out.

GE, that is a good point and you could be correct. With that said, why wouldn’t that same logic of low teaser rates skewing this apply to NY or LA? They are high cost markets that are prohibitively expensive as well. It would indeed be very interesting to know if these stats are based on the fully indexed rate or the initial adjustable portion.

Ahhh… I get it. Thanks, Editor!

And that just goes to show you how geo-centric I am. It didn’t occur to me to be frightened for the rest of the country. I was only focused on SF and environs.

And, in the interest of full disclosure, I’m a renter who refused to jump in during the last few crazy years. So, what would frighten or relieve me may certainly be different than what would affect others.

Thanks again for the clarification. It’s part of what keeps me plugged in!

GE — I add to the chorus of “good points.” This chart refers to “high interest” (generally subprime) loans. SF logically would not have a tremendous number of those since even in the bubble years high interest on a jumbo loan (about the only kind there is in SF) would mean high payments. But SF saw an extremely high percentage of “alternative” loans in 2005-06 — no doc, teaser rates, etc. As many have noted here, these types of loans bring similar, but not identical, concerns — people bought more house than they could afford betting on perpetual appreciation.

Actually, if you have a good credit score, sometimes the lender doesn’t even need to see the proof of income, thus making the loan alt-a.

So, if all those “alternative” loans were made to the people with the best credit, there will be little hope for a real price drop of resell homes. On the other hand, if those “alternative” loans were made to people who couldn’t afford it, we all know where the market is going.

It is just funny two completely opposite situations show up as the same in this mortgage system.

Not surprising, and we all obviously different crystal balls. This backs up my own experience that the people around me put 25-50% down on $1M+ homes and I don’t think they’re in any danger whatsoever. But it doesn’t speak for the whole city of course…

And I totally agree that the crap is no longer going to float and we’re about to experience some serious social darwinism in the mls listings. But at the same time, assuming we can all agree on what is a right price (yeah right), and we can all agree on what defines a beautiful home (yeah right^2), I think quality will continue to shine as it has in previous crashes (meaning this will work out roughly like what’s going on in Santa Cruz county right now in that the crap will experience that 30-50% decline, offset by the jewels going down much less, if at all, balancing it all out at a 20% overall decline).

Obviously, if one were investing in any real estate for short term appreciation right now, one would also be an idiot. But I also think there are going to be a lot of new slum^H^H^H^Hlandlords next year once the subprime reset knocks that sector of the market into instant positive cash flow for people sitting on piles of money. Things don’t look good for the middle class IMO

Hey this isnt Slashdot, noone gets your cute key mapping references.

[Editor’s Note: Don’t be so cocky^H^H^H^H^Hsure about that.]

Hah! my bad, try the following then

stty erase ^H