This past March, Matt Lanning at the SFhomeBlog set out to demonstrate the “real-world” impact of rising mortgage interest rates on home values. As always, the devil is in the details (or in this case, the assumptions), and as such, we thought it might be interesting to use Matt’s own model, with updated assumptions (reflecting the ongoing changes in mortgage and home appreciation rates), to see what it says about the current market.

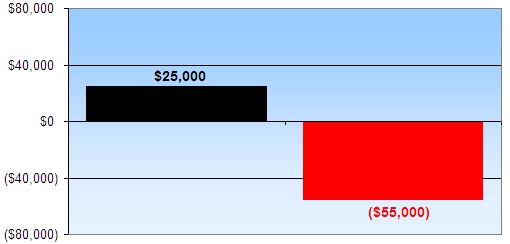

Matt’s model is straightforward: take the purchase of a $750,000 property (with 20% down) and after a year, net out the impact of decreased purchasing power due to rising interest rates from any increase due to local market appreciation. Based on this model, and with his assumptions, Matt suggests that you would have had a “positive price appreciation of at least $25k” from March ’05 to March ‘06. Key assumptions: mortgage rate moving from 5.75% to 6.5% (30-year fixed), and a “conservative” year-over-year market appreciation of 10%. Now let’s fast forward three months…

According to Bankrate.com, the benchmark 30-year fixed-rate mortgage is now 6.72% (up 1.07% from a year ago), and the benchmark 5/1 adjustable-rate mortgage is now 6.29% (up 1.14% from a year ago). In either case, in order to keep mortgage payments the same as a year ago, the price of a $750,000 property would have to drop to about $665,000 (for a loss of $85,000).

At the same time, year-over-year appreciation (imperfectly measured by the change in median sale price) is currently running around 4% and would suggest that a $750,000 property purchased a year ago should be worth $780,000 today (for a gain of $30,000). Based on Matt’s model, we now net the $85,000 loss against the $30,000 gain for an effective loss of $55,000 over the past year.

Yes, this model is flawed and overly simplistic, but it does highlight two points: 1. in any model, question the assumptions, and 2. the SFHomeBlog’s own model would suggest that property values are actually depreciating (not appreciating) in San Francisco. But please don’t blame us, it’s really not our model.

∙ Mortgage rate comparison – Then & Now [SFHomeBlog]

∙ Rates hardly move in paucity of economic data [Bankrate.com]

∙ SF Year-Over-Year Appreciation Now At 3.6% [SocketSite]

So basically as interest rates go up the good people of San Francisco get more and more screwed — is that the general idea? We need graphics for this? I can think of a graphic, but it’s not something to be printed in a good wholesome site such as yours!

Well, “screwed” really wasn’t what we had in mind (regardless, don’t blame the mortgage rates – they’re still reasonable). Think more along the lines of “it’s dangerous to position residential real estate as a fantastic financial ‘investment’ (as opposed to a home).” And yes, the USA Today style graphic was intended to be a bit tongue-in-cheek…

I could have told you the model was simplistic and self-serving based on who developed it. [Removed By Editor] I want a smart woman or man for my realtor who isn’t afraid to tell me the truth.