The good news: according to the OFHEO, home prices in the United States increased 3.19% year over year in the second quarter of 2007 (many had predicted a historic drop).

The not so good news: OFHEO reported home prices dropped 1.38% year over year in California (only Michigan and Nevada recorded higher declines) and .86% in the San Francisco-San Mateo-Redwood City MSAD (versus a 1.32% year over year gain in Q1).

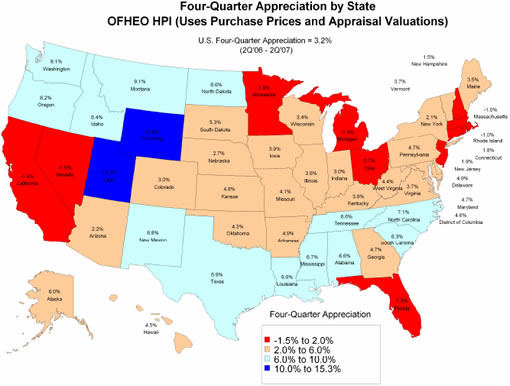

U.S. home prices increased only slightly in the second quarter of 2007 according to the OFHEO House Price Index (HPI). The HPI, which is based on data from sales and refinance transactions, was 0.1 percent higher in the second quarter than in the first quarter of 2007. This is below the revised growth rate of 0.6 percent for the previous quarter and the lowest since the fourth quarter of 1994. Prices in the second quarter of 2007 were 3.2 percent higher than they were in the same quarter of 2006, the lowest annual price change since the 1996-97 period.

“House prices were basically flat in the second quarter despite tightening credit policies, rising foreclosure rates, and weakening buyer sentiment,” said [OFHEO Director] Lockhart. “Significant price declines appear localized in areas with weak economies or where price increases were particularly dramatic during the housing boom.”

That being said, do keep in mind that “[t]he data in this release only include price information through June. To the extent that recent mortgage market instability may have affected housing demand and prices, those effects would be evident in OFHEO’s next HPI release.” (Yes, we’ll keep you plugged-in.)

And once again, the HPI is based on data from repeat single-family home sales, or refinancings, that involve conforming mortgages (under $417,000). Data from transactions involving either condominiums or non-conforming loans (two major components in the San Francisco market) are excluded from the Index.

∙ OFHEO: U.S. House Prices Slow (pdf) [OFHEO]

∙ OFHEO First Quarter Report: 0.35% Appreciation For SF MSAD [SocketSite]

Very interesting report. Note the detail for the various MSAs starting on page 29. San Francisco (extending through San Mateo-Redwood City) saw a price decline of .86% in the last year with most of that (-.61%) in the second quarter. Also, 7 of the bottom 10 (and 12 of the bottom 20) in terms of year-to-year price declines are in California.

And this was all before the recent meltdown.

Still, 5-year gain in SF of 52.1%. Not too shabby.

But I don’t think these 2Q numbers are as interesting as August and Q3 numbers will be.

I would really like to see a survey on socketsite that showed 2 things: first if people are renting with no intention of buying, own, or renting with the intention to buy when prices are right, and second, what people are predicting for pricing trends. There may be some intersting correlations. I would not at all be surprised if the data showed a strong correlation that owners are predicting that prices increase or worst case are flat or slightly decline. And that renters / potential buyers are predicting that prices will decline in the near term.

[Editor’s Note: Damn thunder stealing comments (we have the data from our last reader survey and will release it in two weeks).]

I don’t buy those reader survey results for a minute.

And AC:

“I would not at all be surprised if the data showed a strong correlation that owners are predicting that prices increase or worst case are flat or slightly decline. And that renters / potential buyers are predicting that prices will decline in the near term.”

That is exactly what we would see, no doubt.

Another way of putting it: those who currently own want prices to keep going up. Those who don’t own are waiting for them to come down. Since those who don’t own are the demand side of the equation (i.e. they are the market), owners/sellers won’t have much choice unless they plan to hold for 10 more years.

Like the hedge funds out there, owners can keep “marking to model” or “marking to fantasy,” but eventually you need to face reality. Reference the recent Chronicle sob story about the family in Oakland whose home was “worth” $450K but they could only sell it for $350K. Guess what? It ain’t worth $450K regardless of what your Realtor tells you. If your Realtor thinks it is, tell them to buy it.

