BusinessWeek gives San Francisco real estate a “thumbs up” in terms of “Value for the Long Run.” And while we agree, the jury is still out with regard to the near term. From BusinessWeek:

Housing has gone from a sure thing to a complete muddle. Median prices fell nationwide for a second straight month in September, the first time that has happened since 1990, according to a report on Oct. 25. Homeowners don’t know whether to sit tight or bail. They have no idea whether they’re experiencing the beginnings of a deep bust that will leave a permanent hole in their wealth, or a small hiccup.

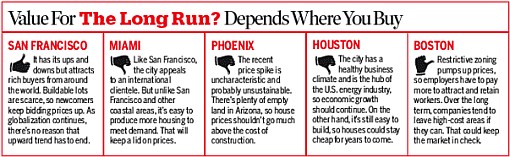

How do you know if your own local market is the kind that will snap back or the kind that will languish indefinitely? One key factor is the ease or difficulty of building new homes. Places where new home construction is a long and expensive process, such as Boston and San Francisco, tend to experience big price movements, both up and down. “Restricted supply leads to more volatility in prices,” says Edward L. Glaeser, a Harvard University economist who has studied big-city housing markets.

Key word: volatility. And then there’s that second to last paragraph: “Sure, [restricting housing supply] can make current owners richer by increasing the scarcity value of their homes. But it’s murder on first-time buyers. And in the long run, it’s bad for the local economy. As Glaeser notes, companies tend to migrate away from areas with costly housing to avoid paying the higher salaries needed to compensate employees for their home costs.”

∙ Boom! Bust! Boom? [BusinessWeek]

The Phoenix example is interesting. They make the traditional argument that in an area with plentiful land, home prices should not be rising much, since supply can more easily keep up with demand.

And yet there’s a price spike in Phoenix. A downtown condo there went from about $200k to just south of $400k in a few years.

Under the traditional theory of big-land cities that spread in all directions, the prices should not have gone up as much as they have. Which is why in Houston, new homes barely reached $200k.

If the new urbanists are on to something, then perhaps there is room for long-term value in a place like downtown Phoenix. Unlike the suburbs, downtown can’t simply grow out, right? Physically it could, but there is usually community opposition to upzoning in surrounding areas, so it would be hard to pull off politically.

If downtown land is artificially constrained, and there is specific demand for living downtown, there could be higher-than-usual price appreciation in urban cores, even in cities with effectively infinite space for suburbs.

I’m not saying Phoenix will ever have the appreciation and volatility of a San Francisco, where there are real physical barriers and stronger political barriers to the spread of density, and where geography limits the suburban options. But it could surprise people.

Sorry – gotta disagree with you on Phoenix. I lived and worked in Phoenix for a few years, so I know the city and economy pretty well.

First, downtown Phoenix still has acres of vacant land. Only now is the city trying to encourage infilling because traffic and commutes are so bad. A lot of those same condos that went from $200K to $400K are now back to $250K (check out flips on the Camelback corridor).

Second, although the Phoenix economy has grown a lot in the last 10 years, it’s still mostly centered around construction and real estate related services – a one-trick pony.

Most importantly, people will always move to cities like SF for opportunity, weather, culture, and lifestyle. People only moved to Phoenix because because housing was cheap and there were lots of low-skilled jobs. Made sense if you were priced out of Inland Empire or laid off in the midwest. Or retiring. Outside of that, what’s the attraction to Phoenix? Not much IMO.

Anything has a price. Therefore, you can still pay too much for anything.

If available land is limiting variable for development in San Francisco, available water is the limiting factor for continued growth in Phoenix.

I have to disagree with this often cited mantra that “there is no available development land left in San Francisco.” This same phrase has been thrown around for decades and what did we see in the last 10 years – quite a bit of construction. While the development potential of San Francisco is not as obvious as weed covered vacant lots everywhere, you have to look at the total zoning potential of a site compared to the existing improvements to see how much is left to be built in the city. Then all of a sudden all of those one and even two story buildings throughout the city that can accommodate 4-story+ new buildings start looking like development lots rather than existing buildings. The planning commission knows this as well and has a pretty significant addition to the building base, both commercial and residential, factored into their growth models. Yes I agree that it is difficult and time consuming to get development approvals and the cost of pretty much every component of construction (land, labor, bricks and sticks, and soft costs like permits, etc.) are universally higher around here, so that definitely constrains supply. But the last two development booms – commercial building with the dot com boom and residential building with the recent residential boom – demonstrated that there is plenty of development land left around here once the price of the under-lying land rises higher than the value of marginal improvements on many older properties.

Money Magazine also rated San Francisco as the number 1 bullet-proof market along with New York, Boston and Seattle. They commented basically the city attracts high income employment and slow growth.

wayne: I was a banker in Manhattan in the early 90’s. Can’t tell you how many co-workers had to pull out their checkbooks to close escrow when they were SELLING their condos. It didn’t feel so “bullet-proof” back then, even amongst the “high income” set.

No market is bullet proof. I agree that SF will fall less than Phoenix or Sacramento, but you get to a point where the numbers just don’t make sense anymore, even for VC bankers and Google employees. I’m sure we all love San Francisco, but everyone has a breaking point where they’d rather move to Wyoming than pay $2 million for a studio or 80% of their salary in rent. But maybe I’m wrong, and international jet-set millionaires will rush in to buy here like the article implies.

Sorry for the double post, but wanted to throw this out there. Prices in the city are indeed falling, and have been since June. This is according to the Case-Schiller-Weiss/S&P index. The drops have been small so far and the city is still up year over year, but the price momentum is down. This index is calculated from sales of the same properties and using county recorder data, and is widely considered to be the best estimate of actual home values.

http://www2.standardandpoors.com/servlet/Satellite?pagename=sp/Page/PressSpecialCoveragePg&c=sp_speccoverage&cid=1143857726920&r=1&l=EN&b=4

I must still miss “the city” if I visit sites like this but the cost of living there has really taken away the advantages of San Francisco.

We sold our condo in Cow Hollow two years ago and moved to Chicago where we able to buy a larger place and invest the remaining profit. A coworker has recently left our San Francisco office for Chicago also. She bought a 2bd in 910 Lake Shore Drive (Mies Van Der Rohe high rise) for around 350k that has views of Lake and skyline. (She was a renter in S.F.) Are there any 2 bedroom condos in S.F. left for 350,000?

Chicago is not “the city”, but it is a “city” and at about 40% the cost.

Four 4-BR homes have gone on sale in my neighborhood in SF (south of Twin Peaks) over the past four months. All of them listed at $900k-$1.05MM. None of them have sold, most have cut their prices by $100k or so. Still not selling.

When the belief that houses are risklessly appreciating assets has washed away, suddenly families are less likely to overextend themselves anymore, which only leaves as buyers the types of people who can afford $1MM houses the old-fashioned way. How many families don’t already own a home locally and are looking to buy one for $1MM?

Disclaimer: My wife and I earn about $250k combined income with a new baby, and we consider ourselves priced out of the SFH market in SF. So who considers themselves priced *IN*?

Amen.

The only ones “priced in” were those who could sell their old places and roll forward $500K of equity. But if they can’t sell their old places, nothing moves and the mutual appreciation society adjourns. This would be OK if 2/3 of the city wasn’t financed with toxic loans.

“Only when the tide goes out do you see who’s naked”

Warren Buffet