Final caveat: OFHEO data is predominantly based on conforming loans, so it’s not especially relevant to SF given 80% of the loans here are non-conforming. But interesting data nonetheless.

I’ve been watching the properties for sale in Medina Ohio (suburb of Cleveland) for the past two years. The reality is that there are very few sales happening. If a house is above $300,000 it usually has usually been re-listed multiple times. A typical example is a house that finally sold in June at $400,000 after being originally listed at $575,000. I think in many markets the price decline isn’t accurately reflected because there few sales.

[Editor’s Note: Damn thunder stealing comments (we have the data from our last reader survey and will release it in two weeks).]

Dear editor,

I think the results of a reader survey conducted now versus conducted back in June might be quite different. Plus, I didn’t participate in June and feel left out.

My opinion counts damn it.

[Editor’s Note: Trust us, there’s no need to fret (or feel left out). We’ll give you another chance to participate soon enough.]

Given that these numbers are limited to conforming loans, one does have to do a bit of putting-the-pieces together to draw any conclusions. If you take the Case Schiller numbers, which show a 4% SF price decline overall in the last year, and the OFHEA numbers, which show about a 1% SF decline for lower-end sales with conforming mortgages, one might conclude that prices at the higher-end have declined more than those at the bottom. This would follow the pattern of the price decline in the early ’90s.

“I think in many markets the price decline isn’t accurately reflected because there few sales.”

This is the natural behavior of the marketplace.

In a slowing market there is no impulse to sell unless it is based on need (job loss or transfer, death, divorce, birth).

What a surprise! The Bush administration wants NO rate cut, so everything is skeweed as far as possible to look rosy.

The worst whoring of the day though was the downgrade of Wal Mart to “sell” by an investment bank who wants a rate cut. Wal mart probably doesn’t care: they want a rate cut just as badly.

Man, there’s three weeks to go before September 18. This is just going to get more and more polarized, with every government report being skewed as far as possible to make things look good, and every investment banker up to their eyeballs in mortgage-backed securities selling their souls for a rate cut. (I know: what souls?)

I’m assuming Bernanke sees through all this whoring and posturing and will come to his own conclusion.

I don’t like how the media covers these numbers. They call it “good news” that home prices haven’t dropped nationally. Good news that so few people can afford to buy a home? Good news that we are continuing with a propped up overinflated bubble? A comment I read somewhere about public risk and private reward keeping ringing in my mind. The private reward has been wrung out of the housing market. Hello public risk.

Oh – and I stand by my readers survery answers. Still true, and haven’t changed my mind on anything – perhaps a bit more certain that we are looking at a long rough patch for a lot of home debtors.

“In a slowing market there is no impulse to sell unless it is based on need (job loss or transfer, death, divorce, birth).”

That’s very true but there are at least four new needs that might change that natural behavior of the marketplace: interest rate resets, the inability to refinance due to tighter underwriting standards, negative cash flow “investment” properties and unsold new construction.

“I’m assuming Bernanke sees through all this whoring and posturing and will come to his own conclusion.”

That’s what some Fed watchers are predicting:

http://www.reuters.com/article/ousiv/idUSL3050022820070830?sp=true

But I bet they fold eventually. Not that it will help much.

So national house is actually up 3.2% y/y.

To me this means that there is absolutely no need for talk of any kind of bailout of homeowners. With increasing house prices, consumers will still have the powder to keep spending.

Bill Gross and others have been refuted by the newly released data. It shows that the problem is not with deflating house prices, but the value of their deflating mortgage security holdings.

“That’s very true but there are at least four new needs that might change that natural behavior of the marketplace: interest rate resets, the inability to refinance due to tighter underwriting standards, negative cash flow “investment” properties and unsold new construction.”

True too, but that factor is partially offset since a lot of people (say, 30-something MBAs) are earning a ton more money than when they bought a few years ago, so resets / refinancing / covering negative cash flow are not a big deal. When my ARM resets in 3.5 years from now my household income will probably be $100k more than when I applied for the mortgage.

“True too, but that factor is partially offset since a lot of people (say, 30-something MBAs) are earning a ton more money than when they bought a few years ago, so resets / refinancing / covering negative cash flow are not a big deal. When my ARM resets in 3.5 years from now my household income will probably be $100k more than when I applied for the mortgage.”

Many of those 30-something MBAs were still in school When Genius Failed in 1998 and don’t have a real world sense of what transpires when things get less “easy” as they have been for the past 5 years. But they’re getting it now; many of the hedge funds that have blown up recently are staffed with extremely bright 30-something MBAs. What’s fascinating to me is, if you ask some of them about the P/E of a public company, they can give you quite brilliant insight from a dozen different angles. But if you ask those same persons about the P/E of the home they own, they rarely know what it actually is, and how that compares to historical levels or other cities.

I don’t mean this as a knock on MBAs. Most people don’t know those answers. My point is two fold. First, MBAs cannot rescue the day simply by making more money, because the are not insulated from the global economy. Second, we should take no comfort from the willingness of a 30-something MBA to buy a house, especially if he or she is completely concerned about negative cash flow, which most MBAs would be rightly concerned about if investing money for a client. The rigor of analysis applied to private equity investments, venture capital, and public equities tends to be far beyond that applied on one’s home. Mostly because the conventional wisdom is that real estate always goes up in value over the long run. Isn’t conventional wisdom always correct?

There is another, growing problem that we’re seeing. In addition to all those who bought more than they could afford at the peak because they could do so with creative loans (and may or may not be able to keep up with re-setting ARMs), an awful lot of people here who bought long ago at affordable prices refinanced and refinanced again until they now can no longer keep up. A quick glance on PropertyShark reveals a huge percentage of foreclosures resulting from this situation. These people do not now earn 100k more than when they bought. They have already tapped all their equity and more, and lenders will not pour more money in any longer. There has been no job loss or transfer, death, divorce, or birth — these large numbers just made their affordable places unaffordable and they will have to sell.

There’s a little good news and a little bad news in here for everyone.

I think there’s really good news for those who want a more “marginal” property (e.g. starter home in starter neighborhood), bad news if you’re selling one of those. If you want to buy in Daly City or South SF or East Palo Alto, prices are falling and inventory is way up. Don’t take my word for it. Go do a search on Ziprealty or trulia or whatever. There seem to be very good deals due to abundance of inventory. The 1% drop in OFHEO includes SF, Marin and San Mateo county (SFR under $417k — where do people find SFRs under $500k?). The 4% drop in Shiller/Case includes the above, plus Contra Costa, Alameda, etc. Alas, my dreams of buying a SFR in Palo Alto for $600k are probably going to remain unfulfilled…

The effects of that 30-something MBA crowd are overstated. Half these people are buried in student loan debt with little cash, so in today’s environment they’re not getting $900K loans like they were a year ago. Plus, hopefully, most of them are smart enough to read the papers and realize they may be well served by waiting a year or so to purchase.

Besides, if they work at hedge funds or in banking, many are probably more worried about whether they’ll even have a job next year….

Sounds like a lot of nervous owners are grasping at straws, trying to “preserve their equity.” Sorry, but nobody wants to catch a falling knife. Not MBAs, not rich foreign investors, and not retired empty nesters. Hope you can all afford your ARMs when they adjust…

That’s very true but there are at least four new needs that might change that natural behavior of the marketplace: interest rate resets, the inability to refinance due to tighter underwriting standards, negative cash flow “investment” properties and unsold new construction.

My comments about the marketplace were meant to describe the behavior of owner occupied residential real estate, and why they are holding back from selling properties now, not speculative real estate investors, or commecial multi-family real estate investments.

Homeowners, who have fixed rated loans are not effected bycash flow, stricter underwriting standards, or raising interest rates or unsold new construction. These conditions have more of an effect on buyers, not sellers.

These will not prompt an owner to sell.

Dude, anyone can rephrase your exact same setence the opposite way, e.g.:

Sounds like a lot of nervous renters are grasping at straws, trying to “justify their staying in a rental.”

Anyway, I’ll be happy when it is a year or two from now and we can hopefully move on from this endless speculating on the same exhausted topic ad infinitum, although I am certainly guilty myself.

I am wondering if there is any value whatsover in these threads, other than pure entertainment. Probably not.

The OFHEO numbers are far less interesting that the Case-Schiller and other indices. I recommend this article, but particularly the accompanying graphic and video, from the New York Times.

[Editor’s Note: Keep in mind the NYT graphic for San Francisco is based on the S&P/Case-Shiller index which represents the greater San Francisco MSA and should look rather familiar if you’ve been plugging in.]

AC: you’re right – let’s agree to disagree and let the market tell it’s own story. We can revisit in 12-18 months. By then, I’ll still be able to afford my rent without moving. Wonder how many current homeowners can say the same thing?

I can see it now….

OFHEO: SF REAL ESTATE FORECLOSURES (pdf) [OFHEO]…

“…a recent trend in San Francisco’s real estate market is foreclosure due to homeowners losing their jobs because they spent too much time reading and commenting on Socketsite.”

I predict in 24 months we will start predicting when the next boom will start.

“Homeowners, who have fixed rated loans are not effected bycash flow, stricter underwriting standards, or raising interest rates or unsold new construction.”

That’s true but the majority of new homeowners in San Francisco made their purchases with short term and adjustable rate – not fixed rate – mortgages over the past five years. A new condo hitting the market because a developer can’t wait out the market and has to pay off a construction loan looks no different to a buyer than a condo that hits the market because of one of the not so rare homeowner needs you outlined.

“We can revisit in 12-18 months. By then, I’ll still be able to afford my rent without moving. Wonder how many current homeowners can say the same thing?”

I will be able to say that, even though I just bought six months ago. And I will also still be able to say I no longer have any worries about getting evicted, which happened twice in last eight years before I bought. I have a lot more control over my monthly housing cost now then I did as a renter when it would increase dramatically every time I was forced to move for reasons beyond my control.

“I am wondering if there is any value whatsover in these threads, other than pure entertainment. Probably not.”

I disagree. Although it is a lot of rehashing, every time we discuss it there are “new” people popping in who may never have heard of any of this.

also, the market is fluid. The events transpiring now will be different in the future. one day makes not a trend… but several months do.

A home is THE MOST important purchase most people will ever make in their lives. Too many homebuyers rely on people they think are experts, but who are really salespeople with a conflict of interest. (i.e. RE agents, Mortgage brokers, developers, etc). nothing wrong with that, but also good to make people THINK before they shell out good $$$…

“A new condo hitting the market because a developer can’t wait out the market and has to pay off a construction loan looks no different to a buyer than a condo that hits the market because of one of the not so rare homeowner needs you outlined.”

Have to disagree — the new condo is priced at a premium relative to the resale market and the developers have historically shown an amazing ability to “wait out the market” — at least in this market. It took years for the developer to sell out the Brannan towers for example, but they got their prices!

“What a surprise! The Bush administration wants NO rate cut, so everything is skeweed as far as possible to look rosy.”

Just proves the theory that people can twist anything to fit their myopic view of the world. If Bush were pushing for a rate cut you’d be claiming he’s out to save the hide of his banking and hedge fund cronies. The reality is, a rate cut would probably save a lot of lenders and investors that need to get their asses handed to them or go out of business. Only then does the industry self-reform…at least for awhile.

A bit late, but just had to comment on the 30-year old MBA posts:

Those 30-year old MBA’s should talk to a few 40+yr old MBAs for a dose of perspective. Perhaps your comp will be up $100K + over the next few years….but maybe not.

Our Ivy-league MBA household had great comp through the late 90’s (although nothing compared to the dot-com stories we all heard about). Even hit seven figures in 2001. Then in 2002 it dropped by half. Literally. And we were better off than many – still had a job with still-high comp. Doesn’t anyone remember all those folks with massive tax liabilities from suddenly-worthless stock options??

But we never lost a night’s sleep since we had bought a small house several years earlier at 1.5x income. Seemed like everyone around us was moving up during the boom years, but we stayed put. So when comp took a nose-dive and investments cratered (stuff that was 10x on paper now worth $.10 on the dollar), it was disappointing. But not tragic. Life pretty much went on as usual.

So please don’t think because you’re smart and well-educated, and even have a great job now, that things will only go up. If anything, the jobs that MBAs often go to (i-banking, hedge funds, professional services) are even more prone to comp swings (swings go both up and down) because they are heavily bonus-based.

Years ago a good friend who lived in Westchester County NY told me that all the smart i-bankers in his neighborhood paid cash for their houses, because they never knew when their comp and/or jobs would disappear.

It may be too conservative a view for some here, and perhaps it will keep us from being wildly rich (although we’re doing just fine in my book). But I’ve never lost a nights sleep over my mortgage. And that is priceless…..